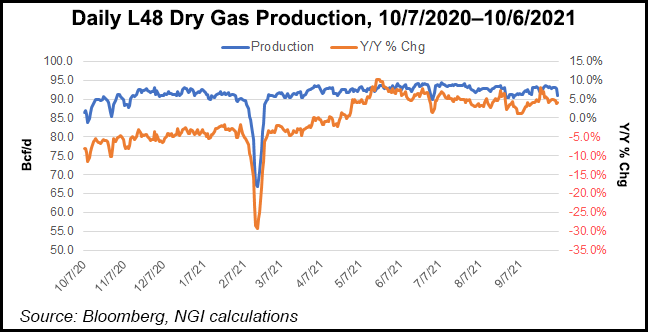

The ability of North America’s natural gas market to respond to price spikes this winter may be limited on both the supply and demand sides of the equation, according to experts.

In recent years, Lower 48 gas producers would typically respond to high prices by ramping up output. However, the response to the current price surge has been more muted, said NGI’s Leticia Gonzales, Price and Markets editor, in a recent presentation for Maxar WeatherDesk’s 20th Annual Energy Conference.

The relatively sluggish production response has partly been by choice, as publicly traded exploration and production (E&P) companies have prioritized capital discipline and returns over maximizing oil and gas output. Weather events such as Hurricane Ida, combined with stronger than expected...