Earnings | NGI All News Access

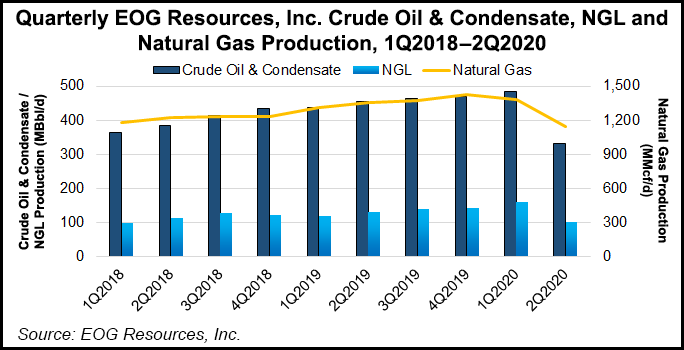

EOG Swings to Steep Loss as Coronavirus Crimps Demand, but Shut-ins Coming Back Online

Share on:

© 2024 Natural Gas Intelligence. All rights reserved.

ISSN © 2577-9877 | ISSN © 2158-8023 |

Earnings | NGI All News Access

© 2024 Natural Gas Intelligence. All rights reserved.

ISSN © 2577-9877 | ISSN © 2158-8023 |

Markets

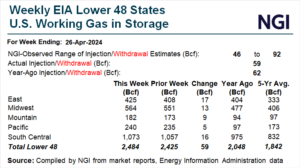

Weekly natural gas cash prices pushed upward, supported by lower production activity and forecasts for intensifying heat. Those catalysts also bolstered futures. NGI’s Weekly Spot Gas National Avg. for the April 30-May 3 period rose 15.5 cents to $1.385/MMBtu. As the trading week closed, leading gainers included Florida Gas Zone 3, up 36.0 cents to…

May 3, 2024By submitting my information, I agree to the Privacy Policy, Terms of Service and to receive offers and promotions from NGI.