Oil | Natural Gas Prices | NGI All News Access

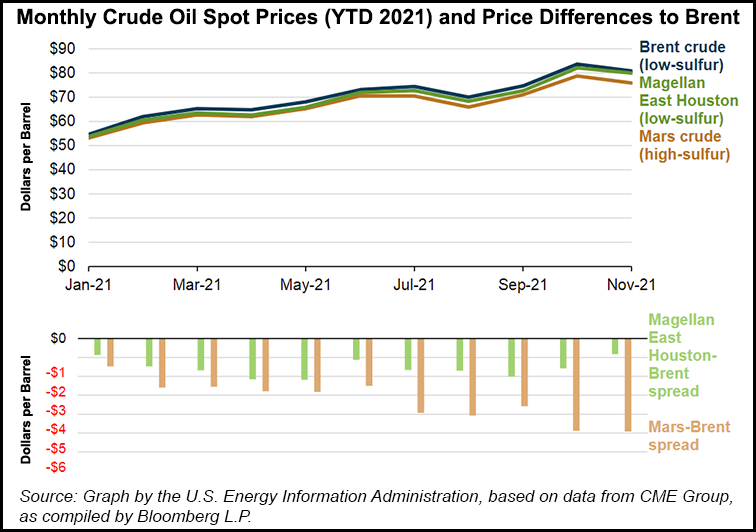

Divide Grows Between Sweet, Sour Oil Prices as OPEC-Plus, Natural Gas Play Key Roles

Share on:

© 2024 Natural Gas Intelligence. All rights reserved.

ISSN © 2577-9877 | ISSN © 2158-8023 |

Oil | Natural Gas Prices | NGI All News Access

© 2024 Natural Gas Intelligence. All rights reserved.

ISSN © 2577-9877 | ISSN © 2158-8023 |

Markets

Natural gas futures on Tuesday notched a fourth-straight day of gains – albeit barely – on maintenance-induced reductions to already lower production activity. At A Glance: Production hits May low Weather forecasts mixed LNG steadies above 12 Bcf/d Coming off a cumulative gain of more than 25 cents over the prior three sessions, the June…

May 7, 2024Earnings

By submitting my information, I agree to the Privacy Policy, Terms of Service and to receive offers and promotions from NGI.