Infrastructure | E&P | NGI All News Access

U.S. Rig Count Stable as SCOOP Activity Increases, Says BHI

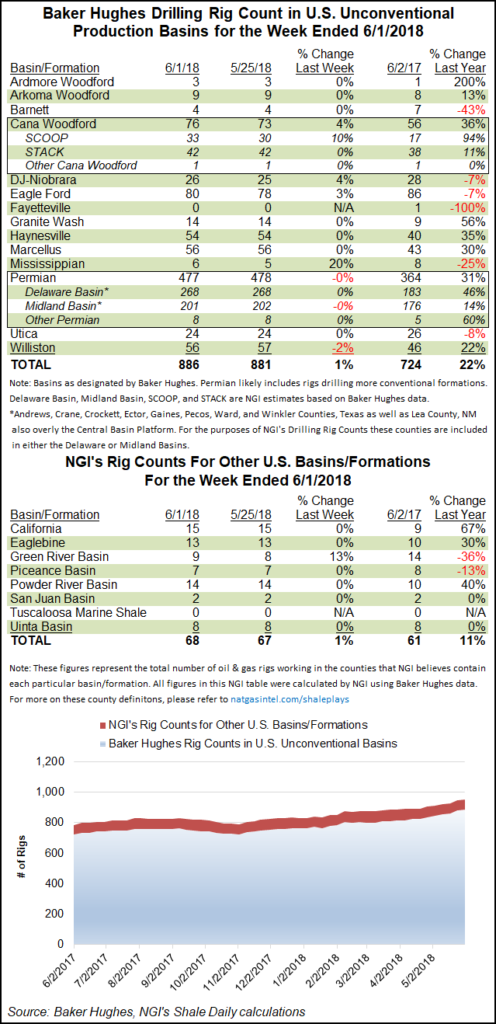

The U.S. rig count held steady for the week ended Friday, adding one net rig thanks to a small increase in oil-directed drilling, according to data from Baker Hughes Inc. (BHI).

The United States added two oil rigs and dropped one natural gas-directed unit to end the week at a combined 1,060 rigs, up 16% from 916 rigs running a year ago.

Three horizontal units were added, while two directional units packed up for the week, according to BHI. Three land rigs returned, while two departed from inland waters. The Gulf of Mexico finished flat week/week (w/w) at 18 rigs.

Canada saw 18 rigs return to the patch for the week, with an increase of 21 oil rigs offsetting the departure of three gas units. Canada finished at 99 rigs, in line with its year-ago total.

The combined North American rig count as of June 1 stood at 1,159, up from 1,015 rigs a year ago, according to BHI.

Among major basins, the biggest weekly increase came in the Oklahoma’s Cana Woodford, which added three rigs to grow its count to 76 from 56 a year ago. According to a more detailed breakdown of BHI data by NGI’s Shale Daily, all those rigs were added in the South Central Oklahoma Oil Province (aka the SCOOP), which finished the week at 33 units. The STACK, aka the Sooner Trend of the Anadarko Basin, mostly in Canadian and Kingfisher counties, finished flat w/w at 42 rigs.

Other gainers for the week included the Eagle Ford Shale, which saw two rigs return, along the Denver Julesburg-Niobrara formations and Mississippian Lime, which added a rig a piece.

The oil-focused Permian and Williston basins each dropped one rig from their respective tallies for the week.

Among states, Oklahoma led with a w/w increase of two rigs to finish at 142 units, while Texas, Wyoming and Colorado each saw one rig return to the patch. Louisiana dropped two rigs w/w to fall to 58 units, while New Mexico and North Dakota each had one unit exit the patch.

Crude oil futures have pulled back sharply since last week, in part on suggestions that the Organization of Petroleum Exporting Countries and its allies, including Russia, could ramp up more oil to global markets “in the near future” to fill the gap from U.S. sanctions on Iran and the loss of Venezuela output, as signaled recently by the Saudi Arabia energy minister.

During a panel discussion hosted by CNNMoney, Khalid Al-Falih said discussions are ongoing with cartel members and Russia to balance the market and reduce prices, which had climbed to about $80/bbl in recent weeks.

After cracking the $70/bbl mark earlier in the month, New York Mercantile Exchange July West Texas Intermediate futures were down around $66/bbl Friday.

Meanwhile, U.S. natural gas producers are guiding toward 4.2 Bcf/d in output gains this year versus 2017, based on a survey of 50 of the largest onshore operators by UK-based Energy Aspects Ltd. (EA). The survey represents more than half of the firm’s total year/year (y/y) U.S. projected growth forecast of 7.0 Bcf/d.

The biggest uncertainty looming for Appalachian and Permian exploration and production companies is takeaway capacity, according to analyst David Seduski.

Range Resources Corp. “noted in its conference call that without additional capacity it has contracted on the beleaguered Rover Phase 2, its Appalachia production was likely at a ceiling of 1.2 Bcf/d,” while Cabot Oil & Gas Corp. “cited the need to temper expectations until work is completed on Atlantic Sunrise.”

Lots of questions during first quarter calls also centered around Permian gas constraints, which exploration and production executives noted are linked to oil takeaway rather than gas infrastructure.

Anadarko Petroleum Corp. CEO Al Walker during the 1Q2018 conference call said of the Permian, “The ability to extract that gas into any market at a reasonable price is an objective of ours, in order to evacuate the liquids at the most economically available way we can.”

© 2024 Natural Gas Intelligence. All rights reserved.

ISSN © 2577-9877 | ISSN © 2158-8023 |