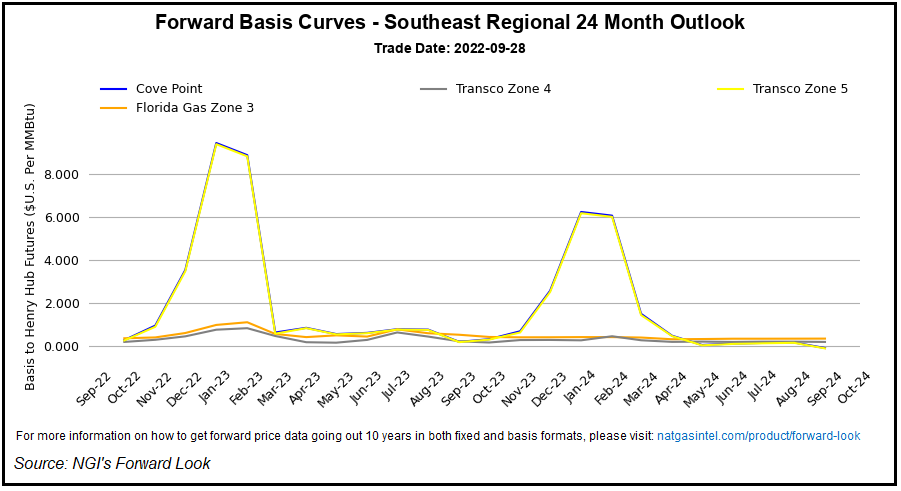

With natural gas production remaining stout – even amid temporary shut-ins ahead of Hurricane Ian – and cooler weather leaving its mark on storage inventories, natural gas forward prices continued to fall during the Sept. 22-28 week, according to NGI’s Forward Look.

In the latter part of the period, all attention was on Florida, where Ian packed maximum sustained winds around 150 mph when it made landfall on the southwest coast near Cayo Costa Wednesday afternoon.

The system was downgraded to a tropical storm on Thursday but regained hurricane status by early Friday. Ian made a second landfall as a category 1 hurricane near Georgetown, SC, Friday afternoon.

About one million Florida utility customers remained without power as of Friday afternoon, with more outages...