The natural gas market in Mexico is a new opportunity for private sector producers, as firms begin to analyze alternative possibilities, according to a research note from consultancy Talanza.

“Natural gas has become a worldwide commodity, and particularly in Mexico, a scarce one,” Talanza analyst Daniela Flores said. “In that sense, natural gas-producing companies must capitalize on their production and turn it into profit.”

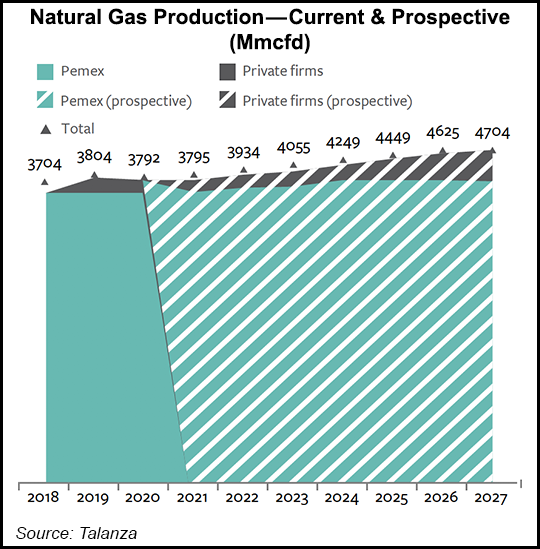

Mexico, which imports most of its gas from the United States, has been importing more than its domestic production since 2015. This is in part because of declining domestic production from Petróleos Mexicanos (Pemex), but is also because of the abundance of cheap gas north of the border.

As a result of the opening of the upstream sector as...