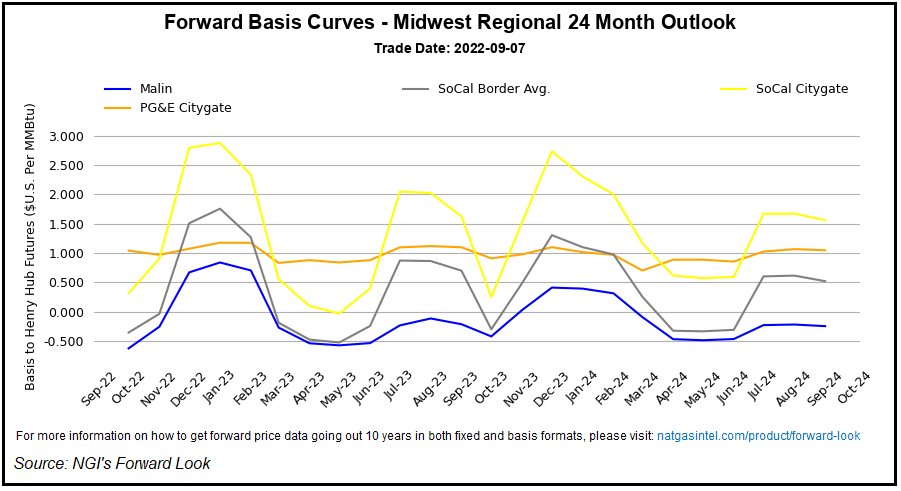

Amid erosion of value in the futures market as traders continued to try to price in winter supply risks, regional natural gas forwards pulled back sharply throughout the Lower 48 during the Aug. 31-Sept. 7 period, NGI’s Forward Look data show.

From coast to coast, hubs posted fixed price declines of $1-plus for October delivery, paced by a $1.199 discount at benchmark Henry Hub, which finished the period at $7.848/MMBtu.

The unusual circumstances surrounding the upcoming winter, notably in the context of Europe’s ongoing energy crunch, continued to drive volatility during the period as the market contemplated the risks posed by exposure to overseas pricing.

On the domestic front, strong production numbers and fading heat in the transition to the shoulder season also...