LNG | LNG Insight | NGI All News Access

LNG Prices Still Bearish on Limited European Delivery Slots

Share on:

© 2024 Natural Gas Intelligence. All rights reserved.

ISSN © 1532-1231 | ISSN © 2577-9877 |

LNG | LNG Insight | NGI All News Access

© 2024 Natural Gas Intelligence. All rights reserved.

ISSN © 1532-1231 | ISSN © 2577-9877 |

Markets

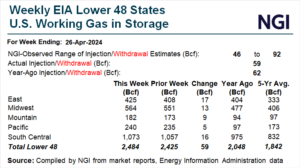

Natural gas futures on Thursday snapped a two-day losing streak, bolstered by a bullish storage print, lower production and forecasts for strong summer heat. At A Glance: EIA prints 59 Bcf injection Hotter temperatures ahead Output hovers at 97.6 Bcf/d The June Nymex gas futures contract rallied 10.3 cents day/day and settled at $2.035/MMBtu. After…

May 2, 2024By submitting my information, I agree to the Privacy Policy, Terms of Service and to receive offers and promotions from NGI.