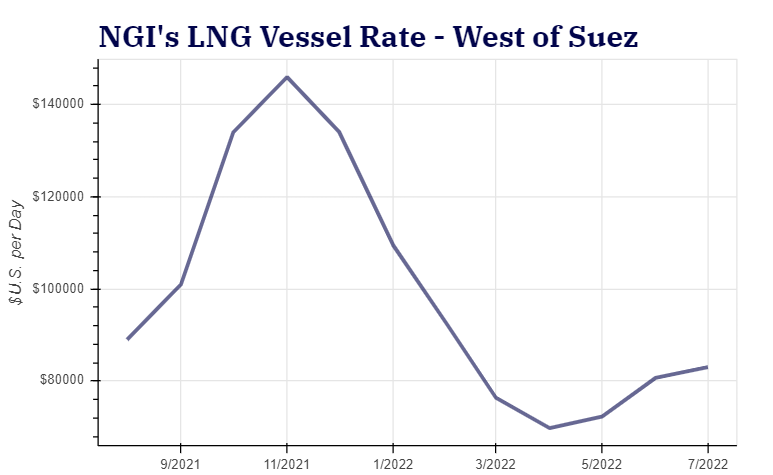

The liquefied natural gas (LNG) shipping market remains tight as demand from South America to Asia is strong, but analysts said freight rates could diverge from LNG prices in the coming weeks on a variety of factors.

For now, vessel rates are up. While the spot market in the Pacific Basin is “fairly quiet,” demand for shipping remains high in the Atlantic Basin, shipbroker Fearnleys AS said this week. Daily vessel rates in the Atlantic for a standard 174,000 cubic meter vessel were at $89,000 on Friday, up from $75,000 a week earlier, according to Fearnleys. In the Pacific, they stood at $73,000, up from $65,000 the prior week.

Strength in the Atlantic market is being driven by booming U.S. exports. While American exports slowed this month on maintenance outages, Vortexa...