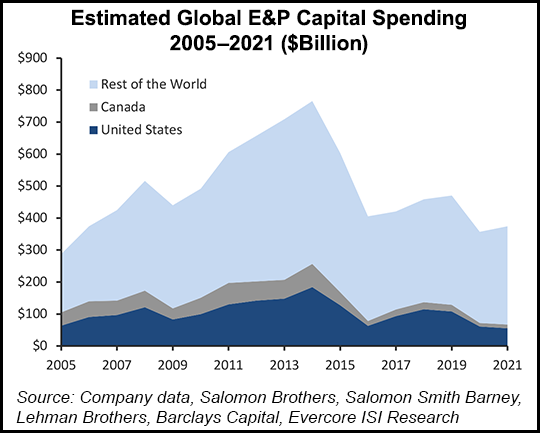

The collapse in global exploration and production (E&P) spending last year ranked among the worst downturns in history, but 2021 is the beginning of a multi-year recovery that will accelerate into 2022 and beyond, according to Evercore ISI.

The firm’s Global E&P Mid-Year Spending Outlook indicates U.S. producers remain a bit cautious regarding their capital expenditures (capex) plans. However, as Henry Hub natural gas and West Texas Intermediate (WTI) prices strengthen, E&Ps could increase their spending into the last half of this year.

The mid-year forecast, completed in May, is an update of Evercore’s annual survey published last December. Like the initial survey, the update provides insight into about 250 producers that work around the world, including the energy majors,...