NGI The Weekly Gas Market Report | Coronavirus | LNG | LNG Insight | Markets | NGI All News Access

Coronavirus Thrusts LNG Market Further into Turmoil as More Cargoes Float with Nowhere to Go

Bedlam reigned in the global natural gas market on Thursday as more force majeures were issued, cargoes appeared to have nowhere to go, and prices continued spiraling because of widespread measures to stem the coronavirus outbreak.

The uncertainty and quickly changing dynamics were deepening an imbalance in the liquefied natural gas (LNG) trade that has plagued the global market since last year. Ship brokerage Poten & Partners warned Wednesday during a webinar that the virus could weigh on LNG for the next 18 months. U.S. export terminals, the firm said, would likely be the first to cut supply as producers respond to restore balance.

“I think we’re going to most likely see some pretty significant cargo cancellations,” said Poten’s Jason Feer, global head of business intelligence. “We saw a few this spring, but there were places to put them and a lot of those cargoes were at least in the money on a cash basis or a variable cost basis. By fall, though, we think you’re going to have to see some pretty significant response in terms of supply. We think U.S. cargoes are likely to shoulder most of the cuts, but other producers are already talking about reducing supply.”

U.S. netbacks were already squeezed, with marginal returns in Europe where storage is at record highs and demand is crumbling as the continent is hunkered down against the coronavirus. Margins in Asia were only slightly better, but demand is still wavering in the region as the pandemic continues taking its toll. LNG was facing headwinds coming into 2020 given the supply glut, while weak winter weather in the Northern Hemisphere hasn’t helped and the recent supply shock in oil markets has sent crude-linked prices to the floor.

“Delays to the start-up of new capacity will relieve some market pressures, but LNG producers with high variable costs are likely to be affected,” the Boston Consulting Group said in a report earlier this week. “It already appears that the U.S. is being affected. Some cargoes have been cancelled and capacity utilization at U.S. plants fell to 60% in early March, down from an average of around 90% in 2019.”

Long-term U.S. contracts are more flexible, while the wholesale market has higher marginal costs than stranded assets from some overseas projects that pull associated gas from oil production. Some U.S. offtakers also face high variable expenses, such as those for shipping and regasification at import terminals.

“U.S. supply is already barely above water on a variable cost basis,” Feer said, adding that the forward curve suggests the cost of lifting cargoes would be uneconomic.

In Italy, among the hardest hit countries in the world, gas demand has slipped by 23% compared with the same time last year, Feer said. In Spain, he said importers have warned of a 10% demand decline in April.

Southern Europe was once a bright spot in a global market where demand had already been softening before the outbreak. Key buyers in Italy and Spain are reportedly considering declaring force majeure.

Meanwhile, despite some economic recovery in parts of Asia, activity isn’t expected to bounce back completely for months.

“We have seen in the past when markets have become volatile and prices have become low,” the Asia-Pacific region “gets saturated,” Feer said. In those circumstances, it becomes “very difficult” to find buyers.

“For the Japanese and Koreans, this would be a great time to buy cargoes, but they’re not doing it a great deal,” he said. “Storage is full, they have their burn plans in place for the rest of the year, so they’re not picking up incremental cargoes, and that kind of phenomenon we’ve seen before, where Asia seems to offer a better market, but it becomes difficult to actually place cargoes.”

Other areas in the region, including India, are only now grappling with the severity of Covid-19. The country has provided relief lately with its opportunistic buying of cheap cargoes. However, a highly restrictive three-week lockdown began Wednesday in India, prompting ports and LNG buyers to announce force majeures as they faced manpower shortages.

Gail Ltd., Gujarat State Petroleum Corp. and Petronet LNG Ltd. all reportedly issued notice that they couldn’t take volumes. Gail has 20-year contracts to buy LNG from both Cove Point in Maryland and Sabine Pass in Louisiana.

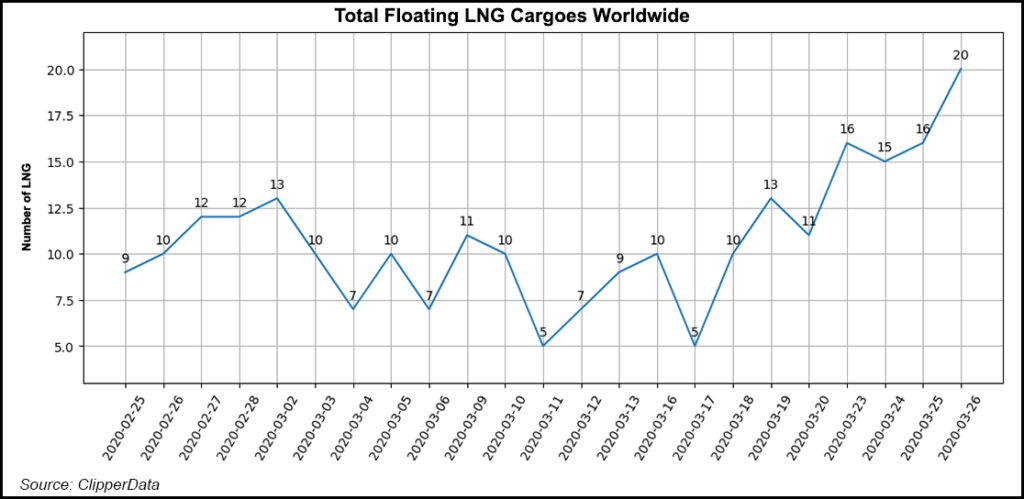

Shipping operations have been upended by the virus too. ClipperData said Thursday there were six LNG cargoes floating off the west coast of India and one offshore Pakistan. Another four laden vessels were anchored near Qatar, the world’s largest exporter, which was also reportedly offering cargoes for April and May delivery on Thursday.

Across the world, ClipperData said 20 vessels were floating with nowhere to unload, compared to 13 at the same time last week. Kpler LNG analyst Nathalie Leconte said the firm’s tracking data showed a similar spike, with 12 LNG vessels tagged as floating storage, compared to seven a week ago. Estimates differ based on how firms define floating storage, which can include varying factors such as time at sea, speed of travel and direction.

The chaos has pushed global gas prices down. Asian spot prices fell about 18 cents between Wednesday and Thursday, while the Japan Korea Marker prompt month also dropped. The Dutch Title Transfer Facility was trading near record lows on Thursday, while Henry Hub continues to test the floor at well below $2.00.

“It’s a difficult situation that the market finds itself in,” said Pareto Commodities’ Brad Hitch, head of LNG.

The global gas market has continued to evolve from a more rigid model that leaned heavily on restrictive long-term contracts linked to oil prices. More players have entered the market over the last two decades and liquidity has increased, but Hitch said the virus is testing the market in an unprecedented way.

“There are still a lot of countries that don’t import LNG or import very little, and they theoretically could be out in the market absorbing some of this supply in this kind of situation, but given the way the market has developed with these point-to-point contracts, this is one of the problems with it,” Hitch told NGI. “It has built in a lot of inflexibility, and to a certain extent, it’s a nightmare scenario because of that.”

Poten said in a best-case scenario, year/year demand growth of 0.5% is expected in 2020, with 1% growth forecast for 2021. If the virus were to lead to more severe impacts, Poten expects LNG demand growth to decline by about 4.7%, which Feer said would be “unprecedented.” The firm still sees a supply surplus of 4 million tons this year, down from its pre-virus expectations of 8 million tons.

Given the pandemic, Boston Consulting Group analysts Alex Dewar and Juan Vazques said they expect global LNG demand to drop by 6% in the near-term, or the equivalent of 25 million metric tons/year.

One winner from the fallout could be Latin America. For example, Argentina recently lined up 11 LNG cargoes in preparation for the upcoming Southern Cone winter. Others throughout the region could step in as opportunistic buyers.

“Potentially Brazil or Mexico could be the beneficiaries of a lot of availability and low cost,” Hitch said. “The challenge of course is how much gas can you get into the Mexican terminals, really more than what they need, given the U.S. pipelines. I don’t know what the port situation is in Brazil, whether they have the ability to take in a lot of tankers right now.”

Brazil’s Petroleo Brasileiro SA, aka Petrobras, and Mexican state-owned electric utility Comision Federal de Electricidad are among the biggest spot buyers in the Atlantic Basin. However, lockdown measures are also spreading throughout the region as the virus has made its way there.

ClipperData’s Kaleem Asghar, director of LNG analytics, said more ships could make their way toward Latin America, but he said the region doesn’t have the kind of appetite to absorb all the cargoes that are likely to be available.

“And honestly speaking, these are uncertain times. I would hold on my buying until the last minute” to pick up “distressed cargoes.”

© 2024 Natural Gas Intelligence. All rights reserved.

ISSN © 1532-1231 | ISSN © 2577-9877 | ISSN © 1532-1266 |