Weekly California NatGas Weakens, East Strengthens As Gas Migration West Builds

On the surface it looked like a benign week of trading as overall prices moved little and many areas of the country experienced only modest price changes. The NGI National Weekly Spot Gas Average fell just a penny to $2.44, but larger moves in the East and California may augur a shifting natural gas price landscape.

The point with the largest weekly gain proved to Transco Zone 6 NY with an 83-cent rise to $2.17, and the week’s laggard was Kern Delivery with a 33-cent loss to $2.75. All Rocky Mountain points were in the red for the week.

That east-west split looks to be the result of infrastructure now being completed to bring underpriced Marcellus and Utica gas westward, increasing quotes in the East and putting downward pressure on Rockies and California gas.

Fittingly, the Northeast proved to be the week’s top regional gainer with a 28-cent advance to $1.75, and California held a solid grip on the cellar with a 23-cent loss to $2.81. For the week, the Henry Hub at $2.72 was just a penny under the SoCal Border average.

Rockies quotes proved to be the next region out of the cellar with at 13-cent loss to $2.49 and the Midcontinent shed 9 cents to $2.59.

East Texas shed 7 cents to $2.68 and South Texas was off 6 cents at $2.65.

The Midwest came in 6 cents lower at $2.74 and South Louisiana fell a nickel to $2.69.

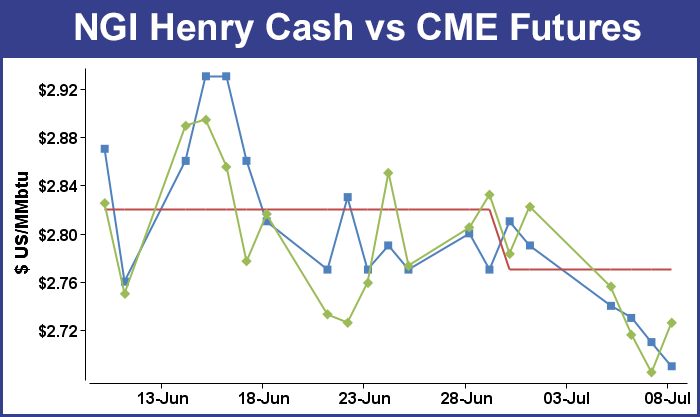

August futures for the week fell 5.2 cents to $2.770, and had it not been for a counterintuitive move higher in response to a bearish Energy Information Administration (EIA) storage report Thursday, the decline might have been greater. In its weekly release of storage data, the EIA reported a build of 91 Bcf, somewhat greater than what was anticipated. August futures fell to a low of $2.644 after the number was released and by 10:45 EDT August was trading at $2.659, down 2.6 cents from Wednesday’s settlement. That decline proved to be short-lived however, and at the closing bell August had gained 4.1 cents to $2.726 and September was higher by 4.1 cents as well to $2.738.

Prior to the release of the data analysts were looking for an increase in the mid 80 Bcf range. Industry consultant Bentek Energy utilizing its flow model calculated a build of 88 Bcf, and IAF Advisors was counting on a 84 Bcf increase. A Reuters poll of 23 traders and analysts showed an average 86 Bcf with a range of a 79 Bcf to a 93 Bcf injection. Industry consultant Bentek Energy predicted an 88 Bcf build utilizing its flow model and said the number could go even higher due to the holiday. “Demand in the U.S. fell 2 Bcf/d from the previous week, largely due to power burn demand as temperatures fell in the eastern half of the country,” the firm said.

Traders were unimpressed with the move lower. “There’s not a lot of conviction in the market’s move. It’s just drifting within its [established] trading range,” said a New York floor trader.

When queried whether today’s apparent lack of downside follow through to an otherwise bearish number offered a buying opportunity, the trader said “I think a little lower from here. The upper $2.50s to lower $2.60s. The problem is there is nothing fundamental on the horizon to change people’s opinions.”

Tim Evans of Citi Futures Perspective saw the “91 Bcf build for last week was above the consensus estimate and also more than the 76-Bcf five-year average refill, and so moderately bearish in terms of its immediate price impact. This will be a test for the market, but we still expect prices to hold above the June and April lows, which may set up an eventual intermediate-term price recovery.”

Inventories now stand at 2,668 Bcf and are 658 Bcf greater than last year and 45 Bcf more than the 5-year average. In the East Region 69 Bcf were injected and the West Region saw inventories decrease by 1 Bcf. Stocks in the Producing Region rose by 23 Bcf.

In Friday’s trading buyers elected to step up to the plate and commit to three-day purchases rather than rely on short-term “as-needed” buys. Weather forecasts suggested warm temperatures and elevated heat indices over major markets, and overall prices added 5 cents to $2.43.

Gains were deep and widespread, and only a handful of points failed to turn positive. Forecasts of stout power loads and higher Monday peak power prices made the buying decision all that much easier. Futures gained as well, encouraged by longer-dated weather forecasts that turned supportive also. At the close, August had risen 4.4 cents to $2.770 and September was higher by 4.2 cents to $2.780. August crude oil eased 4 cents to $52.74/bbl.

Northeast points scored gains close to a dime as Monday on-peak power prices advanced. Intercontinental Exchange reported that Monday peak power at the New York ISO Zone G delivery point (eastern New York) rose $3.92 to $37.25/MWh and on-peak power at the ISO New England’s Massachusetts Hub added $6.65 to $34.75/MWh. Monday power at the PJM West terminal came in at $40.70/MWh, up $7.38.

Three-day parcels at the Algonquin Citygate rose by 37 cents to $2.09, and gas on Iroquois Waddington gained 13 cents to $2.90. Deliveries to Tennessee Zone 6 200 L added 43 cents to $2.12.

Gas on Tetco M-3 added 7 cents to $1.29, but packages bound for New York City on Transco Zone 6 fell a dime to $1.86.

Marcellus points made modest gains. Three-day gas on Millennium added 6 cents to $1.06, and deliveries to Transco Leidy changed hands 3 cents higher at $1.06. Gas on Tennessee Zone 4 Marcellus rose 6 cents to $1.02, and gas on Dominion South was seen 6 cents higher at $1.12.

Monday power loads were forecast to be significantly higher than Friday. The New York ISO forecast Friday’s peak load at 24,854 MW and Saturday was seen dropping to 22,832 MW. By Monday, peak load was expected to reach 26,459 MW. PJM Interconnection said Friday’s peak load of 44,028 MW would ease to 41,687 MW Saturday, but by Monday peak load was seen rising to 46,351 MW.

The Henry Hub added 6 cents to $2.75, and with only a few exceptions all actively traded points in the East and Northeast fell below Henry. “Henry Hub in the summer has become the premium market. Other than Transco Zone 5 and a few other outliers, everything is trading below that,” a Houston-based pipeline veteran told NGI. “Most of the gas will end up in the Far East and Asian markets.”

Other market hubs were firm as well. Chicago Citygate added 7 cents to $2.74, and gas on El Paso Permian rose 3 cents to $2.51. Deliveries to PG&E Citygate also tacked on 2 cents $3.06.

The ultimate driver of the day’s power and gas price matrix was weather reports calling for near-term warmth. “The unseasonably cool air from portions of the Great Plains, Midwest and Great Lakes region will give way to much warmer conditions going into the weekend, with downright hot temps expected to develop from the northern Plains to upper Midwest, and near to slightly above-normal temps across the rest of the Great Lakes, Ohio Valley and New England, said Steve Gregory, a meteorologist with Wunderground.com.

“The question is, will it last for more than a few days, especially in the Great Lakes to New England. The subtropical ridge (‘Bermuda High’) has begun to build back into the southeast U.S. and will slowly retro-grade westward towards the Great Plains by early next week.”

Like the pioneers of the 19th century, gas keeps moving west. On Friday, Rockies Express Pipeline LLC (REX) notified FERC that on Thursday it had placed into service new facilities at its Chandlersville and Hamilton compressor stations as part of its Zone 3 East-to-West project [CP14-498]. The project is expected to be fully operational around the beginning of August.

The market impact of the expansion isn’t totally clear, but once the capability to move large volumes out of the Marcellus to higher-priced markets like the Midwest comes into play, the present $1.50 premium Chicago Citygate enjoys over Marcellus points is sure to narrow. “Once these modifications are complete, the Rockies Express Zone 3 mainline will become bidirectional between the Clarington Hub located in Monroe County, OH, and the existing Natural Gas Pipeline Co. of America delivery interconnect located in Moultrie County, IL, which in turn will generate 1,200,000 Dth/d of firm east-to-west transportation capacity on this portion of the system,” REX told the Federal Energy Regulatory Commission last year (see Daily GPI, June 24, 2014).

Traders looking at recent price action are seeing an extension of the move lower rather than any signs of a longer-term market reversal. “[Thursday’s] reversal is offering solace to the bulls, but we continue to prioritize chart deterioration, re yesterday’s new one-month lows,” said Jim Ritterbusch of Ritterbusch and Associates in a Friday morning note to clients.

“This market appears to be acquiring some bullish spillover from the gains across most of the oil complex since we haven’t seen significant adjustments in the short-term temperature views to support higher values. Additionally, yesterday’s larger than expected 91 Bcf storage injection…is likely to be followed next Thursday by a bigger build than seen yesterday.

“This implied expansion in the surplus against five-year average levels should be able to contain additional price strength unless the weekend brings some significant changes in the short-term weather views in the direction of some warm trends across the heavily populated northeast quadrant of the U.S. We feel that [Thursday’s] upside price reversal and this morning’s bullish follow-through is more representative of technical factors and a strong desire on the part of the large speculative entities to accept profits rather than any significant changes in short-term fundamentals.”

Gas buyers over the weekend across the MISO power pool will likely have their work cut out for them as wind generation looks to be highly variable. WSI Corp. in its Friday morning report said, “A residual frontal boundary will remain a focal point for showers and storms across the Ohio and mid Mississippi Valley today. Otherwise, weak high pressure will support partly sunny skies. Highs will range in the upper 70s and 80s. A warm front and wave of low pressure will shift the best chance of additional shower and thunderstorm activity into the Upper Midwest and Great Lakes during the weekend, but the chance of rain and storms will become more widespread early next week.

“Light wind generation is expected most of today, but wind gen will gradually increase tonight into the weekend. Generation will be variable but might peak upward of 4-6 GW at times. Wind gen will remain variable but relax a bit early next week.”

© 2024 Natural Gas Intelligence. All rights reserved.

ISSN © 2577-9877 | ISSN © 1532-1258 |