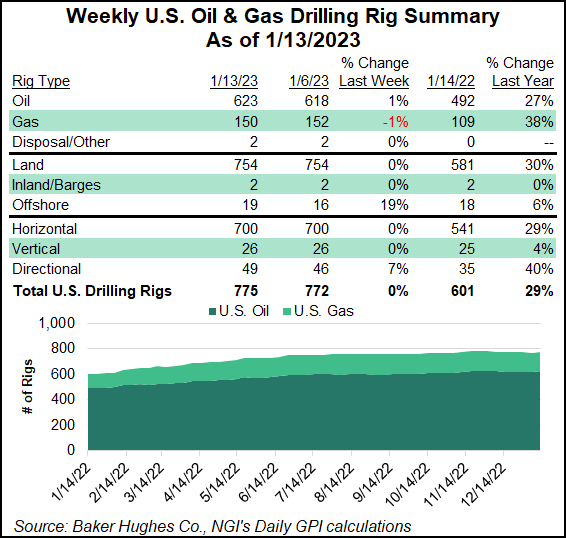

Bolstered by gains in the oil patch, including in the Permian Basin and the Eagle Ford Shale, the U.S. rig count rose three units to reach 775 during the week ended Friday (Jan. 13), according to updated numbers published by Baker Hughes Co. (BKR).

Changes in the United States for the week included a five-rig increase in oil-directed drilling, partially offset by a two-rig decline in natural gas-directed drilling. Activity on land was unchanged overall for the week, while the Gulf of Mexico added three rigs to raise its total to 19. Directional rigs increased by three, while total horizontal and vertical units were flat week/week.

The combined 775 active U.S. rigs as of Friday compares with 601 rigs running in the year-earlier period, according to the BKR numbers, which are...