Loosening balances, evidenced by a weekly inventory build that overshot major surveys, accompanied declines in forward prices for most of the Lower 48 during the Aug. 12-18 trading period, NGI’s Forward Look data show.

Nymex September futures experienced some up-and-down action, but on the whole lost ground during the Aug. 12-18 time frame, including a steep 10.9-cent sell-off on Tuesday (Aug. 17).

An 8.1-cent decline in September Henry Hub coincided with fixed price front-month discounts at most Lower 48 hubs for the period.

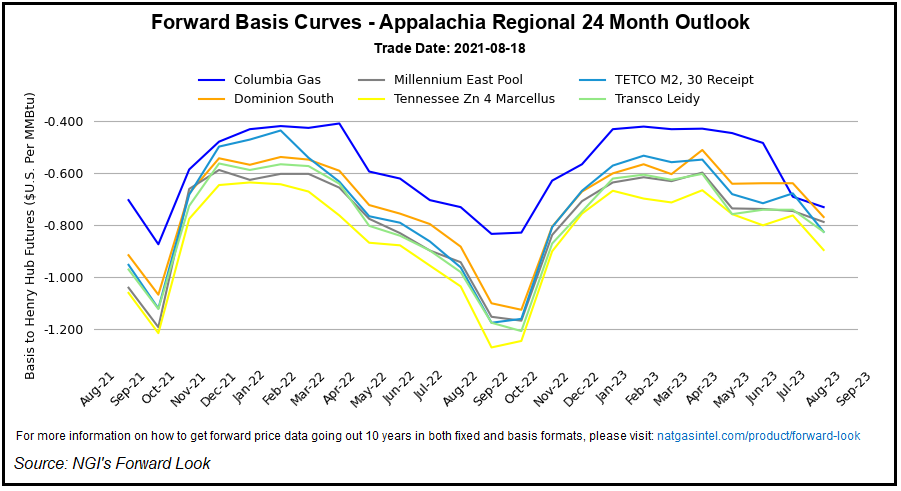

Meanwhile, forward contracts at hubs in the West and in Appalachia saw both fixed price gains and strengthening basis as they bucked the broader market downtrend.

Post-Storage Bounce

Nymex futures initially seemed poised to add to recent losses...