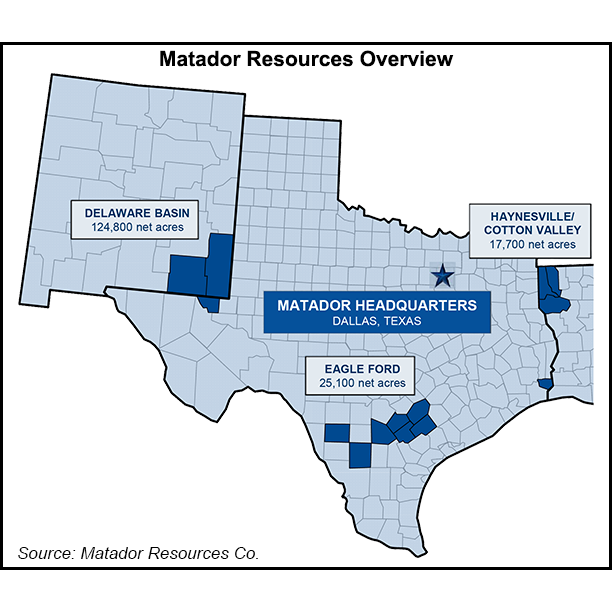

Matador Resources Co. is seeing better than expected results from recently completed wells in the Permian Basin’s Delaware sub-basin, according to CEO Joseph Foran.

As a result, Dallas, TX-based Matador is increasing the midpoints of its full-year 2022 production guidance from 21.7 to 21.85 million bbl for oil, and from 95.5 to 97.0 Bcf for natural gas, Foran said upon announcing the firm’s third-quarter 2022 results.

The upwardly revised figures translate to about 59,863 b/d and 266 MMcf/d, respectively. The midpoint of expected 2022 capital expenditures remains unchanged at $800 million.

“Operating efficiencies, which include faster drill times and use of existing facilities, continue to improve and help to mitigate service cost inflationary pressures realized in...