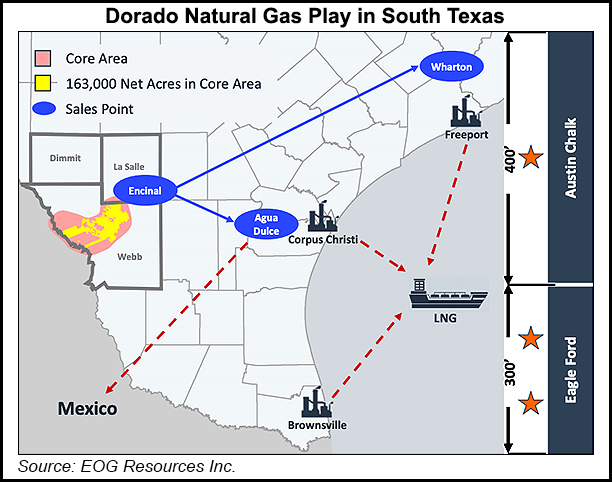

The Dorado, a stacked play in South Texas where EOG Resources Inc. has amassed a 163,000 net acre leasehold, may be a lock to build the Houston independent’s natural gas market credentials, the executive team said Friday.

The formation, which runs through the Austin Chalk and Eagle Ford Shale, has an estimated 21 Tcf net resource potential and is “highly competitive” with EOG’s oil inventory, according to the management team.

The Houston-based executive team shared results from the fourth quarter and a look ahead during a quarterly conference call. CEO Bill Thomas pointed to solid quarterly results across the board, that came during a dire year for the energy sector.

“EOG made significant improvements to its operating performance during 2020, across every area of...