E&P | NGI All News Access | NGI The Weekly Gas Market Report

EnerVest Lender Not ‘Trying to Take Control’ of Assets

Houston-based EnerVest Ltd., one of the largest privately held onshore exploration operators in the United States, is working with its investors and lenders to recapitalize over-leveraged equity funds and may sell more assets to ensure it is in compliance. However, one of the funds is not about to be taken over by one of the lenders, a spokesman told NGI.

A story published Monday in The Wall Street Journalsaid a $2 billion fund launched in 2013 was “worth essentially nothing” and had wiped out investments by major pensions, endowments and charitable foundations.

The fund’s lenders, led by Wells Fargo & Co.,“are negotiating to take control of the fund’s assets to satisfy its debt, according to people familiar with the matter,” the Journalsaid.

EnerVest spokesman Ron Whitmire, chief administrative officer, said that’s not true.

“Wells Fargo is not trying to take control of any of EnerVest’s funds to satisfy the debt,” Whitmire said. In simple terms, EnerVest is not broke.

“That was one of the most unfortunate pieces of that article,” Whitmire said of the Journalstory. “The way to look at EnerVest is each fund gets its own entity, its own company, if you will. There are two common threads. One, EnerVest Ltd. is the general partner of each of those entities. And two, EnerVest Operating, which is 99% of our employees, operates all the wells. But other than that, they’re all separate, legal entities.”

EnerVest during the run-up in oil prices used investor-backed funds to gobble up a huge swath of properties across the U.S. onshore. Funds were designated to buy stakes in, among other places, the Permian Basin, Barnett Shale, Eagle Ford Shale, Austin Chalk, Appalachia and in the Oklahoma’s STACK/SCOOP, aka the Southern Trend of the Anadarko Basin, mostly in Canadian and Kingfisher counties and the South Central Oklahoma Oil Province.

When oil prices collapsed, “we found that we were getting killed in data rooms on oil properties,” Whitmire said. “So we sold what we had in the Permian Basin, which was a very nice position, and that was a great divestiture for us.

“At the same time, during the run-up, we were buying in Fund 12, which is a lot of Barnett, while Fund 13 is a lot of Midcontinent…We bought those at the higher prices, and we did our typical 30-35% leverage that we’ve done throughout the history of the company. And then commodity prices plummeted.”

The “modest percentage now was over-levered. And that’s where we are right now.”

EnerVest now is working “with both our investors and our bank groups to recapitalize those two funds and or sell assets to get us closer to compliance with our bank groups.”

Wells Fargo is the lead bank for Funds 12 and 13, he said. “As the lead banker, they’re very engaged in what we’re doing in funds 12 and 13 to try to right the ship, of course. But no, they’re not trying to take over…

“When you have 18 or more banks in a bank group, you’re going to probably have 18 different positions. So, are the bank groups putting pressure on us? Yes. That’s their job. But it’s been a good working relationship throughout the process,” he said.

“When we recognized that we had an issue, we reached out to the banks. We didn’t wait for them to call and they were appreciative of that. I’m sure that they wish like we wish that it hadn’t been going on as long as it has. But we’re all still working together for the best possible outcome.”

There hasn’t been any pressure from investors that he is aware of, as they recognize the situation for what it is. Many energy companies are pressured by stagnant commodity prices and lack of demand.

“The options are fairly limited right now. Sell or you recapitalize,” he said. “Hope is not a strategy. You can’t bank on prices.”

EnerVest has five rigs working in the onshore today, with two in the Eagle Ford, one in Virginia’s Nora field, one in the Austin Chalk in East Texas and one in the Barnett Shale.

Fund 15, EnerVest’s most recent and active fund, acquired the Eagle Ford position, along with Nora from Range Resources Corp. in southwestern Virginia. It acquired the Barnett property from EOG Resources Inc.

“That was over $1 billion on acquisitions in three deals,” Whitmire noted. “We entered the Eagle Ford the same way we did the Bakken, in a no-op position to check it out and see if it was something for us. In the Bakken we determined it wasn’t, so we sold. In the Eagle Ford we determined it was, so we started buying more. It’s a concentrated position within Karnes County, and we’re drilling some really good wells.”

To get the company and its peers back to financial stability is going to take stronger prices.

Said Whitmire, “Hope is not a strategy, right? For the overall industry, prices have to go back up. Right now, I think that the Permian, the SCOOP/STACK, Eagle Ford and parts of the Bakken are really the only four places where people are making money and wanting to put a lot of rigs.

“But there’s a whole lot of oil and gas across the country outside of those four basins.

With supply not coming down as was expected with cuts from the Middle East and with demand being where it is, we are as an industry in a holding pattern outside of those four areas until something happens with prices.:

Until prices cooperate, the strategy will continue to be to sell assets if they can fetch a good price.

“We’re of the mindset that if someone had the right price, we would sell,” Whitmire said. “The Permian divestiture is an example of that…It’s something that we paid a little over $300 million

According to EV Energy Partners’ (EVEP) 2016 Form 10-K filed with the Securities and Exchange Commission, the credit facility for EnerVest’s publicly traded master limited partnership was amended in April 2016, which eased leverage covenants and added an interest coverage ratio. Specifically, the amendment decreased the borrowing base to $450 million. It also changed the senior secured funded debt-to-ratio covenant for EBITDAX, or earnings before interest, taxes, depreciation, depletion, amortization and exploration expenses.

The EBITDAX ratio covenant was amended so that it could be no higher than 3.0-1.0 for fiscal 2016 quarters and no higher than 3.5-1.0 for fiscal 1Q2017 and 2Q2017. For fiscal 3Q2017 and 4Q2017, the ratio is to be no higher than 4.0-1.0. Total funded debt to EBITDAX ratio covenant may no more higher than 5.50-1.0 for fiscal 1Q2018 and no higher than 5.25-1.0 for the fiscal 2Q2018 and 3Q2018. For fiscal 4Q2018 and thereafter, the ratio covenant may not exceed 4.25-1.0. At the end of 2016, EnerVest’s aggregate carrying amount of the senior notes due April 2019 was $341.9 million.

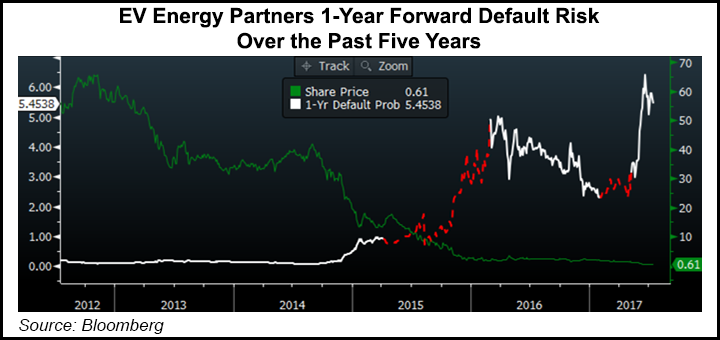

Standard & Poor’s Ratings Services currently has a “CCC+” long-term local issuer credit rating on EVEP, with a negative outlook. Similarly, Moody’s Investors Service gives them a long-term credit rating of “Caa2,” albeit with a stable outlook. Both ratings are firmly in junk territory. EVEP traded at 61 cents/unit at mid-day Tuesday, slightly above its 52-week low of 53 cents, and well off its 52-week high of $2.72.

Bloomberg pegs EVEP’s probability of default during the next 12 months at 5.45%.

During a presentation last year to investor Orange County Employees Retirement System Board in Santa Ana, CA, EnerVest’s asset impairments were detailed regarding Funds 12 and 13. The total impairment in fair market value between the two funds was $31.5 million at the end of 2015.

At the end of 2015, Fund 12 had fallen in fair market value year/year to $3.2 million from $14.3 million. Fund 13’s value had declined to $6.5 million from $26.9 million.

© 2024 Natural Gas Intelligence. All rights reserved.

ISSN © 2577-9877 | ISSN © 1532-1266 | ISSN © 2158-8023 |