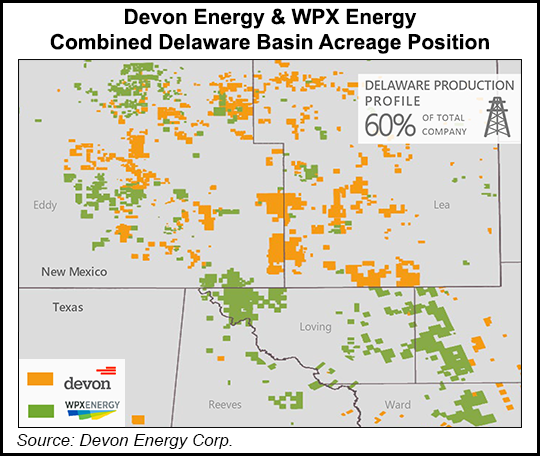

Devon Energy Corp. has raised its production guidance, lowered exploration costs and set its sights on expanding its hold in the Permian Basin, CEO Dave Hager said Friday.

The Oklahoma City independent in its third quarter results showcased how it’s managed to not only hold things together but improve since the sharp industry downturn in the second quarter.

For the second consecutive quarter, Devon increased its full-year 2020 oil production forecast to 152,000-154,000 b/d on better-than-expected well productivity and strong base production performance.

“Our teams are responding to a challenging operating environment by delivering results that continue to exceed production and capital efficiency targets, while successfully driving down per-unit operating costs and...