Markets | NGI All News Access | NGI Data

August Natural Gas Futures Eke Out Modest Gain on Cooling Demand Expectations

Ongoing expectations for above-normal temperatures and strong cooling demand through July and beyond nudged August natural gas futures higher Tuesday.

The August Nymex contract rose seven-tenths of cent day/day and settled at $1.746/MMBtu. September, however, decreased 1.0 cent to $1.787.

NGI’s Spot Gas National Avg. declined 4.5 cents to $1.675.

While the latest forecasts lack some of the heat intensity found in outlooks last week, Bespoke Weather Services continues to view this month as on pace to edge out July 2011 as the hottest July on record, as measured by total gas-weighted degree days.

“We are lacking extremes in any one given region, as this month is being defined mostly by persistence” and wide “coverage of above normal temperatures rather than a pattern that is setting daily records in many locations,” the forecaster said. However, “the level of cooler changes we saw over the weekend make it seem as though the pattern is not as hot as it actually is” and “we still expect the hotter than normal pattern to roll on into August, given the consistency of the La Niña base state present in the atmosphere.”

That should bode well for cooling demand.

“The coming pattern is still a hotter than normal one, with national cooling degree days solidly above normal the next 15 days, especially so this weekend and next week,” NatGasWeather said.

However, the firm said, weak liquefied natural gas (LNG) exports remain a drag and continue to keep price advances in check.

The direction of LNG export demand, hampered by continued spread of the coronavirus and uncertainty about economic activity driving energy demand in Europe and Asia, remains highly uncertain.

Virus cases are mounting anew in the United States and globally, forcing some governments to impose new restrictions that could curtail activity and could further hinder the need for LNG and commercial energy demand in general.

A “revival of increased restrictions after two months of non-stop economic reopening” is weighing on markets broadly, Raymond James & Associates Inc. analysts said.

The worry is that a pullback would not only stall natural gas demand but further freeze conditions near those experienced in April, the first full month that the pandemic gripped the Lower 48.

U.S. natural gas production declined by 2.6 Bcf/d in April, while domestic crude fell by 670,000 b/d, the U.S. Energy Information Administration (EIA) said on Tuesday. “Production declines of that magnitude usually arise only in natural disasters such as hurricanes,” the EIA said. The drop in U.S. gas production was the largest monthly decrease since Hurricane Isaac-related shut-ins in August 2012.

Heading into trading Tuesday, Bespoke said, production was down about 0.5 Bcf and LNG volumes were up slightly to a 3.5 Bcf. Exports to Mexico were up modestly, but overall, LNG levels are still well below pre-pandemic levels.

That backdrop, combined with the weather outlook, gives “us a slightly stronger balance picture day/day.” The firm added, however, that “it is possible that the market fears a weak number in this week’s EIA storage report,” as well.

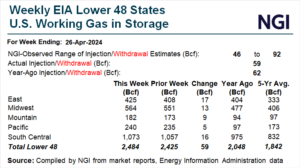

The EIA last week reported an injection of 56 Bcf into storage for the week ending July 3, coming in slightly below average estimates and marking the second consecutive week of sub-100 Bcf builds. Bespoke is looking for a build of 48 Bcf for the report this Thursday, which will cover the week ended July 10.

Cash Called Lower

Spot prices fell in every region of the country Tuesday. While lofty summer temperatures continue to permeate the Lower 48, near-term heat forecasts eased modestly.

“A small cool change is made to the forecast from the Midwest to the Mid-Atlantic, which comes on model trends for wetter conditions in these areas,” Maxar’s Weather Desk said. Otherwise, the forecaster added, it expects “widespread coverage of above normal temperatures.”

SoCal Citygate, which lost 31.5 cents day/day to average $1.980, led the decline.

Elsewhere, decreases were generally modest. Kern Delivery fell 6.0 cents to $1.880, while Opal lost 6.0 cents to $1.585.

PNGTS lost 3.5 cents to $2.540, and Chicago Citygate shed 4.5 cents to $1.665.

On the pipeline front, Northern Natural Gas said it plans to conduct station maintenance in its field area starting Wednesday and continuing through July 23, limiting up to 142 MMcf/d of receipts on the most impacted days. Genscape Inc. said the allocation groups impacted are Brownfield North Group (deliveries representing northbound flow), Mitchell to Gaines (receipts onto the pipeline), and Pampa North (deliveries representing northbound flow).

On Wednesday and Thursday (July 15-16), “we could see receipts onto the pipeline restricted by up to 142 MMcf/d at Mitchell to Gaines. Over the past 14 days, Mitchell to Gains has averaged 456 MMcf/d and maxed at 462 MMcf/d. Operating capacity will be at 320 MMcf/d for July 15 and July 16,” Genscape said.

From Thursday to July 23, Genscape said northbound flow could be “restricted by up to 50 MMcf/d at Pampa. Over the past 14 days, Pampa North has averaged 303 MMcf/d and maxed at 363 MMcf/d.” Operating capacity is set to be 314 MMcf/d for Thursday through July 23.

© 2024 Natural Gas Intelligence. All rights reserved.

ISSN © 1532-1231 | ISSN © 2577-9877 |