E&P | NGI All News Access | NGI The Weekly Gas Market Report

Chesapeake Mantra Changes from ‘No Acre Left Behind’ to ‘No Barrel Left Behind’

Doug Lawler jumped into the driver’s seat at Chesapeake Energy Corp. last June, gassed up by a land-rich portfolio but slowed by a poorly-running cash generator. Asset sales and spinoffs continue, to improve the balance sheet and more nimbly compete in the onshore.

At the annual analyst day Friday, Lawler attempted to make one thing clear: Chesapeake is no longer its co-founder’s company.

Lawler, a rising Anadarko Petroleum Corp. executive, accepted the top job at Chesapeake one year ago, but the decision was not without peril (see Daily GPI, May 21, 2013). Still smarting following apparent indiscretions by co-founder and CEO Aubrey McClendon, Chesapeake faced the scorn of investors and analysts. “There was significant potential that was not realized,” Lawler said. It was a “challenging time and a difficult time.”

Personnel were laid off. Budgets were cut. Staff members were anxious. Shareholders were more anxious. It’s time to put all of that aside, he said.

“The focus in the past, and the strategic initiatives in the past, had been to make sure we captured land, held the land for future value. The focus today is that we’re not going to leave a dollar behind. We’re not going to leave a barrel behind. Whereas in the past, it might have been, ‘we’re not going to leave an acre behind.'”

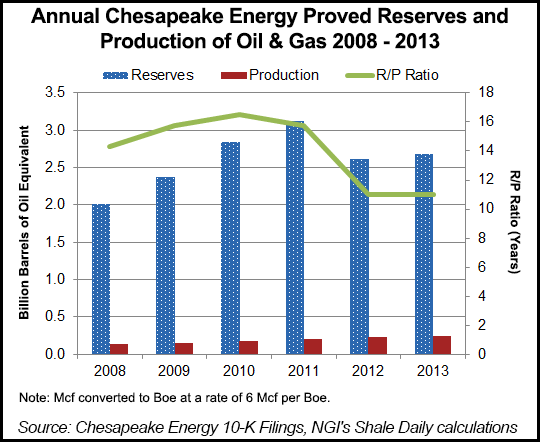

Chesapeake’s ability to produce oil and gas never has been an issue, said the CEO. What wasn’t clear was the financial performance.

CFO Nick Del’Osso, who also served under McClendon, told analysts that complexities have been cleaned from the balance sheet to give shareholders more transparency. “We’re absolutely focused on it, and we’re going to be driving for performance improvement for all future periods,” he said.

The credit ratings agencies also are recognizing the changes. Fitch Ratings last Wednesday revised Chesapeake’s outlook to “positive” from “stable” and affirmed its long-term issuer default rating “BB-”. Standard & Poor’s Ratings Services on Friday gave Chesapeake a “two-notch upgrade” to “BB+”.

“I think we’ve noted previously that complexity around here is coming down,” Del’Osso said. “The most complex thing about this company was that you couldn’t tell what we were going to look like until we delivered on the growth…”

Don’t judge Chesapeake by the past, Lawler urged.

“It’s really easy to look at this company and…say, ‘what’s wrong with Chesapeake? Let’s find a hole. Let’s poke at this, let’s poke at that.’ What we’re trying to do is demonstrate to you that I believe sentiment in the investment community is going to be, ‘let’s look at what’s right with Chesapeake.’ I…wouldn’t want to be one of those on the short end of not having confidence in this company.”

There is much more to do to fuel the production and earnings growth engine. Chesapeake plans to continue to sell more of its non-core properties or find other ways to create value, said Lawler.

The oilfield services business — currently conducted through subsidiary Chesapeake Oilfield Operating LLC (COO) — will be spun off to shareholders, a plan that was launched in February. COO filed a Form 10 with the U.S. Securities and Exchange Commission and expects to update it in the coming weeks (see Daily GPI, March 17).

Once the spinoff, to be named Seventy Seven Energy Inc., is completed, about $1.1 billion of consolidated debt would be eliminated from the balance sheet. The spinoff and recapitalization transactions should be completed by the end of June.

Chesapeake also is transferring ownership in a subsidiary, CHK Cleveland Tonkawa LLC, to an undisclosed owner group. The proposed transaction, set for completion in the third quarter, would eliminate $1 billion of equity and $160 million of balance sheet liabilities.

Also to be sold are producing assets in southwestern Oklahoma, East Texas and South Texas. The Texas properties have associated volumetric production payments. Chesapeake expects to receive about $310 million in cash proceeds combined from the three sales.

An acreage package in southwestern Pennsylvania (a dry gas area) that has “minimal associated production” also is being readied for sale, as is a portion of acreage in Wyoming’s Powder River Basin. Those transactions should net about $290 million.

All together with other sales proceeds received as of May 7, total divestitures year-to-date would be more than $4 billion.

“We expect that the transactions we are announcing…will result in a net leverage reduction to Chesapeake of nearly $3.0 billion, while only reducing our 2014 production by 2% and our operating cash flow by $250 million,” said Lawler. “Further, these transactions would reduce Chesapeake’s 2014 interest expense and dividend payments by approximately $70 million and eliminate $200 million of projected capital expenditures for the remainder of 2014.”

Even with the big sales packages, Chesapeake is estimating that 2015 production would be 7-10% over 2014. Management also believes it can deliver the production growth with total capital expenditures of $5.5-6.0 billion. The five-year annual growth target is set at 7-9%.

Tudor, Pickering, Holt & Co.’s Matt Portillo moved the stock to “hold” from “trim” and increased the firm’s model for proved, probable and possible net asset value by about $2.00 to $27.00/share.

“We continue to believe Chesapeake likely needs another year of restructuring to fully right the ship but they continue to take steps in the right direction to improve financial flexibility,” Portillo said. “The spin or sale of southern Marcellus/dry Utica a clear sign leadership is trying to unlock value where possible…

“Management has done an admirable job of working to simplify a complex financial organization burdened by years of onerous contract commitments which were used to finance acreage acquisitions during the land boom from 2008 through 2012. These contracts will continue to weigh heavily on the company’s netback as midstream and marketing commitments increase from $1.55 billion in 2014 to a peak of $1.95 billion in 2017 but we estimate that cost per Mcf should peak in 2015 as volume growth will start to offset the absolute dollar increase.”

On Monday, Wunderlich Securities Inc.’s Jason Wangler was also enthused about the progress.

“We believe Chesapeake remains a compelling value given it trades at 3.5x versus peers at 5.2x and, given its initiatives, we look for multiple expansion as well as incremental value from the spin-off of the oilfield services business that is not included in our estimates but could possibly add 10%-plus to an investor’s return given a potential $2.5 billion equity value,” Wangler said.

© 2024 Natural Gas Intelligence. All rights reserved.

ISSN © 2577-9877 | ISSN © 1532-1266 | ISSN © 2158-8023 |