Markets | NGI All News Access | NGI The Weekly Gas Market Report

Column: Solving the Natural Gas Supply Crunch in the Yucatan Peninsula

Editor’s Note: NGI’s Mexico Gas Price Index, a leader tracking Mexico natural gas market reform, is offering the following column as part of a regular series on understanding this process, written by Eduardo Prud’homme.

Prud’homme was central to the development of Cenagas, the nation’s natural gas pipeline operator, an entity formed in 2015 as part of the energy reform process. He began his career at national oil company Petróleos Mexicanos (Pemex), worked for 14 years at the Energy Regulatory Commission (CRE), rising to be chief economist, and from July 2015 through February served as the ISO Chief Officer for Cenagas, where he oversaw the technical, commercial and economic management of the nascent Natural Gas Integrated System (Sistrangas).

The opinions and positions expressed by Prud’homme do not necessarily reflect the views of NGI’s Mexico Gas Price Index.

The seasonality of energy demand in Mexico runs opposite to that of the United States. Although summer is the rainy and hurricane season, temperatures soar and air conditioning systems lead to peak electricity demand in Mexico between the months of June and August, straining generation capacity and natural gas supply.

Keeping the electric power and gas networks in balance during the summer season implies complex operational decisions. While the power grid is congested in parts of the country, gas inventories also drop. In a free market, marketing contracts and transportation capacity determines who receives gas and who does not; and price signals restore market equilibrium. But in a market in transition such as that of Mexico, authorities and operators still play a central role in the way energy demand is met.

In the recent past, energy policy has privileged gas supply to private users, that is, the industrial sector and distributors. The electricity sector has been the determining factor in whether gas flows to the rest of the economy. Essentially, in times of gas shortages, generation plants with dual technology options are asked to switch to a non-natural gas fuel. These switching events are not exempt from efficiency and economic losses, nor are they always easy to pull off from an operational standpoint, especially given their financial impacts.

Given the lack of consistent natural gas supply, over the past six years, state power company Comisión Federal de Electricidad (CFE) launched tenders for new pipelines connected to basins with abundant gas. CFE also ventured into commercialization activities with the aim of ensuring security of supply. CFE had been subject to a supplier, Pemex, who itself was a large consumer of natural gas and had its own commercial priorities, and this offered it a safeguard against unforeseen events.

Still, natural gas supply has remained inconsistent in Mexico, especially during the summer months, and this summer is no different. The vulnerability of the electricity and gas networks is especially critical in the Yucatán Peninsula, a region that has seen blackouts this year, and that for energy security purposes has characteristics that resemble an island.

Currently, the Yucatán Peninsula sources its natural gas from the Cactus and Nuevo Pemex processing centers. These processing plants are connected to the Mayakan gas pipeline, which crosses through the states of Campeche and Yucatán to the city of Valladolid. The 250 MMcf/d Mayakan pipeline is owned by France’s Engie, and is one of the oldest private pipelines operating in Mexico.

The gas produced in Cactus and Nuevo Premex is principally injected into the Sistrangas national pipeline network to meet the demand of the oil sector in the southeast, and to contribute to natural gas supply in the center of the country, with the secondary option of it going to power plants and industry in the Yucatán. This practice has left gas users unhappy in the Yucatán, who complain with some justification of being affected by a centralist vision.

Natural gas-fired generation in the peninsula belongs either to CFE, or to private companies that deliver electricity to CFE under the Independent Power Producers (IPP) scheme. Mayakan has capacity to meet the demand of these plants. If it does not, it is because gas availability at Mayakan’s only injection point typically is around 70 MMcf/d. Some days natural gas injection into the pipeline is non-existent, events that are more common since the explosion of the Abkatun Alfa marine platform offshore Mexico’s southeastern coast in 2015.

There are also additional quality problems that lead the carrier to refuse gas reception. The gas that Pemex delivers in Cactus can have nitrogen levels of up to 16%, when the permissible limit is 8%. Finding water or traces of hydrogen sulfide in the gas stream is also common. If this same gas is accepted into the Sistrangas, it is because not doing so would limit available volumes and affect system balance.

The fact that the Mayakan pipeline was related to the activities of CFE, and not of Pemex — which developed the infrastructure for the national pipeline system — explains why it’s not connected to the Sistrangas.

So, lacking injection options, and with no operative flexibility, Yucatán is an area that requires innovative natural gas solutions.

Over the years, analysts have studied the technical and economic feasibility of importing liquefied natural gas (LNG) directly into the area. Several companies have promoted initiatives to build an LNG terminal or floating storage and regasification units (FSRU) offshore Campeche or the Yucatán. However, industrial, residential and commercial consumption do not provide financial viability for any sort of project of this sort without there being an active policy of government promotion, or a long-term financial commitment.

Power generation projects based on LNG cargoes arriving in the peninsula might offer a solution. The problem is that there is sufficient installed capacity in the Yucatán and so the only viable sponsor would be CFE with its existing plants.

Another solution is LNG via an FSRU piped into the Sistrangas, with Pemex together with the CFE making a commercial commitment to finance the project. Plans were actually advanced for an FSRU at Pajaritos in Veracruz, though this plan was scrapped by the new administration.

The new government’s flagship project, the Dos Bocas refinery, makes it likely that an FSRU might be developed there in conjunction with the complex. If the gas is used for Pemex and CFE consumption, the project makes sense as a business decision that seeks continuity of supply. If the gas is marketed to other end users, the project would mean a clear reversal towards centralizing transactions and removing power from market players.

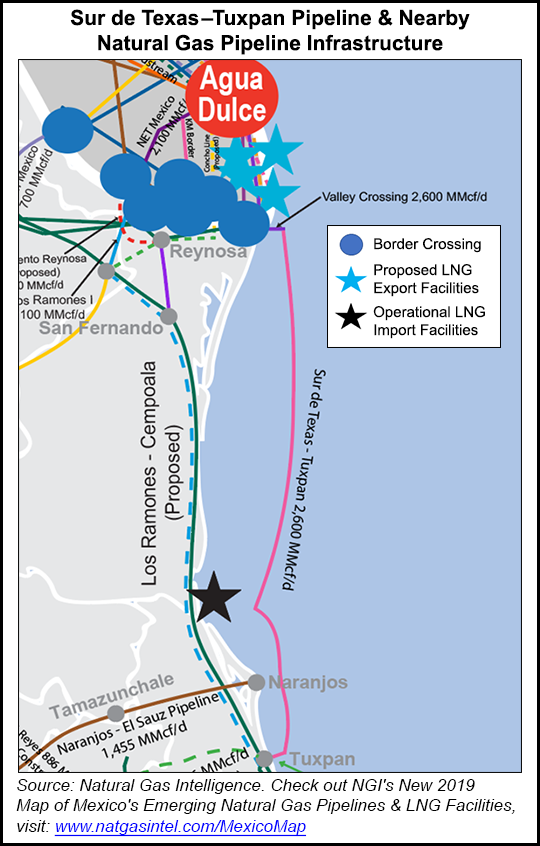

The solution for Yucatán gas supply as designed in the five-year plan prepared by pipeline operator Cenagas was built around the startup of the 2.6 Bcf/d Sur de Texas-Tuxpan marine pipeline. The 500 MMcf/d Sistrangas connection at Montegrande would allow natural gas coming in from Agua Dulce to displace volumes of gas produced in Pemex processing centers.

Cactus gas could then be re-routed to the Yucatán. To improve operational flexibility, the Sistrangas and Mayakan pipelines would be connected to mitigate the risk of unscheduled gas processing shutdowns. Basically, the Yucatán would be served by imported gas through an operational exchange.

The official position of the government of Mexico is that the flow of natural gas to the Yucatán Peninsula should increase starting this month. This would be plausible if the reconfiguration of the Cempoala compression station were complete, which would allow for gas flows south, the marine pipeline began commercial operations, and the Sistrangas started to receive gas at the Montegrande interconnection.

However, the Sur de Texas-Tuxpan pipeline remains stalled as CFE seeks to change its contract terms with the developers of the pipeline, while the Montegrande interconnection is not yet recognized by Cenagas. The Mayakan is also still not connected to the Sistrangas. That said, if capacity allocation issues on the Sistrangas are taken care of, the infrastructure is in place to allow for the entry of gas to improve the natural gas balance in the southeast.

If indeed there are no technical impediments to receiving natural gas, we can infer that the CFE is simply not accepting gas at Montegrande. It may well be a legal strategy complementary to the publicly announced arbitration. In this scenario, Cenagas as operator of the Sistrangas should have the ability to start receiving gas on behalf of other users. This could well happen since the entry into technical operation of the marine pipeline is the responsibility of the developers. As a holder of an operating permit, it is enough to notify the energy regulator CRE of being ready to carry out activities.

All this to say that a happy ending seemed within reach for the supply problems in the Yucatán, and yet the summer of 2019 is again one of natural gas shortages and a good share of drama.

© 2024 Natural Gas Intelligence. All rights reserved.

ISSN © 2577-9877 | ISSN © 2577-9966 | ISSN © 1532-1266 |