NGI Data | Markets | NGI All News Access

No Fireworks for Natural Gas Futures as Slide Continues

Natural gas futures sold off for a third straight session Tuesday, with weak physical prices, cooler forecast trends and the prospect of another above-average inventory build all helping to keep the bulls on the sidelines. Meanwhile, calls for more heat and humidity along the East Coast couldn’t stir up a stagnant spot market; the NGI Spot Gas National Avg. slumped 5.5 cents to $1.875/MMBtu.

The August Nymex futures contract settled at $2.240 Tuesday, off 2.7 cents. The front month traded as high as $2.297 and as low as $2.232. Further along the strip, September fell 2.5 cents to settle at $2.217, while October settled at $2.249, down 2.7 cents.

Heading into Tuesday’s session, Bespoke Weather Services noted a “divergence in signals,” including cooler weather trends but tightening in the daily balance indicators, including stronger power burns.

“Given the heat, however, on a weather-adjusted basis, the burns remain weaker than in early June,” Bespoke said. “Nonetheless, the market used the data to attempt a rally, as the August contract nearly touched the $2.30 level” Tuesday morning. “The winter strip was quite weak, however, and then cash prices began to weaken as well.

“…It has been a little odd to see no improvement in the weather-adjusted burns with this leg lower in price” from the $2.35-2.40 area. “Perhaps it comes, but until it does, it will be difficult to sustain a rally unless the heat can crank back up more than we expect in the medium range.”

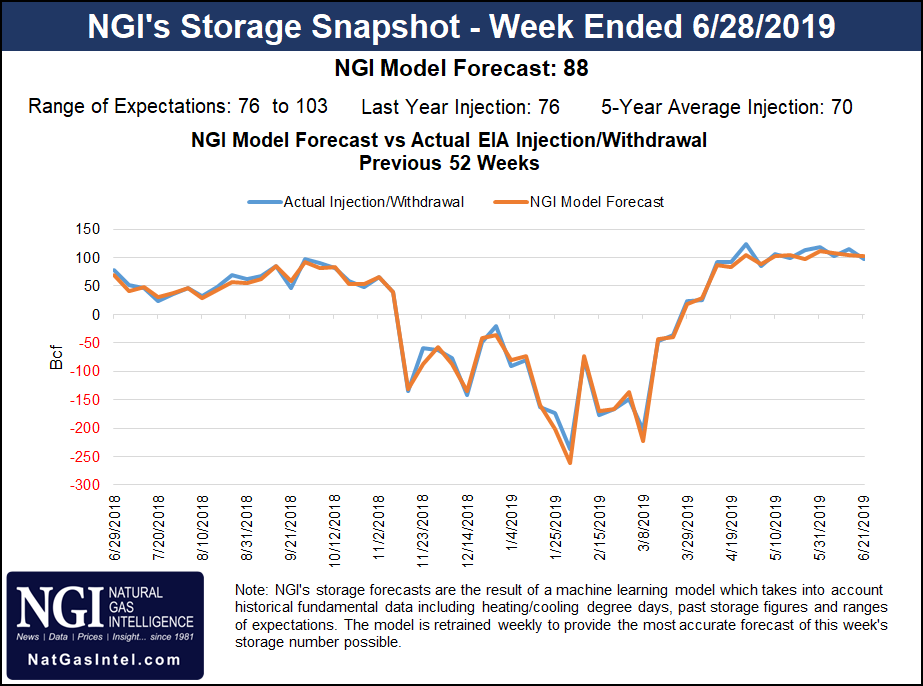

Predicting that the number would come in looser than last week’s 98 Bcf build, Bespoke said it was holding its sentiment at neutral ahead of this week’s Energy Information Administration (EIA) storage report.

Wednesday’s EIA report — scheduled for release a day earlier than usual because of the Fourth of July holiday — is expected to show a larger-than-average build but one well shy of the triple-digit injections recorded earlier in the refill season, according to estimates.

A Bloomberg survey Tuesday showed a median prediction of 83 Bcf based on seven estimates. A Reuters poll pointed to an 85 Bcf injection, with a range of 76 Bcf to 94 Bcf. Intercontinental Exchange EIA Financial Weekly Index futures settled Monday at 82 Bcf. ION Energy analyst Kyle Cooper called for an 87 Bcf build. NGI’s model predicted a build of 88 Bcf.

Last year, EIA recorded a 76 Bcf injection for the period, and the five-year average stands at 70 Bcf.

Energy Aspects issued a preliminary estimate for an 80 Bcf build, based on a 2.5 Bcf/d increase in power burn week/week, offsetting a 0.4 Bcf/d increase in domestic supply.

“From here on we expect injection rates to fall precipitously,” the firm said, noting that its power burn models show daily rates approaching 40 Bcf/d for the first few days of July. But the heat “is also closely aligned with the potential demand dampening effect from the Fourth of July holiday.”

Energy Aspects said it expects “record gas burn” in July, but this comes as production has also been running above the weekly highs observed last December.

“With news on the arbitration process on Sur de Texas-Tuxpan, a scenario in which cross-border exports increase dramatically looks off the table,” according to the firm. “The fundamental backdrop is still looking quite loose, with our estimates through the week of July 12 indicating it is running 5 Bcf/d looser on average. Given the very short bias of the market, however, any massive step up in weather could leave the market exposed to an overshoot.”

Meanwhile, data issues related to changes in Transcontinental Gas Pipe Line (Transco) reporting, which appeared to erroneously show a large day/day production drop out of Pennsylvania Monday, were mostly resolved as of early Tuesday, according to Genscape Inc.

“We believe the initial postings of bad data were a contributor” in Monday’s declines in the Nymex futures, analyst Josh Garcia said. For the first few cycles of Monday’s gas day, Transco posted “incomplete” data that caused “supply and demand sums to fall significantly day/day. Some major locations that were posting zeroes include the Lighthouse Road delivery point to Sabine Pass LNG and all production points in Northeast Pennsylvania, causing an initial production drop of around 3.6 Bcf/d day/day.”

While the data issues appeared to be mostly resolved as of early Tuesday, “we are advising clients…to remain alert, as there is potential for additional data issues as Transco sorts through the process of renaming and reclassifying points in its reports,” Garcia said.

As for the overall Lower 48 supply picture, Genscape’s latest modeling Tuesday showed production resuming steady growth following maintenance- and weather-related impacts this spring. The firm is forecasting further output gains moving forward.

“With the dust having settled on first-of-month and recent-day production revisions, we see production reached 89.87 Bcf/d on Sunday (June 30),” Genscape senior natural gas analyst Rick Margolin said. “This was the highest single-day production print since Nov. 30. The number helped close the month of June at an estimated average of 88.53 Bcf/d. This was just 0.15 Bcf/d below our forecast due to unplanned outages in Ohio and storming and flooding in Oklahoma and East Texas.

“Production through much of the spring had gone through fits and starts and underperformed due to a prolonged maintenance season and weather challenges,” Margolin said. “However, since the start of June, production has resumed following steady growth rates, with end-of-month output averaging more than 1 Bcf/d higher than month-start.”

Genscape forecasts show production growing more than 0.7 Bcf/d month/month through July and August, with volumes potentially cresting 91.2 Bcf/d by the end of the summer.

If forecasts are anything to go by, residents in the eastern United States will be cranking up their air conditioners this week. But the spot market response to the prospect of rising temperatures has been mostly tepid, a trend that continued Tuesday. After selling off Monday, benchmark Henry Hub held steady Tuesday, slipping 0.5 cents to average $2.250.

“A stationary frontal boundary draped from the Great Lakes to the Central Rockies will continue to be a focus for showers and thunderstorms” over the next couple of days, according to the National Weather Service (NWS). “Strong to severe thunderstorms are possible, along with locally heavy to excessive rainfall.”

NWS called for the eastern United States to see increasing heat and humidity through the middle of the week.

“Daytime highs are forecast to be in the mid to upper 90s from the Southeast to the Mid-Atlantic, with heat indices making it feel even hotter,” the forecaster said. “Moisture rounding the ridge will also result in daily afternoon chances for showers and storms from the Southern Plains to the Mid-Atlantic.”

Despite the hot and humid conditions expected in the region, Southeast price moves were mixed. Transco Zone 4 eased a penny to $2.240. Further up the East Coast, Transco Zone 6 NY slid 1.5 cents to $2.110.

Prices throughout much of the middle third of the Lower 48 saw only small day/day adjustments Tuesday. Down in Texas, Katy added a penny to $2.150.

Further west, meanwhile, points throughout the Rockies and California posted double-digit discounts.

The NWS was calling for an upper level trough over the western United States to “keep conditions unsettled” over the next couple days, with near or below normal temperatures.

In California, PG&E Citygate tumbled 31.0 cents to $2.030, while further south, SoCal Citygate shed 17.0 cents to average $1.865.

A combination of cooler temperatures and strong output from renewables has helped prevent price blowouts at SoCal Citygate so far this summer, even as the risk for natural gas supply shortages remains, according to Genscape.

Total gas demand in Southern California, reflected in flows on Southern California Gas, Kern River, Mojave and El Paso Natural Gas, averaged just 2.63 Bcf/d in June, the lowest June average since at least 2009. That followed record monthly lows recorded in April and May, Genscape’s Margolin said.

The cool temperatures have accompanied lower total power generation, calculated based on all of the California Independent System Operator (CAISO) territory, including imports. Total generation summer-to-date has been down about 1.2% compared with last year, Margolin said.

“However, gas generation is down an even greater amount at minus 7% (minus 7.4 GWh/d), and imports are down 14% (minus 20.2 GWh/d). Nuclear is up slightly summer-on-summer (plus 4%, or plus 2.0 GWh/d), but renewables are up 24.8 GWh/d, a 9% year/year increase,” he said.

The strong renewables output can be traced back to a strong year for hydroelectric generation and sustained growth in solar. Hydro output in the region this summer is currently running 37% above last year’s levels and 32% higher than the 10-year average, while solar output is running at double the rate observed just two summers ago, according to Margolin.

“Solar now accounts for 16% of the total CAISO stack, and this summer all renewables combined are accounting for 52% of the stack,” he said.

© 2024 Natural Gas Intelligence. All rights reserved.

ISSN © 1532-1231 | ISSN © 2577-9877 |