October Natural Gas Firms on Sustained Heat Keeps; Spot Gas Mixed Ahead of Labor Day Weekend

Another hotter turn in weather models lifted October natural gas prices for a third day Friday as summer heat is expected to linger a little longer into September than originally forecast. The Nymex October gas futures contract settled at $2.916, up 4.2 cents on the day. Increases of close to 4 cents were also seen throughout the winter 2018-2019 strip.

Spot gas prices were mixed but mostly higher despite the extended Labor Day weekend as the looming heat wave was expected to start building late in the weekend and provided support to some prices. The NGI National Spot Gas Avg. rose 4 cents to $2.68.

As far as the weather, the European model had been the hottest of all the datasets, but the Global Forecasting System (GFS) model trended notably hotter overnight Thursday to better match it, according to NatGasWeather. Each model slowed the weakening of the hot ridge over the eastern half of the country during the second week of September, which would add several cooling degree days/Bcf in demand. Meanwhile, the European model was further hotter trending to remain the hottest of the models, the forecaster said.

“Clearly, bulls have regained momentum ahead of the long Labor Day Holiday weekend,” NatGasWeather said.

Bespoke Weather Services had been looking for resistance around $2.92 to hold firm following Thursday’s Energy Information Administration (EIA) reported storage injection “as clearly the market has loosened and supply remains near record highs.

“Eventually, with these loose balances and a weak strip, we would see this weather-driven rally being a strong shorting opportunity, but current forecasts are just too bullish to expect any reversal yet, and we need models to pick up on week 3 cool risks first,” Bespoke chief meteorologist Jacob Meisel said.

NatGasWeather said Friday’s trade could be quite telling to true market sentiment and whether bulls would buy the dip created going into September contract expirations. “Every day late summer warmth holds on, the less opportunity record production will have in improving deficits this shoulder season,” the forecaster said.

Indeed, much of market fodder in recent months has been on growing production, which set a fresh record a few days ago and is expected to continuing climbing as infrastructure goes online later this year. Many market observers have made no secret of their theories that the additional supplies would help fill lagging storage inventories, which are now expected to expand even further thanks to the lingering heat across the country.

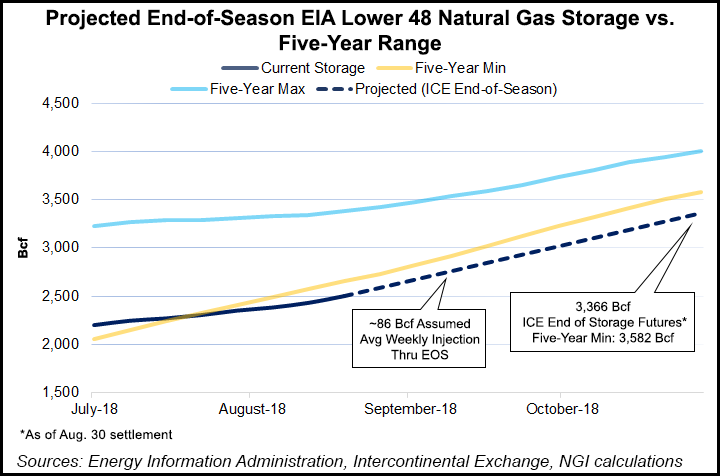

As of Friday, Intercontinental Exchange showed end-of-season storage stocks sitting at 3,366 Bcf, a 10 Bcf increase week/week. The gain reflected increased confidence that once summer heat finally fades, production will be able to tighten the storage deficits. Even so, market participants lowered their end-of-season estimates from Wednesday to Thursday, likely because of the hotter trending weather outlooks.

To reach an end-of-October inventory level of 3,366 Bcf would require weekly injections to average 86 Bcf through the remainder of the injection season.

As Mobius Risk Group noted, pre-winter inventory is essentially guaranteed to start with a 400 Bcf-plus storage deficit. “The statistical relevance here is that a 400 Bcf deficit nullifies the first 2.6 Bcf/d of year-over-year production growth,” the Houston-based company said.

Shoulder season is fast approaching and week/week, as well as year/year, volatility can become pronounced as summer demand begins to wane, Mobius said. The EIA’s reported 70 Bcf build was a “whopping 38 Bcf” more than at the same time last year. “Were the deficit not so large, this might have caused sell-side interest to dominate the market, but at 646 Bcf versus the same week last year, there is still a sizable shock absorber for the periodic larger-than-normal build,” Mobius analysts said.

Meanwhile, Tudor, Pickering, Holt and Co. analysts said incremental color from Cheniere Energy Inc. regarding the Sabine Pass liquefied natural gas (LNG) facility Train 5 and Corpus Christi Train 1 reaffirmed first LNG in 4Q2018, but it also indicated limited cargoes through year’s end, “confirming suspicions that demand tailwinds are likely not felt until 1Q2019.”

Spot Gas Mostly Higher Ahead Of Labor Day

Despite the extended holiday weekend, spot gas prices were mixed in Friday trading as a heat wave was expected to start building late in the weekend and then get the first week of September off to a hot start.

National demand eased Friday as a cool front advanced across the Mid-Atlantic and Northeast, easing highs back into the 70s and 80s. A swing back to stronger-than-normal national demand was expected to occur later in the weekend through next week as hot high pressure returned over most of the United States, except over portions of the West, according to NatGasWeather.

The result is daytime temperatures in the mid-80s and 90s again becoming widespread across the Great Lakes, Mid-Atlantic and Northeast, with hot and humid conditions remaining across the southern part of the country, the forecaster said.

“The data continues to be slower in how fast the upper ridge weakens Sept. 7-11 and where the GFS and European models have been hotter trending the past couple days, stalling the fizzling of late summer heat across the eastern, central and southern U.S.,” NatGasWeather said.

Trading action on Friday was a direct reflection of where the most intense heat was forecast to be concentrated. California markets were a sea of red as the volatile SoCal Citygate tumbled more than 50 cents to $4.25, while Malin slipped less than a nickel to $2.36.

Moderate declines were also seen in the Rockies, where El Paso-Bondad dropped a dime to $2.10, and Northwest S. of Green River fell 6 cents to $2.20.

Interestingly, most Appalachia points also declined despite the hot weather heading into the region. Dominion South fell 6 cents to $2.52, while Transco-Leidy Line dropped 13 cents to $2.41. Tennessee zone 4 Marcellus plunged 25 cents to $2.13.

Meanwhile, other points on the Tennessee Gas Pipeline posted sharp increases as the pipeline on Friday issued an operational flow order “Daily Critical Day 1” for Tuesday (Sept. 4) for all balancing parties downstream of Station 245 on the 200 Line and downstream of Station 325 on the 300 Line.

All delivery point operators downstream of Station 245 on the 200 Line and downstream of Station 325 on the 300 Line were required to keep actual daily takes out of the system equal to or less than scheduled quantities regardless of their cumulative imbalance position, the company stated. All receipt point operators downstream of Station 245 on the 200 and downstream of Station 325 on the 300 Line also were required to keep actual daily receipts into the system equal to or greater than scheduled quantities regardless of their cumulative imbalance position.

Tennessee zone 4 200L spot gas rose 14 cents to $2.77, while Tennessee zone 6 200L spot gas jumped more than 30 cents to $3.09.

Meanwhile, Columbia Gas spot gas prices also nudged out a small 3-cent gain to $2.71 as maintenance beginning Saturday (Sept. 1) on the pipeline’s WB system was to restrict operational capacity through the Lost River compressor station (CS) to various levels through Sept. 10: 1,050 MMcf/d Sept. 1-2; 1,000 MMcf/d Sept. 3-5; 845 MMcf/d Sept. 6-7; and 945 MMcf/d Sept. 8-10.

Flow through the Lost River CS has mirrored operating capacity closely, with a 30-day average utilization of 93%, average nominations of 960 MMcf/d and a max of 1.17 Bcf/d, according to Genscape Inc. “The operational capacity restrictions during the maintenance are likely to reduce scheduled nominations correspondingly,” Genscape natural gas analyst Vanessa Witte said.

In addition, the pipeline’s VB system is set to undergo maintenance beginning Monday through Friday, which would reduce operational capacity to the Loudoun LNG interconnect with Dominion Cove Point to 350 MMcf/d from Monday through Wednesday, and to 225 MMcf/d on Thursday and Friday.

Average nominations to Cove Point at Loudoun were around 400 MMcf/d, excluding prior maintenance from Aug. 7-21, when the Loudoun LNG interconnect was completely shut-in, Genscape said. During this event, Transcontinental Gas Pipe Line picked up the remainder of flows to Cove Point at the Pleasant Valley location, “and it is likely the current maintenance will produce a similar outcome,” Witte said.

Elsewhere across the country, Southeast pricing location put up gains of more than a dime in some areas, while Louisiana and East Texas posted smaller gains.

© 2024 Natural Gas Intelligence. All rights reserved.

ISSN © 1532-1231 | ISSN © 2577-9877 |