Markets | NGI All News Access | NGI Data

Warmer May Temps Boost Weekly Natural Gas Spot Prices; Storage Deficits Support Futures Bulls

Some above-normal May temperatures offered a slight boost for natural gas spot prices during the week ended Friday, while storage deficits helped bulls gain ground in the futures market despite a larger-than-average injection; the NGI Weekly National Spot Gas Average climbed 7 cents to $2.38.

Points across the Midwest and Gulf Coast finished higher on the week as forecasts showed the mercury rising to A/C levels at major population centers in those regions. Chicago Citygate tacked on a dime to $2.49, while Houston Ship Channel added 10 cents to $2.82.

Prices were mixed in the Northeast and Appalachia. A few points traded in an up-and-down pattern during the week amid reports of shoulder season maintenance disrupting pipeline flows in the region.

Transco-Leidy Line fell 66 cents to average 96 cents, with Tennessee Zone 4 Marcellus and Millennium East Pool posting similarly large declines. Transco Zone 6 New York shed 11 cents to $2.46.

In Canada, NOVA/AECO C continued its wild ride this shoulder season, adding 74 cents on the week to average $1.27 after trading in the negatives earlier in the month.

Analysts with Tudor, Pickering, Holt & Co. (TPH) attributed the strengthening at AECO to “a brief break from maintenance” allowing “volumes to flow uninhibited” on the Nova Gas Transmission Ltd. (NGTL) system. “We expect this strength to last until next Tuesday when another slug of maintenance kicks in, which likely keeps pricing weak into late June.”

Natural gas futures inched lower Friday after trading in a fairly narrow range, with the market continuing to piece together a storage picture that could see deficits persist deep into the summer. The June contract slid 1.2 cents to settle at $2.847 after trading as high as $2.870 and as low as $2.840. Week/week (w/w) June added a little over 4 cents after settling at $2.806 the Friday before.

“Yet again we saw another slow Friday trading day” after a larger trading range on Thursday when the Energy Information Administration (EIA) issued its weekly storage report, Bespoke Weather Services said. Like the Friday before (May 11), “the strip was more supportive, however, we also saw weather flip significantly more bearish through the day,” on bearish Global Ensemble Forecast System guidance “pulling prices off the $2.87 resistance level we had been watching, and then European guidance furthering these long-range cool trends that we expect to limit cooling demand into early June.”

The market appears “increasingly primed to rally on sustained heat,” which could arrive by mid-June. Although the potential for further gas-weighted degree day declines presents downside risk over the week ahead, with the market potentially testing $2.80 or even $2.75, according to Bespoke.

“From there, downside remains generally limited” particularly as the next week or two “we would expect mid-June heat risks to become more apparent,” the firm said. “Confidence is limited by this supportive strip still, and there certainly are bullish risks, but given softer daily burns and expectations of further cooling demand losses it would appear risk is skewed modestly lower” to start the upcoming week.

NatGasWeather.com said it expects most of the country to remain warm enough through early June to result in “upcoming builds being near five-year averages, essentially stalling deficits and failing to reduce them much over the next three to four weeks.

“We see this providing a bullish background state as the markets were expecting several builds to print greater than 100 Bcf, and that’s looking less likely as the next several come in closer to 80s to 90s Bcf,” keeping deficits close to minus 500 Bcf through the end of the month, NatGasWeather said. “So while production has set fresh records just about every month this year, it’s still not enough to meaningfully reduce deficits this shoulder season, at least not yet.”

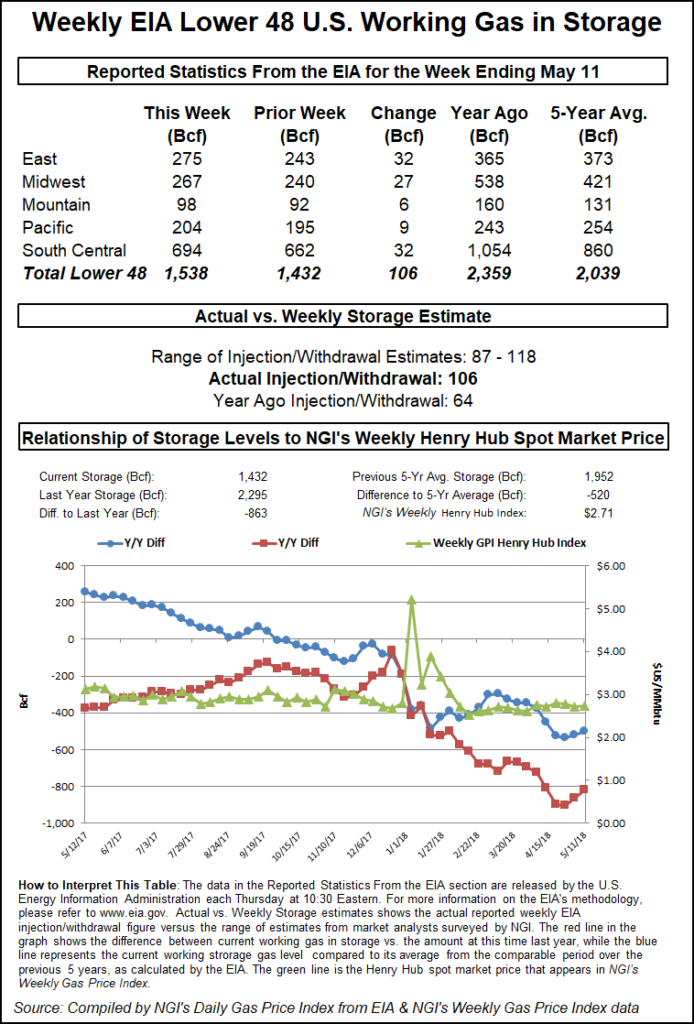

EIA reported a 106 Bcf injection into Lower 48 gas stocks for the week ending May 11, close to consensus estimates and larger than both last year’s 64 Bcf build and the five-year average 87 Bcf injection.

As the data rolled out at 10:30 a.m. ET, the June futures contract briefly traded as high as $2.811 and as low as $2.782 before returning to roughly the same $2.790-2.800 area it had traded in prior to the report. By 11 a.m. ET, June had climbed to around $2.820, up about a penny from Wednesday’s settle.

Prior to the report, surveys showed the market looking for a build close to the actual number. A Reuters survey had produced an average 105 Bcf build, with responses ranging from 99 Bcf to 118 Bcf. A Bloomberg survey had produced a median build of 107 Bcf, with responses ranging from 87 Bcf to 110 Bcf. ION Energy had called for a 103 Bcf build, while Price Futures Group had estimated an injection of 105 Bcf. Intercontinental Exchange EIA storage futures settled Wednesday at an injection of 105 Bcf.

The 106 Bcf build “does represent slight tightening from last week and is not as large as it could have been given how bearish weather was across much of the country,” Bespoke Weather Services said in a note following the report. “However, it similarly does not provide much fodder for bulls, confirming that last week’s bullish surprise may have been more of a one-off and current readings of market balance are accurate.

“Prices are reacting in their expected muted fashion; burns are looser today but have tightened over the past week, and production dips are keeping later contracts firm,” Bespoke said. “Prices may wander toward $2.75, but this print confirms range-bound trading for now.”

Total working gas in underground storage as of May 11 stood 1,538 Bcf, versus 2,359 Bcf a year ago and five-year average inventories of 2,039 Bcf. The year-on-year storage deficit shrank w/w from minus 863 Bcf to minus 821 Bcf, while the year-on-five-year deficit narrowed from minus 520 Bcf to minus 501 Bcf, EIA data show.

By region, the South Central region recorded a 32 Bcf build for the week, including 12 Bcf into salt and 19 Bcf into nonsalt, according to EIA. The East region also injected 32 Bcf, while the Midwest saw a 27 Bcf build. In the Mountain region 6 Bcf was injected, while 9 Bcf was refilled in the Pacific.

TPH said based on total degree days for the period the 106 Bcf build indicates the market is oversupplied on a weather-adjusted basis.

“Warmer-than-normal temperatures continue to be expected across the lower U.S.” as cooling demand appears likely to overtake heating demand, according to the TPH team. “If proven accurate, warm weather will become a boon for pricing as we enter the summer cooling season. Nationally, U.S. dry production failed to break past the 80 Bcf/d barrier, Mexican exports remain at around 4.3 Bcf/d” and liquefied natural gas exports were flat w/w at about 3.4 Bcf/d.

The 106 Bcf build is tighter versus the previous five years by 1.5 Bcf/d based on degree days and normal seasonality, according to Genscape Inc. analyst Rick Margolin said.

“Relative to the previous week, total power generation was up 17 average GWh. Total renewable generation was down 7 average GWh as wind was down around 9 average GWh w/w and nuclear generation up by 2 average GWh,” Margolin said. “Total thermal generation was up 24 average GWh w/w. Gas generation was up around 16 average GWh for an increase of 3.2 Bcf/d gas burn.”

Meanwhile, production increased by close to 1 Bcf/d day/day (d/d) Friday but couldn’t crack the 78 Bcf/d mark for the fourth straight day, according to Margolin.

“At the same time, demand is posting a nearly equal 0.9 Bcf/d d/d retreat ahead of the weekend,” he said. “The main driver is the Midwest, where nominated demand is down nearly 1 Bcf/d with ANR, NGPL, NNG and Panhandle all posting 0.2 Bcf/d d/d drops with temperatures coming back into seasonal norms.”

In the spot market, prices fell across markets in the West as Midwest points strengthened following recent declines; the NGI National Spot Gas Average slipped a penny to $2.33/MMBtu.

Midwest spot prices finished higher Friday after posting broad declines the past two trading days. Chicago Citygate gained back 9 cents to average $2.46 after giving up 11 cents in trading Thursday.

“Weather systems will bring areas of showers across the Rockies and Plains the next few days as well as cooler temperatures,” NatGasWeather said in its one- to seven-day outlook Friday. “It will be a touch cool over the Northeast with upper 50s and 60s, while wet over the Mid-Atlantic Coast and Southeast, but still rather warm with 70s and 80s.

“The Southwest and Texas will be very warm to hot with upper 80s and 90s for regionally stronger demand,” the firm said. “Next week will be warmer than normal across most of the country but still with areas of showers, especially over the West and Southeast.”

Prices were mixed in the Northeast and Appalachia heading into the weekend, with some points continuing a volatile pattern that has coincided with shoulder season maintenance in the region.

Transco Zone 6 New York shed 15 cents to average $2.46 after jumping 29 cents Thursday. Millennium East Pool dove 72 cents to $1.02 after adding 20 cents Thursday.

In the West, the import- and storage-constrained SoCal Citygate recorded another Friday decline ahead of a weekend expected to bring moderate demand for utility Southern California Gas (SoCalGas). SoCal Citygate plummeted 63 cents to average $2.06, while SoCal Border Averageshed 10 cents to $1.82.

SoCalGas was forecasting total system demand of right around 2 Bcf/d over the weekend, down slightly from actual demand of about 2.1 Bcf/d Thursday. The utility was forecasting weighted average temperatures in the mid-60s over the weekend.

Further upstream in the Rockies, prices at most points weakened by a nickel to a dime. Opal dropped 6 cents to $1.71, while Transwestern San Juan fell 15 cents to $1.64.

“Planned maintenance on Northwest Pipeline (NWPL) beginning Monday and lasting through Saturday (May 26) could disrupt over 150 MMcf/d of San Juan Basin outflows,” Genscape analyst Joe Bernardi told clients Friday. “NWPL will perform a hydrotest between its Moab and Cisco compressor stations in southeastern Utah, which will require these points to go to zero flow.

“These points typically bring San Juan molecules north, with an average throughput of 179 MMcf/d over the past month,” Bernardi said. “There has not been an equivalent NWPL maintenance event within recent years, but reroutes could occur onto Transcolorado, El Paso or Transwestern.”

© 2024 Natural Gas Intelligence. All rights reserved.

ISSN © 2577-9877 | ISSN © 1532-1258 |