Markets | NGI All News Access | NGI Data

Bullish Week for NatGas Futures Amid Tight Storage, Frigid Forecast; Spot Prices Weaken

Natural gas futures surged during the week ending Jan. 26 thanks to lean storage inventories and weather guidance showing the potential for a return of frigid temperatures in February. Cash prices weakened as temperatures moderated from the week before, and the NGI Weekly Spot Gas Average fell 64 cents to $3.42/MMBtu.

East Coast prices eased off recent weather-driven gains. Algonquin Citygate dropped $1.12 to $8.92, while Transco Zone 6 New York tumbled $3.83 to $3.82. Transco Zone 5 saw its weekly average cut in half to $3.71.

Gulf Coast prices posted some strong day/day gains during the week as futures rocketed higher, but most points in Louisiana and Texas declined from the week before, when a rare winter storm dropped snow and ice across the South and Southeast.

Henry Hub finished the week at $3.43, down 45 cents week/week. Katy and Houston Ship Channel both shed more than $2 after seeing price spikes amid the prior week’s wintry conditions.

South Texas prices also saw big week/week declines. Tres Palacios gave up 50 cents to average $3.41, while Tennessee Zone 0 South dropped 39 cents to $3.29.

Natural gas futures enjoyed a bullish week that saw lean storage inventories and a potentially frigid February support some of the highest prompt month prices since late 2016.

The February futures contract settled 5.8 cents higher at $3.505 Friday, up more than 30 cents from the previous Friday’s settlement of $3.185. The March contract climbed 7.6 cents to settle at $3.175 Friday.

With the soon-to-expire February contract trading up above $3.50, “the conversation now shifts to March,” according to Societe Generale analyst Breanne Dougherty. “We hold our $3.05 view for the March contract, but there is upside risk on the immediate horizon as there could be more convergence between February and March as the former expires, and then the March contract stands to benefit from another cold snap expected in early February.”

Societe Generale’s view for the rest of 2018 holds at $3.03, “still a slight premium to the current Nymex average of $2.94,” she added, noting that the firm would look to go long during any dips in the “core summer contracts” because of upside from cooling demand.

Breaks above $3.00 in the spring contracts provide an opportunity to enter short positions as “spring demand softness and ongoing production growth makes the season vulnerable to price weakness,” Dougherty said. “There is a mix of fundamental bearish and bullish indicators at play right now, and market reaction to them has been erratic of late. Strong 2018 price conviction is hard to establish.”

The Energy Information Administration (EIA) reported a mammoth storage withdrawal Thursday that surprised to the bullish side of expectations, but prompt-month futures lost ground after rallying earlier in the week.

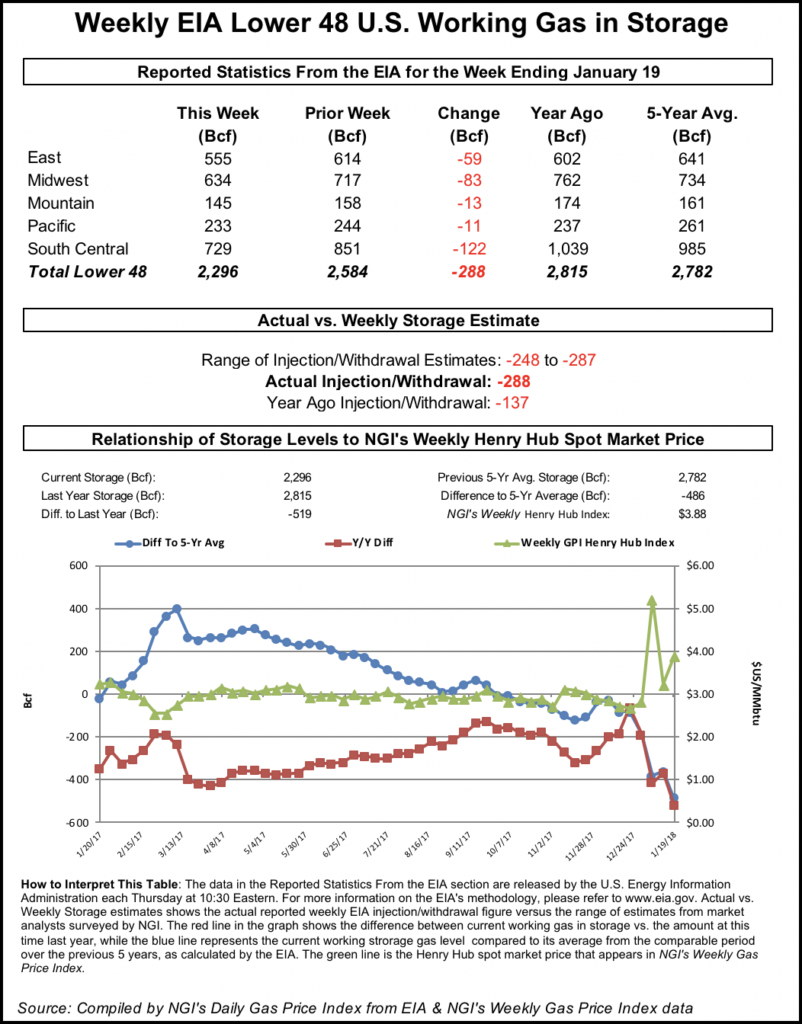

EIA reported a 288 Bcf withdrawal for the week ending Jan. 19, a bigger pull than what the market had been expecting. Last year, 137 Bcf was withdrawn, and the five-year average is a withdrawal of 164 Bcf.

This week’s reported withdrawal is tied for the second largest on record going back to at least 2010, matching the 288 Bcf withdrawal reported Jan. 10, 2014. That -288 Bcf number had stood as the largest on record until earlier this month, when EIA reported a whopping 359 Bcf pull for the week ending Jan. 5.

When EIA published the final figure at 10:30 a.m. EDT, the February contract briefly climbed above $3.50 after selling off to around $3.420 a few minutes before. By 11 a.m. EDT, February was trading around $3.460, down about a nickel from Wednesday’s settle. Shortly after 11 a.m. EDT, the March contract was trading about 5 cents higher at around $3.130.

Prior to the release of the final number, a Reuters survey of traders and analysts had showed estimates for a 272 Bcf withdrawal on average for the week ending Jan. 19. Intercontinental Exchange futures had been trading at -280 Bcf for the period as of Wednesday.

Stephen Smith Energy Associates had called for a 268 Bcf pull for the week. PointLogic Energy had estimated a withdrawal of 272 Bcf, while Kyle Cooper of ION Energy had been looking for a pull of 271 Bcf.

Bespoke Weather Services said it views the 288 Bcf withdrawal as “extraordinarily tight overall,” noting that it exceeded its estimate by 29 Bcf.

“We caution that next week’s print should be far looser, with production loosening and weather turning warmer exactly when” the current report period “ended, which is tempering the impact of the print a bit,” Bespoke said. “Still, this seems to confirm the upside we see for the March natural gas contract on any colder weather in the middle of February, and keeps our bullish sentiment intact for the contract.

“We continue to expect far more support for the March over February contract, as is occurring.”

Total working gas in underground storage stood at 2,296 Bcf as of Jan. 19, according to EIA. That’s versus 2,815 Bcf a year ago and five-year average inventories of 2,782 Bcf.

The year-on-year deficit increased week/week from -368 Bcf to -519 Bcf, while the year-on-five-year deficit widened from -362 Bcf to -486 Bcf, EIA data show.

By region, the largest withdrawal came in the South Central, which finished at -122 Bcf for the period, including 55 Bcf withdrawn from salt and 68 Bcf pulled from nonsalt. The Midwest saw a weekly withdrawal of 83 Bcf, while 59 Bcf was withdrawn in the East. The Mountain and Pacific regions saw withdrawals of 13 Bcf and 11 Bcf, respectively.

In the spot market Friday, warmer temperatures in the near-term sank East Coast prices, while Midwest points gained on forecasts for colder conditions by Monday. The NGI National Spot Gas Average fell 21 cents to $3.28/MMBtu.

Bespoke Weather Services said Friday it saw “a large number of risks for the natural gas market” heading into the weekend. “The market loosened significantly this past week, with elevated cash and prompt prices pulling back burns as a large amount of production came back online following freeze-offs. This should result in a smaller storage withdrawal to be announced” in the upcoming week “than previously expected, and has opened up downside in the market once the weather eases.”

However, guidance Friday continued to show heating demand increasing during the first few days of February, with further cold risks looking toward the middle of the month, according to Bespoke.

“We see further upside for the March contract over the next week or two, as we would expect the core of February cold to be focused from Feb. 10-20,” the firm said. “This does mean that we could lose some medium-term gas-weighted degree days in the first third of February, which was seen on European guidance Friday afternoon.”

According to Genscape Inc., “The market appears comfortable with the notion that production growth is going to be more than capable of satisfying demand for the balance of the winter and injection needs headed into the summer. Our SpringRock daily pipe data shows current Lower 48 volumes mostly recovered from the early January freeze-offs, now solidly back above the 76 Bcf/d mark.

“And SpringRock’s forecast continues to show monthly growth approaching 0.5 Bcf/d through the end of summer.” While the firm’s forecasts also show “impressive gains in demand…those gains are not expected to pace the supply-side growth.”

Genscape also noted that while the reported withdrawal for the week of Jan. 19 exceeded expectations, the previous week’s reported withdrawal came in lower than estimates.

“It often happens that a large discrepancy between expectations and the EIA’s report tends to get ”made up’ the next week with a reported number that’s off from expectations in the other direction,” Genscape said. “This pattern hints at a measurement error (where numbers reported to the EIA by the operators do not match the physical reality) that gets corrected the next week as operators…true-up the report.”

In a note to clients Friday, analysts with Tudor, Pickering, Holt & Co. (TPH) said they expect a “step-change” in the supply and demand dynamics for the upcoming week’s report. The analysts noted that “heating degree day forecasts for the week are around 20% below five-year norms, weather-related outages at Sabine Pass have pushed liquefied natural gas (LNG) exports for the week down to 2017 levels, and U.S. production has returned to peak levels of 77 Bcf/d.

“Though storage levels are precariously low, we still see supply outpacing demand to remove support for the commodity later into the year,” TPH said.

The Desk’s Early View natural gas storage survey showed respondents projecting a 99.8 Bcf withdrawal on average for the upcoming EIA report. Responses ranged from -95 Bcf to -114 Bcf.

NatGasWeather.com said a Friday afternoon run of the European weather model “remained quite cold with the system tracking out of the Midwest and into the East Tuesday and Wednesday…The data also maintained a strong Arctic blast across the Plains” beginning Thursday, “spreading into the East Feb. 3-4, but could be interpreted as just very slightly less extreme” though with some potential noise in the data, the firm said.

In the spot market, moderate temperatures in the near-term forecast kept a lid on prices in most regions.

PointLogic Energy’s one- to five-day forecast Friday showed the period starting “with a forecast mean population-weighted nationwide temperature of about 44 degrees, which is 4.5 degrees warmer than normal,” analyst Alan Lammey said. “Weather-related gas demand will soften as temperatures moderate across the East, capping a fairly bearish week.

“Daytime highs along the highly populated Interstate 95 corridor across the Mid-Atlantic will rise nearly 10 degrees day/day, with Washington, DC, bumping up into the low 50s and Philadelphia in the upper 40s,” both about 5-10 degrees above normal, according to Lammey.

“New York City and portions of New England, namely Boston, will remain chilly for another day with highs in the upper and lower 30s. Throughout the interior Northeast into the Ohio Valley, temperatures will be even warmer, with Pittsburgh and Columbus, OH, both reaching the lower 50s, while Buffalo will be in the lower 40s,” all about 15-20 degrees above normal.

East Coast cash prices weakened, especially at Algonquin Citygate, which dropped more than $5 Friday. Transco Zone 6 New York finished down 16 cents at $3.50, while Transco Zone 5 shed 16 cents to $3.49.

Meanwhile, a number of points in the Midwest and Midcontinent strengthened Friday.

AccuWeather was calling for temperatures in Chicago to drop from the 40s and 50s Friday down into the teens and 20s by Monday. Genscape projected demand in the Midwest region to increase to 15.64 Bcf/d Monday from 13.46 Bcf/d Friday.

Joliet added 8 cents to $3.23, while Northern Natural Ventura climbed 13 cents to $3.17.

After some healthy gains earlier in the week, Gulf Coast prices were mixed Friday. Henry Hub retreated 5 cents to $3.52, while Columbia Gulf Mainline eased 3 cents to $3.31.

Creole Trail Pipeline concluded maintenance on its Gillis Compressor station Thursday, two days earlier than expected, according to Genscape, restoring delivery capacity to Cheniere Energy Inc.’s Sabine Pass LNG terminal.

“This was after pipeline capacity was revised to 1.2 Bcf/d Jan. 24 after originally being set to 1 Bcf/d for the duration of the maintenance,” Genscape said. “Creole Trail reported deliveries of 1.17 Bcf/d to Sabine for Jan. 24-25, and timely cycles for Jan. 26” showed the same Friday.

“Aggregate deliveries to Sabine are at 2.98 Bcf/d as of Jan. 26 timely cycles, which is the highest level since problems at the liquefaction facility restricted feed gas deliveries beginning Jan. 18,” the firm said. “A combination of pipeline maintenance, possible economic shut-in during” winter weather and “downstream issues at Sabine have caused inconsistent feed gas deliveries during the month of January.”

In the West, the Rockies and California regional averages both fell by around a dime. SoCal Citygate posted the largest decline, giving up 39 cents to finish at $3.01.

Utility Southern California Gas Co. projected system demand to fall from just under 3.2 million Dth/d Friday to 2.644 million Dth/d by Monday.

© 2024 Natural Gas Intelligence. All rights reserved.

ISSN © 2577-9877 | ISSN © 1532-1258 |