NGI Weekly Gas Price Index | Markets | NGI All News Access | NGI Data

Modest Weekly Natural Gas Gains Continue, But Futures Leap Higher

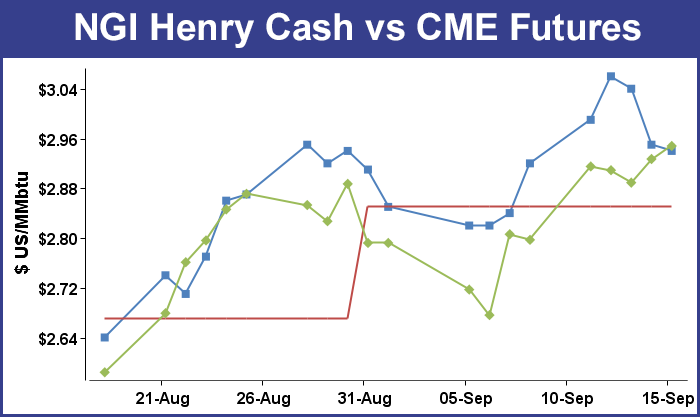

Weekly natural gas prices for the week ended Sept. 17 resembled something of a “tortoise and the hare” comparison, with the hare-like futures putting up double-digit gains and the physical market just plodding along.

The NGI Weekly Spot Gas Average added a slow but steady 2 cents on top of last week’s 6-cent gain to $2.63. October futures, on the other hand, ended the week at $2.948, up a solid 15.1 cents. Of individual market points, the week’s greatest advance was posted at NOVA/AECO C with a gain of $C30 cents to $C2.57/Gj and the week’s biggest loser was gas destined for southeasternmost Pennsylvania and southern New Jersey on Transco non NY North with a loss of $1.04 to $1.31.

Regionally, only two areas fell into the loss column, the Northeast with a 58-cent loss to $2.15 and Appalachia gave up 11 cents to $1.35.

Two regions posted single-digit gains, and all others were up by double-digits. The Midcontinent and Midwest rose 7 and 8 cents to $2.75 and $2.89, respectively.

The Southeast and California both advanced 11 cents, to $2.98 and $2.93 respectively, and the Rocky Mountains added 12 cents to $2.68.

South Texas weekly quotes were 13 cents higher at $2.91 and both East Texas and South Louisiana added rose by 14 cents to $2.91 and $2.93, respectively.

October futures ended the week within striking distance of $3 with a settlement of $2.948.

In Thursday’s activity futures trading was looking a little grim after the release of Energy Information Administration (EIA) figures showing a build of 62 Bcf, almost exactly what the market was expecting, but by the close October had managed a gain of 3.8 cents to $2.927 and November followed suit with a rise of 3.3 cents to $3.002.

Going into the day’s EIA storage report traders calculated that storage builds would have to equal the five-year average if storage were to match last year’s record-setting 3,954 Bcf. With seven weeks to go on the traditional injection season, 65 Bcf will be necessary to bring current stocks of 3,499 up to that level. This week’s estimates of the storage build were a step in that direction.

Last year, 74 Bcf was injected, and the five-year pace is a 68-Bcf addition, and when the 62-Bcf hit trading desks, the initial reaction was negative. No bullish news in a number that everyone expects. October futures reached a low of $2.834 immediately after the figures were released but by 10:45 a.m. October was trading at $2.884 down five-tenths of a cent from Wednesday’s settlement.

‘We were hearing a 62 to 63 Bcf figure and it was not much of an event,” said a New York floor trader. “The market was down, but then it jumped back. You see that almost all the time.”

“The 62-Bcf refill for last week was a match with the consensus expectations and so neutral on that account,” said Tim Evans of Citi Futures Perspective. “However, we note that that was also a step up from the 36-Bcf net injection and was also within 7 Bcf of the five-year average report. By that measure, this was the smallest, least supportive variance to the five-year average since April.”

Inventories now stand at 3,499 Bcf and are 184 Bcf greater than last year and 299 Bcf more than the five-year average. In the East Region 20 Bcf were injected and the Midwest Region saw inventories increase by 26 Bcf. Stocks in the Mountain Region rose 3 Bcf, and the Pacific Region was up by 4 Bcf. The South Central Region increased 9 Bcf.

In Friday’s trading physical natural gas for weekend and Monday continued to grind lower as forecasts of mild weather made three-day deals unattractive.

The NGI National Spot Gas Average fell 6 cents to $2.51, but several eastern points suffered stout double-digit losses and traded below $1. The few points that traded in positive territory did so by only a few pennies.

Futures trading was a different story, with the stalwart October contract continuing to gain ground. At the close October had risen 2.1 cents to $2.948 and November was higher by 1.9 cents to $3.021. October crude oil continued to sputter and fell 88 cents to $43.03/bbl.

Prices at eastern and Appalachia locations plunged as mild temperatures were forecast over the weekend. AccuWeather.com predicted that Boston’s high of 71 degrees Friday would climb to a pleasant 77 Saturday and ease slightly to 75 by Monday. The normal high in Boston at this time of year is 72. Philadelphia’s Friday high of 77 was expected to advance to 83 Saturday and slide to 80 by Monday, 2 degrees above normal.

Gas at the Algonquin Citygate fell 15 cents to $2.37, and packages on Iroquois Zone 2 shed 17 cents to $2.40. Deliveries to Tennessee Zone 6 200 L were quoted 28 cents lower at $2.13.

Several points in the Mid-Atlantic traded below $1. Gas on Tetco M-3 for weekend and Monday delivery fell a stout 26 cents to 93 cents, and gas bound for New York City on Transco Zone 6 lost 26 cents as well to 96 cents.

Marcellus points took it on the chin as well, with Tennessee Zone 4 Marcellus dropping 29 cents to 84 cents and gas on Dominion South shedding 24 cents to 93 cents. Deliveries to Transco Leidy retreated 31 cents to 87 cents.

Other market centers weren’t hit nearly as hard. Gas at the Chicago Citygate rose 4 cents to $2.88, and deliveries to the Henry Hub came in a penny lower at $2.94. Packages on El Paso Permian shed 5 cents to $2.64, and gas priced at the SoCal Citygate changed hands 9 cents lower at $2.78.

Futures traders see more gains ahead. “I think we still have a little more upside before we start seeing some of the downside,” said Alan Harry, director of trading at McNamara Options in New York.

One factor that has Harry’s attention is that “on Aug. 19, 17,000 October $3 calls were purchased and 7,000 of the October $3.25 calls were bought on Globex, and it doesn’t look like any of them have been sold out. That could exacerbate the move, and you should have a lot of shorts running to cover.

“Fundamental-wise, I think you have lower levels. I am looking for a move up to $2.97 to $3.02 and then a fall back down. There is some interest in this Sabine situation (return to production following maintenance) and when that is going to fill up. I think that happens Sunday or Monday.

“I’m looking for a catalyst to say the market will go down, and one of the catalysts would be the cash market. The cash market until recently was trading premium to the Henry Hub and I’m looking for that spread to tighten. That would be a catalyst for prices to fall. And the other catalyst would be if we can’t get rid of this excess gas.

“I’m looking for a brief move up and then we will have a big fall-off.”

Despite being solidly within the confines of the shoulder season, forecasters are continuing to expect above-normal temperatures. In its Friday morning outlook WSI Corp. said, “[Friday’s] six-10 day forecast is even warmer than yesterday’s forecast over the southern half of the nation, but cooler over the West Coast and the northern tier. As a result, CONUS PWCDDs are up another 1 to 38.3 for the period. This is 16.1 higher than average!”

Analysts don’t see the warm weather as having a market impact. “[H]opes for any support off of the weather factor are beginning to diminish. Extended hot temperature forecasts along the eastern portion of the U.S. are seeing some moderation beyond next week while most of the Midcontinent will be seeing normal patterns that will sharply reduce air conditioning requirements,” said Jim Ritterbusch of Ritterbusch and Associates in a Friday morning report to clients.

“And on the storm front, lack of any significant threat to GOM infrastructure is forcing some erasure of storm premium. Going forward, the likelihood of major hurricane events will begin to diminish amidst a shoulder period that will be sharply upsizing injections. [Thursday’s] EIA supply increase offered no surprises as storage lifted to 3.5 Tcf as expected. And although next week’s figure will likely show a larger contraction in the surplus against the averages, we still see possibilities of an additional 450-500 Bcf added to supply by early November when a peak is usually established.

“We are maintaining a bearish stance as we continue to target a further price decline in October futures to the $2.70 area. We are keeping stop protection above 2.99 for now but will likely adjust this stop lower to above today’s highs…”

Gas buyers for weekend power generation should have plenty of wind power at their disposal. “High pressure will depart today and allow a broad frontal system to slowly track into and across the power pool during the next three or so days with areas of rain and thunderstorms,” said WSI. “Despite the unsettled weather, there will actually be a general moderating trend with highs in the upper 60s, 70s and 80s.

“The frontal system will lead to a rise of wind generation [Friday] into early Saturday with output of 4-6+ GW. After a brief decline, a southwest-to-west wind associated with the northern stream frontal system will lead to a pulse of elevated wind gen during Sunday into Monday.”

Analysts saw Thursday’s 62 Bcf storage build as still representing a tightening market. “Compared to degree days and normal seasonality, a +62 BCF appears tight vs. the prior five years by approximately 2.4 Bcf/d,” said industry consultant Genscape in a Friday morning report. “This includes an estimated 10 Bcf impact from the labor day holiday, which is the average estimated impact of Labor Day over the prior five years. Gas burn declined by approximately 36 Bcf week/week due to cooler temps and Labor Day knocking down generation by 33.8 AGWH as well as a 10.6 AGWH increase in renewables. Gas generation was down a whopping 26 AGWH, which equates to approximately 5.2 Bcf/d.”

© 2024 Natural Gas Intelligence. All rights reserved.

ISSN © 2577-9877 | ISSN © 1532-1258 |