Markets | NGI All News Access | NGI Data

Weekly NatGas Inches Higher Ahead Of Long Weekend

For the shortened week of trading ended Thursday quotes were something of a mixed bag with little overall change, but significant differences arose between producing zones and market zones in the Northeast and California.

The NGI Weekly Spot Gas Average gained 2 cents to $2.71, and Westcoast Station No. 2 in Canada took the honors as the market point with the week’s greatest gain, $C0.31 to $C2.33/Gj. The week’s greatest loser turned out to be El Paso Permian with a drop of 66 cents to $2.77.

Three regions, the Rocky Mountains, the Northeast, and California were all in the red, but the remainder of the country regionally posted gains. The Rockies lost a penny to $2.54, the Northeast was down 9 cents to $2.53, and California shed 22 cents to $2.88.

Appalachia added 3 cents to $2.00, the Southeast rose a nickel to $2.94, and South Texas came in 6 cents higher at $2.92.

Both East Texas and the Midwest added 8 cents to $2.93 and $2.84, respectively, the Midcontinent gained 7 cents to $2.69, and South Louisiana tacked on 11 cents to $2.91.

July futures terminated Wednesday at $3.067, down 16.9 cents from the settlement of the June contract.

The August contract finished out the five-day week at $3.035, up 8.4 cents.

At the end of the abbreviated trading week Thursday physical natural gas for Friday delivery managed to outdo a futures market that seemed to have had its fill of bullish weather reports. Gains in the Northeast, Appalachia, and California were able to offset softer quotes in the Midwest, Midcontinent, and Louisiana, and the NGI National Spot Gas Average rose 4 cents to $2.77.

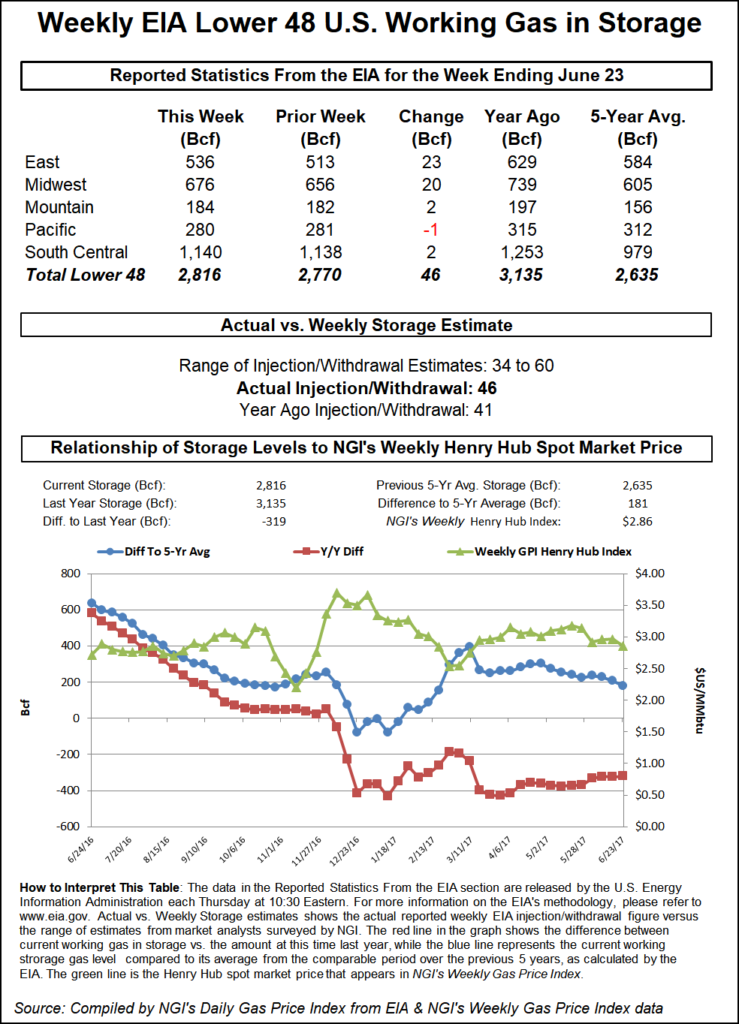

The Energy Information Administration (EIA) reported a storage build of a miserly 46 Bcf, about 6 Bcf less than expected, but the futures market nonetheless turned lower. At the close August had lost 5.2 cents to $3.042 and September was down 5.0 cents to $3.037. August crude oil added 19 cents to $44.93/bbl.

The newly-minted spot August future took what should have been construed as a supportive Energy Information Administration (EIA) natural gas storage report and turned it into a negative despite figures that were well below market expectations.

The EIA reported a storage injection of 46 Bcf, about 6 Bcf less than consensus estimates. Following the release of the figures, August futures rose to $3.122, and at 10:45 a.m. August was trading at $3.097, up three-tenths from Wednesday’s settlement.

Prior to the report traders were looking for a somewhat larger storage build. Last year 41 Bcf was injected and the five-year average stood at 72 Bcf.

Citi Futures Perspective calculated a 54 Bcf injection and IAF Advisors estimated a 51 Bcf increase. A Reuters survey of 22 traders and analysts showed an average of 52 Bcf with a range of +40 Bcf to +60 Bcf.

“The market came up a bit, but fell off its highs,” said a New York floor trader. “The market really didn’t do much of anything, but it’s holding above $3, which is a positive, and that’s probably where it is going to hold for now.”

Longer term, traders are optimistic.

The Denver analytical team at Wells Fargo said the storage data “provides further confirmation that the natural gas markets are at least 2 Bcf/d undersupplied. Over the last 9 weeks, this state of undersupply has caused the surplus to fall by 120 Bcf from 307 Bcf at the end of April.

“Based on current weather forecasts, our model indicates a 102 Bcf cumulative injection over the next 2 weeks, which would bring the storage surplus (versus the five-year average) down to just 147 Bcf. As a reminder, our forecast for end-of-injection season storage is 3.88 Tcf, which is in-line with the five-year average and incorporates 3 Bcf/d of lost power generation demand due to gas-to-coal switching driven by higher summer natural gas prices.”

“The 46 Bcf build for last week was smaller than both the 52 Bcf consensus estimate and the 72-Bcf five-year average, a clear bullish surprise,” said Tim Evans of Citi Futures Perspective. “In our view, this keeps the market on track for further gains, with failed technical support at $3.25, and the $3.50 level last tested in mid-May as possible targets in the weeks ahead.”

Inventories now stand at 2,816 Bcf and are 319 Bcf less than last year and 181 Bcf greater than the five-year average.

In the East Region, 23 Bcf was injected, and the Midwest Region saw inventories rise by 20 Bcf. Stocks in the Mountain Region were 2 Bcf higher, and the Pacific Region was down 1 Bcf. The South Central Region increased 2 Bcf.

The physical market saw healthy weather-driven advances as eastern highs going into the weekend were expected as much as 10 degrees above normal. AccuWeather.com forecast that Boston’s Thursday high of 79 degrees would jump to 90 by Friday before ebbing slightly to 88 on Saturday, well beyond the normal high of 80. New York City’s high Thursday of 82 was also expected to jump to 90 on Friday but ease to 86 by Saturday. The normal high this time of year in the Big Apple is 83. Philadelphia’s Thursday high of 88 was forecast to reach 92 on Friday and hold at 90 on Saturday, 4 degrees above normal.

Gas at the Algonquin Citygate jumped 51 cents to $3.22 and gas on Iroquois Waddington gained 9 cents to $3.03. Deliveries to Tennessee Zone 6 200 L added a stout 45 cents to $3.10.

Packages priced at Tetco M-3 Delivery added 11 cents to $2.16 and gas bound for New York City on Transco Zone 6 rose 23 cents to $2.79.

The National Weather Service in New York City reported that a warm front remains well to the north as high pressure sits over the western Atlantic through Friday. “A cold front will slowly approach during the day on Saturday, eventually moving offshore late in the day on Sunday. The front remains nearby on Monday before weak high pressure builds in from the northwest for the middle of next week.”

Other market points were mostly lower. At the Chicago Citygate deliveries Friday shed a penny to $2.83 and gas at the Henry Hub also eased a penny to $3.00. Gas on El Paso Permiandropped a penny to $2.63, and gas on Northern Natural Demarcation came in 2 cents lower at $2.74.

Gas on Kern Receipt lost 3 cents to $2.60 and gas priced for Friday delivery at the PG&E Citygate was quoted a penny lower at $3.18

Physical natural gas for delivery over the extended holiday weekend took a nose dive in Friday trading as traders saw no reason to commit to what amounted to a five-day deal. Double-digit setbacks were widespread and only a single point followed by NGI made it to the positive side of the trading ledger. The NGI National Spot Gas Average plunged 13 cents to $2.64.

Futures traders see a weak market but admit that forecast warm weather is likely to prop prices up and limit moves to the downside. At the close August had slipped seven-tenths to $3.035 and September was off six-tenths to $3.031.

Energy demand at eastern locations was seen steady to lower over the extended holiday weekend. The New York ISO forecast peak load Friday of 25,715 MW would fall to 23,908 MW by Monday and rise modestly to 24,192 MW by Wednesday. The PJM Interconnection said Friday peak load of 49,613 MW would rise to 49,852 MW Monday and slide to 49,311 MW Wednesday.

Gas at the Algonquin Citygate fell 57 cents to $2.65 and deliveries to Iroquois Waddington dropped 12 cents to $2.91. Gas on Tennessee Zone 6 200 L skidded 50 cents to $2.60.

Major market centers were down by double-digits. Gas at the Chicago Citygate was quoted 16 cents lower at $2.67 and deliveries to the Henry Hub came in 6 cents lower at $2.94. Gas on El Paso Permian changed hands 19 cents lower at $2.44 and deliveries to the NGPL Midcontinent were seen 15 cents lower at $2.56.

Gas at Opal fell 16 cents to $2.44 and packages priced at the SoCal Border Average dropped 18 cents to $2.54.

[Subscriber Notice Regarding NGI‘s Market-Leading Natural Gas Price Indexes]

August futures opened a penny lower Friday morning at $3.03 as weather forecasts moderated and traders reacted cautiously to inventory data that was expected to drive the market higher.

“Natural gas is looking a little soft,” said a New York floor trader. He hedged his bets somewhat and added, “I think we will get a lot more heat now, and you notice they put a little bit less in this week so the bullish [storage] numbers could stay.

“I do not think it will stay above $3, but I do like it at $2.90 to $2.92. I think it’s a little sale here, but if you get a rally over $3.05 to $3.06, you have some room to the upside.”

Higher prices would be music to the ears of producers expected to increase drilling in the Marcellus/Utica and Permian basins. U.S. oil and gas rig activity remained pretty steady during the last week of June as those in search of oil declined by two to 756, while those drilling for natural gas added one to 184, according to data from Baker Hughes Inc.

Combined, the 940 U.S. oil and gas rigs in service marks a 118% increase over the 431 rigs that were in operation one year ago.

Economics are still favoring plays with strong oil returns, especially the Permian Basin and its various sub-basins. For the week ending June 30, the Permian Basin only added one rig to reach 370 in the play. While the increase was small, the 370 rigs in operation represent a 140% increase over last year’s level of 154 rigs.

Ritterbusch and Associates senses that the market is sending off some bearish vibes given its inability to advance off of last week’s seemingly bullish Energy Information Administration storage report that offered a smaller than expected 46 Bcf injection. In a morning report to clients it said while contraction in the surplus is likely to slow appreciably next week, the short term temperature views continue to favor additional contraction in the supply excess against 5 year averages of around 40 Bcf next month.

“This dynamic should prove sufficient to keep values supported above last week’s lows of about $2.87 per nearby futures. However, our expected advance up into the 3.22-3.25 zone is being pushed back a couple of weeks as some moderation is beginning to show up in some of the weather views toward mid-month. All factors considered, we are still sidelined in this market in anticipation of some wide price swings in both directions with prices apt to post negligible change a couple of weeks down the road.

“For now, we will await price pullbacks into the $2.87-$2.92 zone to approach the long side for an investment type trade given what is shaping up to be a much smaller storage cushion with 2-3 months remaining in the” cooling degree day (CDD) “season. We are, however, keeping a hold on long Sept ’17-short March ’18 bull spreads.”

Gas buyers for electrical generation throughout the vast PJM footprint over what could be an extended holiday weekend will not have much in the way of renewable power to work with should incremental purchases be necessary. WSI Corp. in a morning report to clients said a few storms may be locally strong. Despite the chances for storms, a southwest flow and partial, hazy sunshine will support seasonably warm/hot and humid conditions. Max temperatures will generally top out in the 80s to low 90s. Humidity levels will be elevated with dewpoints in the mid 60s to near 70. This will help hold min temps in the mid 60s to mid 70s.

“A southwest to northwest breeze will support modest wind gen during the next two days. Output will range 1-3 GW. Wind gen will subside and become relatively light and variable during Sunday into early next week.”

In a longer time frame WSI said conditions had moderated just a touch. “The 6-10 day forecast is initially warmer. However, cooler changes were made to portions of the Plains and East during the back half of the period. The West is now even warmer.” Continental U.S. population-weighted CDDs “are down 0.9 to 62.5, which are 10.7 above average.

“Models are hinting at a more amplified flow, which supports some warmer risks over the western and central US. The Midwest and Northeast could run a touch cooler.”

© 2024 Natural Gas Intelligence. All rights reserved.

ISSN © 2577-9877 | ISSN © 1532-1258 |