NGI Archives | NGI All News Access

Western Canada’s Unconventionals Seen Doubling Oil Output by 2025

Western Canada’s oil production should hit 5.7 million b/d by 2025, which is double the current output, boosted by unconventional growth from the oilsands and shale formations, according to ITG Investment Research (IR). Unconventional natural gas production also is seen lifting gas supplies by 3 Bcf/d from current numbers.

More than 300,000 wells that posted oil and natural gas production in 2007-2012 were analyzed by the IR analysts, led by ITG vice presidents of energy Brook Papau and Samir Kayande. The analysis, compiled in “No More Guessing: Canada,” enabled the analysts to create a rig- or project-based development model to forecast natural gas, oil and natural gas liquids (NGL) production to 2025.

“A break-even cost curve analysis (B/E) was then layered on to forecast the average supply cost of new production,” said Papau and Kayande. “Finally, we examined current takeaway capacity out of Western Canada and North Dakota to estimate further rail capacity required to alleviate transportation bottlenecks.”

The analysts reviewed 12 different plays across the Western Canadian Sedimentary Basin, as well as the Williston Basin extending in Canada, and examined historical oil, gas and NGL output and activity for each.

Bottom line: oil production is growing by leaps and bounds, and gas has a good chance of contributing if the unconventional plays now being developed materialize as they’ve been forecast. But it’s infrastructure that may hold everything back.

“Pipeline capacity in the Western Canada, U.S. Rockies and U.S. Bakken production areas will not keep pace with supply growth over the next four years, requiring incremental rail shipment volumes 600,000 b/d, even if all planned pipeline projects, such as Keystone XL and Northern Gateway, proceed,” the ITG IR analysts found.

Since 2005, bitumen, cold flow heavy and synthetic crude oil has accounted for more than half (53%) of Canada’s production additions, said the analysts. Last year alone, Alberta’s oily Cardium formation accounted for 12% of production additions, while the Bakken Shale in Saskatchewan accounted for 7%. The base decline in Western Canadian oil production is expected to fall to about 7% by 2025, down from 12% in 2012, driven by bitumen growth, said the IR analysts.

Among other things, the analysis determined that:

Natural gas output, particularly from emerging unconventional formations, also should strengthen.

“At assumed rig counts in the Montney, Horn River Basin and Duvernay plays, Western Canadian raw natural gas production rises to 19 Bcf/d, equivalent to 16 Bcf/d of marketable production, by 2025, up 3 Bcf/d compared to today,” said the researchers.

“Our forecast is predicated on a ramp-up in activity in the Montney and Horn River Basin in response to liquefied natural gas facility feedstock requirements. In addition, we assume success in the Duvernay, and model 42 rigs running there by 2016.”

Including natural gas from both gas and oil wells, there’s been a base decline of 20% over the past year for Western Canadian gas production, according to the data. Gas shut-ins from early 2012 caused a jump in base decline rates by about 3% from 2011, when the decline rate was 17%.

“Monthly gas production additions during the past six years averaged 300 MMcf/d, and Western Canadian production fell from 20 Bcf/d to 16 Bcf/d (raw). Total rigs counts in the period dropped by half, but the proportion of horizontal rigs rose from 10% in 2007 to 90% in 2012.”

Meanwhile, the region’s liquids-rich plays, which include associated gas and Alberta’s Deep Basin, accounted for more than half (56%) of gas additions in 2012, the research showed.

More than one-third (36%) of the gas reserves last year were from the top 10 gas producers in Western Canada, which implies “a more diverse set of operators than oily producers,” said ITG’s researchers.

In addition, the Deep Basin and Montney Shale “have shown increasing production adds/drill day. A rig running in either play brought on 90 Mcfe/d/drill day in 2012.”

If the gas rig count were to remain at 2012 levels, it would reduce the researchers’ gas forecast by 3.2 Bcf/d by 2025, “equating to a slight decline in Western Canadian gas production.”

Of the incremental production, gas from liquids-rich plays, such as the Deep Basin, Duvernay and associated gas, is forecast to account for more than half (55%) of new production by 2020. Analysts are projecting a half-cycle, weighted-average supply cost for natural gas of $3.74/Mcf New York Mercantile Exchange by 2015.

Assuming success in the liquids-rich Duvernay, NGL output is set to grow to 420,000 bl/d by 2025, up from 300,000 b/d last year.

“To date, the Duvernay looks encouraging but due to the early stage of development it is not without risk,” said the IR analysts. “Without the Duvernay, our gas and NGL supply model forecasts very modest growth.

“Marketable gas volumes would drop by 2 Bcf/d in 2025 to 14 Bcf/d, and our NGL forecast would drop by 92,000 b/d to 328,000 b/d. In addition, ITG IR’s 2015 estimate of the half-cycle gas supply cost would increase to $4/Mcf.”

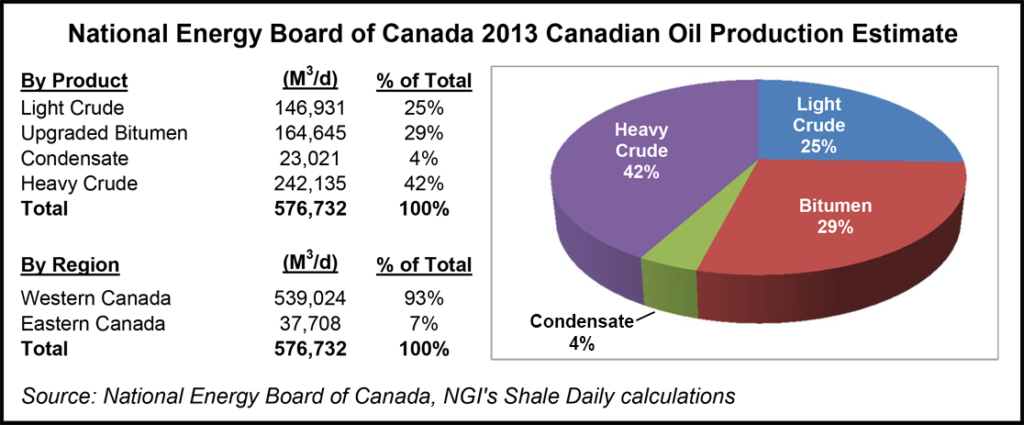

Looking at a more near-term oil forecast, the National Energy Board (NEB) expects Canadian oil production for the year to consist of 42% heavy crude, 29% upgraded bitumen, 25% light crude and 4% condensate. Also, Western Canada will account for 93% of the country’s oil production in 2013, according to NEB data and NGI’s Shale Daily calculations.

© 2024 Natural Gas Intelligence. All rights reserved.

ISSN © 2577-9877 | ISSN © 2158-8023 |