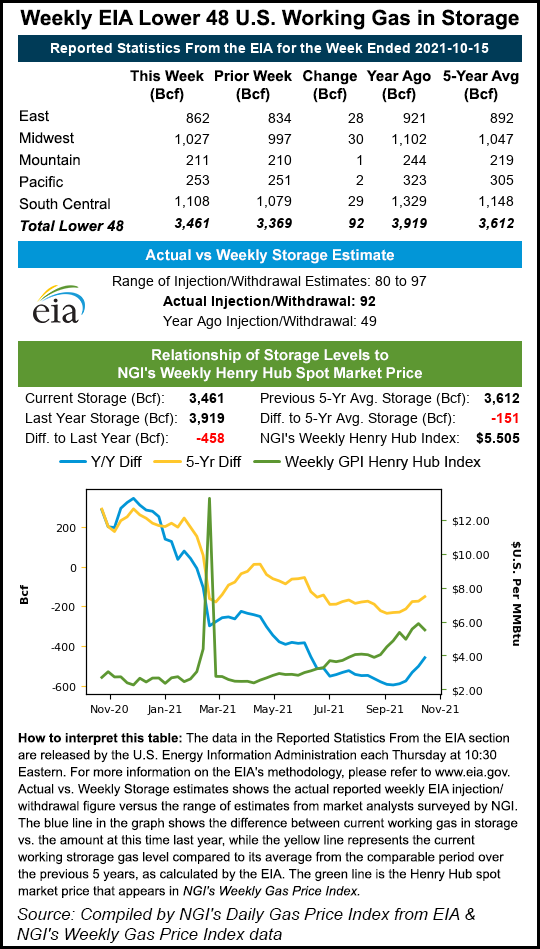

Markets | Natural Gas Prices | NGI All News Access

Weekly Natural Gas Prices Extend Downward Slide Amid Benign Weather Conditions

Share on:

© 2024 Natural Gas Intelligence. All rights reserved.

ISSN © 2577-9877 | ISSN © 1532-1258 |

Markets | Natural Gas Prices | NGI All News Access

© 2024 Natural Gas Intelligence. All rights reserved.

ISSN © 2577-9877 | ISSN © 1532-1258 |

Earnings

Producers of natural gas may be struggling with low prices, but for pipeline operators like Kinder Morgan Inc. (KMI), the outlook is anything but bearish. The Houston-based midstreamer, which transports about 40% of the natural gas consumed in the United States, kicked off the first quarter earnings season with stellar results and a positive message…

April 18, 2024Infrastructure

Natural Gas Prices

By submitting my information, I agree to the Privacy Policy, Terms of Service and to receive offers and promotions from NGI.