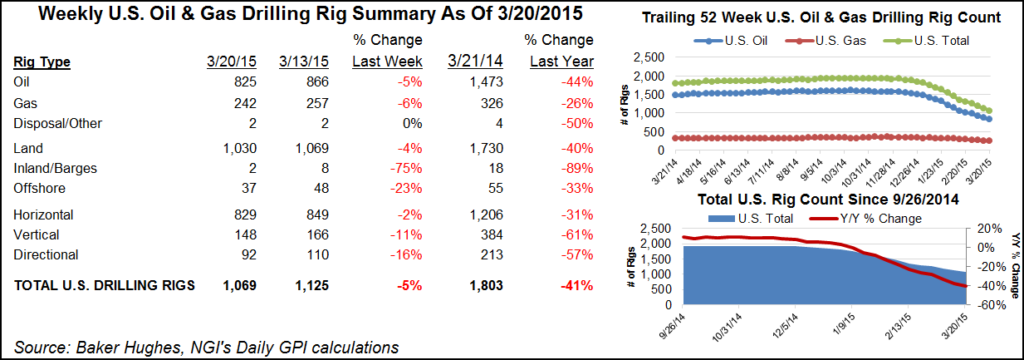

Infrastructure | E&P | NGI All News Access

U.S. Producers Raise Two NatGas, Three Oil Rigs Ahead of Holiday

U.S. natural gas operators hoisted two rigs ahead of the Thanksgiving holiday, while oil operators raised three for the week, Baker Hughes Inc. said Wednesday.

Overall, the North American total rig count was down by five week/week to 767 from 772, and it declined from 928 in the year-ago period. The five-year average is 2,020.

The U.S. rig count ahead of the holiday was down 151 from the same period a year ago to 593. The number of U.S. rigs drilling for gas stood at 118, 71 fewer (38%) than a year ago. There also were 474 oil rigs in operation, down 81, or 15%, year/year. The U.S. offshore rig was static week/week at 23, but it was off seven from a year ago.

Horizontals were the rig of choice in the United States, with 475, versus 470 a week earlier. There also were 52 directional and 66 vertical rigs running in the United States for the week.

Canada, which lost 10 rigs week/week and saw its rig count fall by 10 overall from a year ago, had 174 in total running as of Wednesday. There were 94 oil rigs running as of Wednesday, versus 100 a year ago. Seventy-eight gas rigs were active, down from 84. The five-year rig count average is 372.

In a note earlier this month about how many U.S. drilling permits had been issued through October, Evercore ISI senior analyst James West said permitting had fallen off from a September high, but it was still well above the 2016 average.

“U.S. land permits totaled 2,501 in October, down 12% from 2,845 in September. October exhibited the third highest monthly permit total this year, but was 44% below year-ago levels, as the U.S did not experience the same seasonal uptick observed in previous years…” October usually benefits from operators accelerating permit filing to work through drilling budgets in the fourth quarter.

Year-to-date through October, land permitting was down 42% from the same period of 2015 and 48% from 2009, when drilling was in a slide from the 2008 peak.

“Relatively strong permit numbers in Ohio (plus-59%), Virginia (plus-100%), and Colorado (plus-3%) bolstered October U.S. land totals, offset by modest declines in Louisiana and Oklahoma (each down 25%),” West said. “Texas permitting has remained resilient relative to the land total, down just 2% sequentially.”

Texas, led by the Permian Basin and complemented by the Eagle Ford Shale, Gulf Coast and Haynesville Shale development, “continues to be the single-most important state in terms of evaluating the magnitude and direction of U.S. permitting trends, although permitting also exhibited strong growth in the Rockies, Gulf Coast and Northeast,” West said. “Drilling interest also is spreading well beyond the core acreage.”

According to Evercore, Texas District 8A, which includes the Permian’s Delaware sub-basin, has seen its July-October permit totals jump 58% from the same period of 2015. Nearly every Texas oil basin was within 20% of year-ago July-October permit levels as liquid-rich activity increases.

Meanwhile, Wyoming permitting in the Niobrara formation between July and October rose an unprecedented 34% above the 10-year state average as producers use enhanced drilling to unlock the basin, which is third in line in permitting behind the Permian and Oklahoma’s myriad stacked reservoirs.

In addition, Gulf of Mexico permitting increased in October for the third straight month and climbed 60% sequentially from September.

In more positive news for development, the first week of November set a year-to-date weekly high of 763 permits, according to Evercore. “November is on pace to eclipse the 2016 monthly high set in September.”

© 2024 Natural Gas Intelligence. All rights reserved.

ISSN © 1532-1231 | ISSN © 2577-9877 |