NGI All News Access | E&P | Infrastructure

U.S. Natural Gas Rig Count Drops Again as E&Ps Facing Headwinds

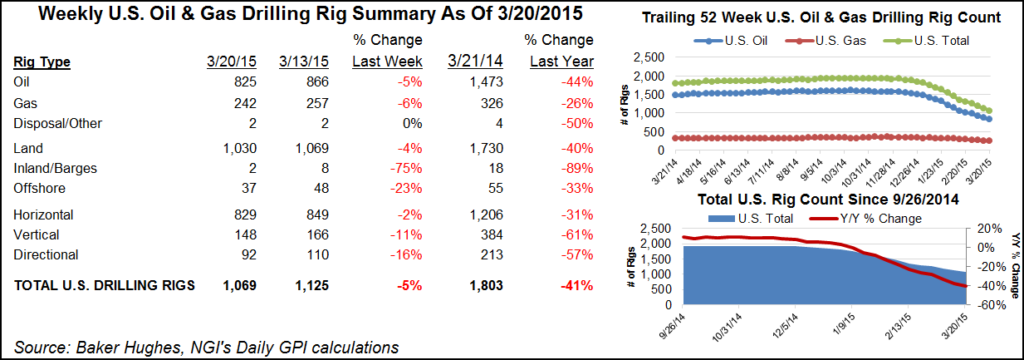

The U.S. natural gas rig count fell four units to 119 for the week ended Friday (Jan. 10), while a double-digit decline in oil activity compounded yet another down week for domestic drilling activity, according to the latest numbers from Baker Hughes Co. (BKR).

The combined U.S. count tumbled 15 units — 11 oil-directed — for the week to end at 781. That’s down nearly 300 units from the 1,075 U.S. rigs active in the year-ago period.

Most of the declines occurred on land, with one rig departing in the Gulf of Mexico. Six directional units and six vertical units packed up shop, joined by three horizontal rigs, according to BKR.

Canada’s rig count, meanwhile, bounced back during the week, jumping 118 units overall, including 93 oil rigs and 25 gas rigs. The Canadian count ended at 203, up from 184 in the year-ago period.

Among the major plays, the Permian Basin (down six) and the Haynesville Shale (down four) posted the sharpest losses on the week. The Permian ended the week with 397 active rigs overall, down from 488 a year ago. The gassy Haynesville finished at 45, versus 53 at this time last year.

Also among plays, the Ardmore Woodford, Cana Woodford and Marcellus Shale each added one rig, while the Denver Julesburg-Niobrara, Utica Shale and Williston Basin each dropped one.

Among states, the week/week changes mirrored the shift in the plays, with Texas (down seven) and Louisiana (down three) accounting for the largest drops. New Mexico saw two rigs pack up during the week.

Also among states, Oklahoma and Pennsylvania each added one rig, while Alaska, Colorado, North Dakota, Ohio and Wyoming each dropped one.

The natural gas and oil sector is coming to grips with a bevy of uncertainties in 2020, as capital markets are drying up, investors are fleeing and the global community voices increasing concerns about fossil fuels.

Energy industry prognosticators see a foggy 2020, potentially a repeat of sorts from 2019, with a mild increase in capital expenditures for the E&P sector and continued pain for oilfield services (OFS).

The Evercore ISI analyst team led by James West recently compiled the 2020 Global E&P Spending Outlook, an annual sampling in which data was collected from more than 250 oil and gas operators of all stripes — publics, privates, domestic and internationally focused, from the smallest of the moms-and-pops to the supermajors.

The “tale of two markets” is arriving this year, West said. The pain in North America “is being felt all around,” with more than 32 bankruptcy filings by North American E&Ps last year amounting to around $13 billion in debt.

Investors also are exiting the sector. A dollar invested in the OSX Index 20 years ago would have fetched “an extra penny in your pocket, compared to nearly $5 for the S&P 500,” West said. “This clear disconnect has brought energy weightings in the S&P 500 to between 4-5% versus a stunning 15% this past decade.”

© 2024 Natural Gas Intelligence. All rights reserved.

ISSN © 1532-1231 | ISSN © 2577-9877 |