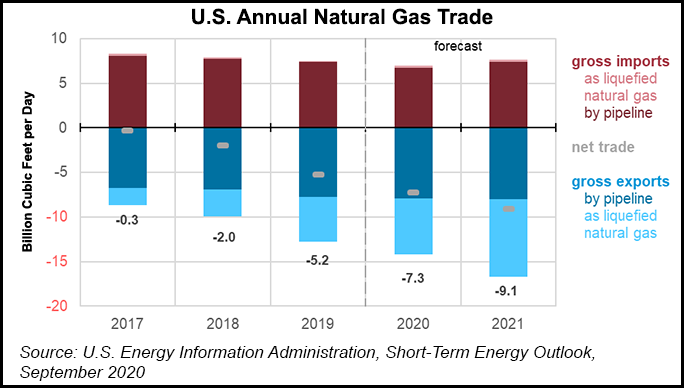

Demand for natural gas is likely to increase domestically and overseas heading into the winter, while production stagnates, pushing Henry Hub spot prices to an average of $3.40/MMBtu in January, the Energy Information Administration (EIA) said Wednesday.

In the latest Short-Term Energy Outlook (STEO), forecasters said monthly average spot prices should “remain higher than $3.00/MMBtu for all of 2021, averaging $3.19/MMBtu for the year, up from a forecast average of $2.16/MMBtu in 2020.”

Total U.S. working gas in storage at the end of August was 3.5 Tcf, 13% more than the five-year (2015-2019) average, EIA noted. EIA now expects inventories to reach almost 4.0 Tcf on Oct. 31, which would be 6% more than the five-year average.

The upbeat forecast noted that Henry Hub spot...