Shale Daily | E&P | NGI All News Access

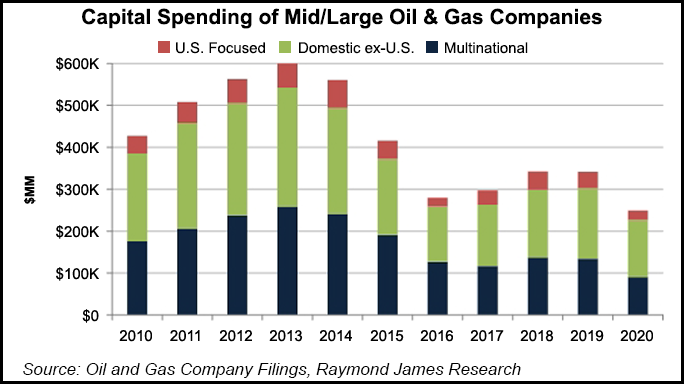

U.S. E&Ps Reining in Capex, while International Operators Spending More

Share on:

© 2024 Natural Gas Intelligence. All rights reserved.

ISSN © 2577-9877 | ISSN © 2158-8023 |

Shale Daily | E&P | NGI All News Access

© 2024 Natural Gas Intelligence. All rights reserved.

ISSN © 2577-9877 | ISSN © 2158-8023 |

Earnings

Liberty Energy Inc. CEO Chris Wright said Thursday he does not expect exploration and production customers to increase their onshore natural gas activity before the end of this year, but a lack of activity will not be a stumbling block to advance future opportunities. The oilfield services (OFS) company, considered one of the leading hydraulic…

April 19, 2024By submitting my information, I agree to the Privacy Policy, Terms of Service and to receive offers and promotions from NGI.