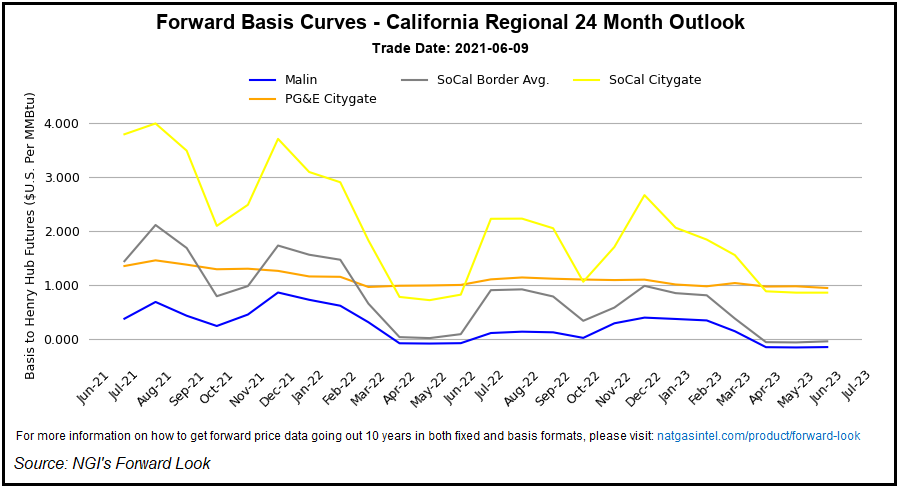

Big basis moves in Appalachia and on the West Coast highlighted natural gas forwards trading during the June 3-9 period, while a sufficiently hot forecast helped propel a broader move higher for the Lower 48 overall, according to NGI’s Forward Look.

Fixed prices for July delivery were higher week/week by around 10-15 cents at numerous locations, with benchmark Henry Hub gaining 8.8 cents to average $3.130/MMBtu.

Forecasts teasing June heat, along with the prospect of Appalachian supply disruptions, helped stoke the fire that saw July Nymex futures rise during the period. On Thursday, the front month continued to nudge higher, going on to settle at $3.149, up 2.0 cents day/day.

Appy Supply Pinch

The potential duration of a pressure reduction on the Texas Eastern...