NGI Archives | NGI All News Access

Statoil Sees ‘Sufficient Demand’ Worldwide for Shale-Driven Natural Gas

North America should find plenty of outlets for its copious natural gas reserves, but some questions need to be clarified soon, such as whether to allow manufacturers to dictate how much supply remains onshore, or whether the free market fuels an export revolution, according to Statoil ASA’s chief economist.

“Energy Perspectives,” compiled annually by Statoil, describes the long-term macroeconomics and market outlook for all types of energy resources. Chief economist Eirik Waerness led a research team to compile the 2013 report, and he shared the company’s perspective on Monday at Columbia University’s Center on Global Energy Policy. Statoil’s analysis, he said, probably falls somewhere in the middle of annual forecasts prepared over the past year by the U.S. Department of Energy, ExxonMobil Corp., BP plc and Royal Dutch Shell plc.

Like all of the other forecasters, Statoil sees a lot of natural gas production potential, particularly in North America. However, how much is kept in North America to help rebuild the manufacturing sector and lower some energy costs remains an uncertain question. In any case, “environmental policies are expected to improve the competitiveness of gas” in every region of the world.

“The supply potential of shale gas continues to surprise, both in terms of volumes and marginal costs,” Waerness said. Uncertainties exist in Statoil’s forecasts for North American gas supplies because of the evolving market questions. Should fewer coal-fired generators be allowed? Should gas be used to help fuel a manufacturing renaissance, build an emerging transportation corridor? Or should it be exported overseas as liquefied natural gas (LNG)?

Bottom line, he asked the audience, “Will there be sufficient demand for all that gas?…We believe there is, with some LNG exports having an impact on the markets. We see more gas in manufacturing and transportation, particularly LNG transportation. Part of the gas also will be used to produce oilsands…North America has an energy source that could be used domestically or for export.”

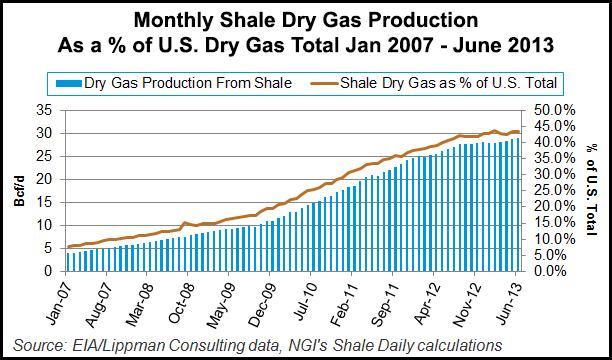

U.S. monthly shale dry gas production and its share of U.S. total dry gas production both increased steadily from early 2007 until about a year ago, and have been nearly flat since then, according to EIA/Lippman Consulting data. In June dry gas production from shale was 28.91 Bcf/d, or 43.6% of the U.S. dry gas total.

However, North America’s gas supplies are far from the only game in town, said the Statoil economist. As North American LNG export projects begin to ramp up over the next four or five years, several mega-facilities also are expected to roar into production in Latin America, Russia, the Asia Pacific region and Africa.

“And we ask, to what extent can gas markets integrate and become more like an oil market?” The key factor is how much LNG is available worldwide. “To 2030, new areas of LNG link the three markets together and then set the limit as to how long the price differential to oil can be…New sources of LNG exist, which open up the possibility of new regions to be part of the energy game that never were before. Also, LNG isn’t going to be cheap,” as some forecasters have claimed.

Gas now being sold to Asian power markets “has to compensate” for the meltdown of the Fukushima nuclear power plant in Japan, where the gas price today is “at least five times as high as at Henry Hub. But that differential cannot be sustained if we are able to build LNG supplies” worldwide.

Could more money be made by exporting excess North American gas and allowing U.S. and Canadian manufacturers to deal with gas procurement on their own? It’s a viable question, said Waerness, who noted that it’s what Norway does today. He said he found it interesting that North America, which espouses free markets, doesn’t allow it to work that way for oil and gas.

Where there’s conventional natural gas, oil and coal, there are potential unconventional resources as well, he said. Statoil defines “conventional” as what has been produced historically, while “unconventional” is what may be produced. “Natural gas grows in regions where they use a lot of gas, where they have a lot of gas. China will use all energy resources they can get hold of, and shale gas eventually. In terms of ratios and shares, gas is not that big yet but a lot more gas will be going into China.”

LNG exports “maybe from the United States, from North America, could do something about the perpetual trade deficit with China…Oil has peaked and we are seeing more natural gas use in shipping and aviation, shipping both due to regulations and to prices,” he said. “Shippers are being forced to use natural gas instead of heavy fuel oil. A typical example is an LNG vessel, which already has LNG on board. We also see some gas in the transportation sector onshore, and indirectly in transportation through electricity.”

There is an “increasing role for natural gas” everywhere, driven mostly by a regulatory drive to decrease carbon dioxide (CO2) emissions. However, oil demand, especially related to transportation increases in emerging economies, is seen rising to 100 million b/d by 2040, a 15 million b/d increase from today. The renewables market share also is jumping from 1% today to an estimated 8% in 2040.

“Global, primary energy demand is growing by 40% by 2040,” Waerness said. In the undeveloped economies, “energy demand will rise by more than 60% by 2040.” Energy “is a prerequisite for economic growth. Economic growth fueled by energy availability, globalization of trade, improved institutional frameworks and democracy is leading to a large number of people in emerging economies gradually and substantially improving their living conditions and becoming part of a global middle class.”

In line with historical growth over the past 20 years, Statoil expects annual economic growth to average 2.8% a year over the next three decades. The undeveloped countries are growing at an average rate of 4.5% a year, while countries within the OECD, the Organisation for Economic Co-operation and Development, are growing about 1.9% every year.

Statoil, like other forecasters, expects fossil fuels to continue to be the primary energy generator to 2040, with Statoil expecting it to provide about 72.5% of total demand.

“With maturation of the world’s largest oil and gas fields, this raises major challenges in terms of stemming decline and replacing current production,” Waerness said. The technology-driven unconventional resource revolution “means that several ‘new’ types of oil liquids,” such as tight oil, natural gas liquids from shale gas and oilsands, today are economic.

“Together with rising biofuels and gas-to-liquids production, these ‘new’ types of oil liquids will play an important role in replacing most of the declining conventional non-OPEC crude production over the next decades,” said Waerness. “Our primary task is technology development and to make investment decisions which contribute to transforming the energy systems of the world…But the authorities need to provide the framework. They need to create an environment in which making the right decisions is profitable.”

In terms of investments, “the money will be where the people are.” Historical trends indicated that there was sustained growth in Asia Pacific nations until the Industrial Revolution, he explained. Now energy demand again is trending toward Asia. “It’s a very strong trend that we believe will continue to affect energy demand.” The OECD countries used 50% of the world’s energy in 2000, but between 2010 and 2011, “China grew to more than 25%.”

One of the biggest reasons for Chinese growth is in the transportation sector, and thus, more oil demand. “The number of vehicles on the road are all about what’s happening in Asia,” with 300 million private vehicles in China alone.

“It’s not how much they drive, because it’s not like here in the U.S.,” Waerness said. “It’s more like European drivers,” who are able to use a wide variety of public transportation venues. “But you get…oil demand in China, which could be 2-5 million b/d. That’s a lot, and that’s just for Chinese private transportation.”

In terms of North America’s oil growth, “there are huge source rocks…in Siberia that is not like the Bakken Shale in North Dakota, but it’s big. There’s also aboveground conditions in China, Russia and Argentina…As long as you have coal, gas and oil, you also have unconventional. It compensates for the declines, and non-OPEC oil production is increasing, a relatively moderate demand pull.”

Statoil completed its global analysis in June, before the Libyan oil disruptions, Waerness noted. He now thinks that in part because of Mideast market disruptions, “until 2025 we see OPEC struggling to keep market share. After 2025, we believe OPEC is back in business.”

Don’t discount more conventional discoveries, Waerness told the audience. There is a lot of potential to score big field discoveries in the North Sea, offshore Africa and in the ultra-deep Gulf of Mexico. Also, there is the potential for additional new finds in oilsands and tight oil. But all of the new sources won’t be produced for today’s prices. “There’s a potential for more oil, but we will have to pay for it.”

© 2024 Natural Gas Intelligence. All rights reserved.

ISSN © 2577-9877 | ISSN © 2158-8023 |