NGI Data | NGI All News Access

Plump NatGas Supplies Pummel Bidweek Sellers, But Market ‘Bottom’ Questions Arise

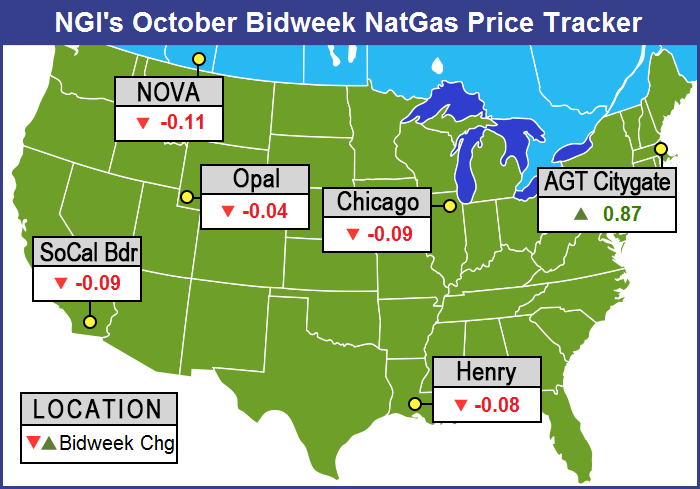

The traditional producing states of Texas and Louisiana suffered the brunt of the decline in October bidweek pricing with declines of up to a dime. With the exception of the Northeast, nearly all regions of the country were off by upwards of a nickel, and NGI‘s National Bidweek Average came in at $2.36, down 7 cents from September bidweek and a whopping $1.19 below October 2014 bidweek.

Of the actively traded market points, Algonquin Citygate topped the leaderboard with an 87-cent rise to average $3.52, followed closely by Tennessee Zone 6 200 L with an 83-cent gain to average $3.36. Bidweek’s biggest loser was Columbia Gas with a 16-cent drop to $2.39.

The Northeast was the only region to post a month-over-month gain, rising 8 cents to average $1.86. However, that still leaves the Northeast as the lowest priced area in the country.

Both East Texas and South Louisiana claimed the cellar spots with losses of 10 cents apiece to average $2.49 and $2.50, respectively.

South Texas did little better with a loss of 8 cents to average $2.51, and the Rocky Mountain bidweek average came in 6 cents lower at $2.42. Both California and the Midcontinent retreated a nickel to $2.73 and $2.47, respectively, and the Midwest escaped with a modest 4-cent decline to average $2.78.

October futures settled Monday at $2.563, down 7.5 cents from the September settlement.

Abundant supplies are at the crux of a softer pricing environment. Figures show that with six weeks remaining in the traditional injection season, 81.5 Bcf would have to be injected weekly to reach a record 4 Tcf, but if November should turn out to feature net injections as well, the figure could go even higher.

Post bidweek, Thursday’s storage report was right on track if not more so if the market is to hurdle a season-ending 4 Tcf and establish a new storage record. The 98 Bcf build for the week ending Sept. 25 put inventories at 3,538 Bcf, which is 454 Bcf greater than last year and 152 Bcf more than the five-year average.

Buyers could not be more pleased. A Florida utility said the company didn’t always purchase monthly volumes during bidweek. “In the past we have gone with the spot market, [but] we are thinking this could be the bottom,” said the utility buyer. “We always do some baseload; we didn’t just go into bidweek thinking we would do dailies. We didn’t go all in but definitely did baseload; prices are very low, and we think they may go up.

“We have seen this price before, and it moved up. We use an index, and we also do basis differentials on last day settle,” he added. “We do both index and basis deals and we found FGT Zone 3 quoted at LDS [last day settle] spot and LDS minus a penny. It was really low. We picked up some [FGT Zone 3] at LDS minus a penny; it was crazy.”

A Great Lakes marketer found basis much higher than expected. Citing the basis on Michcon and Consumers, the marketer said “the basis wasn’t good. The pipelines here in Michigan are undergoing repairs and we were looking at Consumers with a 34-cent basis and DTE [Michcon] was 30 cents.

“By not paying up for the basis we actually got a better price [Wednesday], and we ordered a lot since we didn’t get the baseload we wanted. We did pay less for [Thursday]. We paid $2.82 and $2.85 whereas it would have been in the $2.90 if we had done it during bidweek.”

The marketer said he thought that by hitting the market hard now it might be possible to satisfy a lot of requirements. “We are planning to buy a lot Thursday and for through the weekend and not buying much after that. The high basis was due to outages on Panhandle and Trunkline. There are only a few points you can bring gas to,” he said.

Going forward prices may soften further if Hurricane Joaquin prompts a drop in power and gas load in key east and northeast locations. At 11 a.m. EDT Thursday the National Hurricane Center (NHC) reported Joaquin was located 80 miles southeast of San Salvador and was holding winds of 125 mph. It was moving to the southwest at 6 mph but NHC forecast it would turn to the west and northwest Friday. NHC projects a path toward Connecticut. The storm is resurrecting memories of Hurricane Sandy and its destruction.

At the end of bidweek Wednesday, physical natural gas for Thursday delivery continued to fall. Only a handful of points made it to the “win” column and losses of a nickel or more were common at many points.

The NGI National Spot Gas Average was down 8 cents to $2.30 on Wednesday, and eastern points on average managed to come out flat buoyed by a few locations lifted by a pipeline outage. Futures couldn’t do any better than the physical market, and at the close November had lost 6.2 cents to $2.524 and December shed 6.2 cents as well to $2.701.

Deliveries to Marcellus points put in double-digit drops sending some locations to sub-$1 levels as next-day power prices retreated. The Intercontinental Exchange reported that on-peak Thursday power at the ISO New England’s Massachusetts Hub fell $5.37 to $28.12/MWh. Next-day power at the PJM West Hub fell 92 cents to $35.32/MWh.

Quotes on Millennium fell 18 cents to $1.03 and next-day gas on Transco-Leidy Line was quoted at 81 cents, down 29 cents. Packages on Tennessee Zone 4 Marcellus came in 26 cents lower at 83 cents and gas on Dominion South changed hands at $1.22, down two cents.

Pipeline outages on Transco in southeast Pennsylvania elevated quotes at several Philadelphia-area and New York City points. Gas on Transco Zone 6 non-NY North serving southeastern-most Pennsylvania and southern New Jersey rose a stout 36 cents to $2.39, and gas bound for New York City on Transco Zone 6 vaulted 43 cents to $2.44.

Transco reported on its website that as part of the Leidy Southeast Expansion project, it would be performing facility modifications at Station 515 in Luzerne County in southeastern Pennsylvania. “The current construction schedule requires that compression at Station 515 to be out of service from Oct. 1 through Oct. 22, 2015,” the company said.

Major market hubs were down more than a nickel. Gas at the Henry Hub fell 6 cents to $2.47, and deliveries to Opal were seen 8 cents lower at $2.39. Gas at the Chicago Citygate was quoted 7 cents lower at $2.56, and packages at the SoCal Citygates fell 7 cents to $2.75.

Futures traders see the market in a steady grind lower. “I think we’ll trade down to the $2.45 to $2.50 area and hold again,” a New York floor trader told NGI. “Another 5 cents to 10 cents might be the downside for the next couple of weeks is what I’m thinking.”

That 5-10 cents to the downside was tested with the release of Thursday’s storage figures from the Energy Information Administration. Last year 110 Bcf was injected, and the five-year pace is for a 94 Bcf build. Stephen Smith Energy predicted a fill of 98 Bcf, and industry consultant Genscape Energy was looking for an injection of 102 Bcf. A Reuters poll of 21 traders and analysts showed an average 100 Bcf with a range of 94 Bcf to 110 Bcf.

Analysts now expect an extended injection season carrying through the end of November — and a stunted seasonal price rally. “The gas storage injection season typically takes place between April 1and Oct. 31 each year. The industry does commonly report net weekly injections in the first weeks of November,” BNP Paribas analyst Teri Viswanath, director of natural gas strategy, said in a note to clients Tuesday.

She said as heating demand rose in November, it was unusual to see a net build for the month. “Since the mid-1970s, there have been four years in which monthly injections have been recorded for November. Given our domestic production and demand growth projections, and assuming normal weather patterns, we expect that the industry will likely report the fifth net monthly build for November in 2015. All told, we see working gas in storage increasing 40 Bcf over November to 4 Tcf.

“While we think a seasonal rally for gas is still in the making, the lift-off will now likely be delayed. Moreover, supply-side adjustments will lessen the need to call upon inventory to meet peak winter demand. The end result will be a truncated price rally this winter with high-end March stocks limiting the scope of recovery during the first half of 2016.”

Natgasweather.com sees Hurricane Joaquin generating load-killing showers and thunderstorms along the East Coast “if it can get absorbed by another slow-moving system stalled over the east-central U.S.”

Otherwise, the near-term weather outlook is benign. “Mixed changes are noted overnight nationally,” said Commodity Weather Group (CWG) in its morning report. “We see some cooler adjustments again in the West during the six-10 day, while the Midwest to East are slightly warmer. The 11-15 day changes split in the East, with a cooler start but then warmer finish. The warmest 11-15 day anomalies are in the Western states.

“Overnight models were mixed, but warmer trends at end. Models saw a net demand addition overall overnight, but the individual runs were mixed in this variable pattern situation,” said CWG President Matt Rogers.

© 2024 Natural Gas Intelligence. All rights reserved.

ISSN © 1532-1258 | ISSN © 2577-9877 |