James Waddell, a senior global gas analyst at London-based Energy Aspects, said severe cold, production outages, shipping constraints and a scramble to find supplies are just a few of the myriad factors that have blown into the perfect storm behind a meteoric rise in Asian liquefied natural gas (LNG) prices.

As the historic rally continues, he shares his perspective on when it might end and whether the market can expect similar patterns in the years ahead.

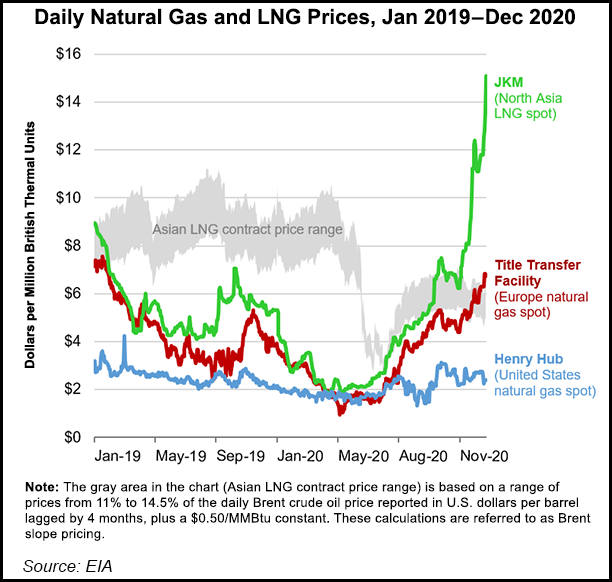

NGI: What’s caused LNG prices in North Asia to increase so much?

Waddell: On the supply side, you’ve had a series of global supply outages rolling on since late summer in Australia, Malaysia, Qatar, Nigeria, Trinidad and Tobago, and Norway. Generally, the supply picture has been underperforming relative to historic...