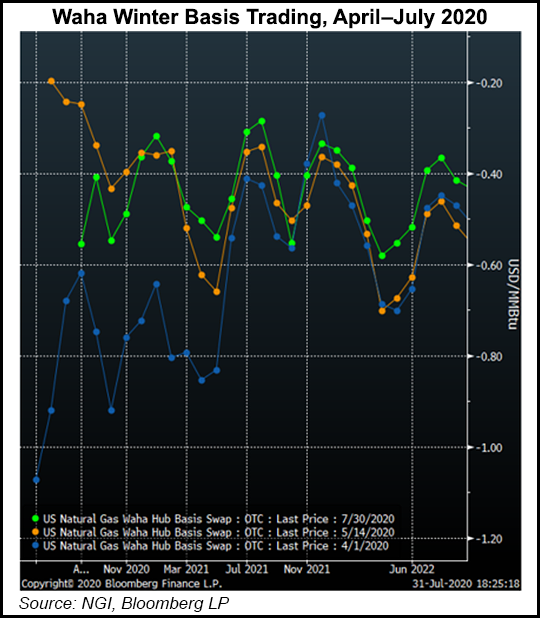

The oil market turmoil earlier this year provided a “rock solid bull trade for natural gas” that lifted basis to levels that should hold through 2021, particularly for West Coast locations and the upstream markets that serve them, according to market experts.

Speaking Wednesday during a webinar hosted by Bloomberg and Natural Gas Intelligence, NGI’s David Dutch, vice president of Business Development and Client Support, said once West Texas Intermediate (WTI) oil prices crashed to an unprecedented minus $37.63/bbl on April 21, the writing was on the wall for oil production.

A byproduct of the retreat in oil activity, though, was the reduced outlook for the associated gas produced, particularly in the Permian Basin. The decline in associated gas led to a wave of strong...