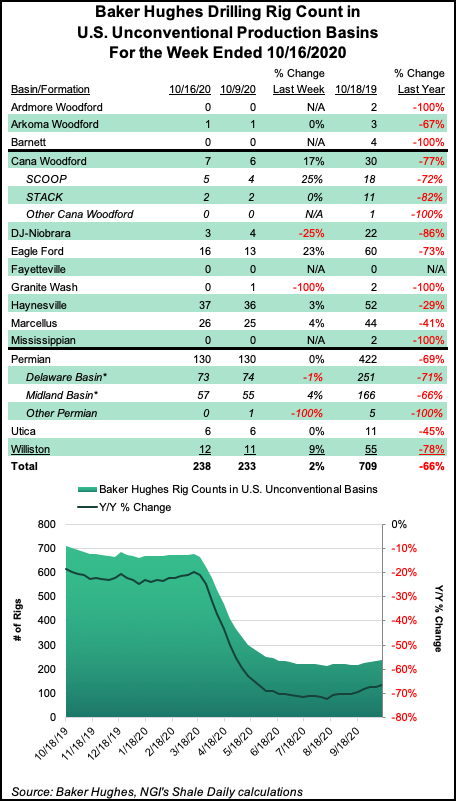

The U.S. rig count surged 13 units higher to finish at 282 for the week ending Friday (Oct. 16) on the strength of gains in oil-directed drilling, according to the latest data from oilfield services provider Baker Hughes Co. (BKR).

Twelve oil-directed rigs and one natural gas-directed rig were added in the United States for the week, leaving the combined domestic tally still 569 units shy of the 851 rigs running in the year-ago period.

All of the gains occurred on land, with the Gulf of Mexico count flat week/week at 14. Seven horizontal units and six vertical units were added, with the total number of directional rigs unchanged, according to BKR.

The Canadian rig count ended the week flat at 80, with the addition of one oil-directed rig offsetting the departure of one...