Markets | LNG | Natural Gas Prices | NGI All News Access

Nymex Natural Gas Futures Fail to Hold Early Gains; Cash Recovers

Share on:

© 2024 Natural Gas Intelligence. All rights reserved.

ISSN © 1532-1231 | ISSN © 2577-9877 |

Markets | LNG | Natural Gas Prices | NGI All News Access

© 2024 Natural Gas Intelligence. All rights reserved.

ISSN © 1532-1231 | ISSN © 2577-9877 |

International

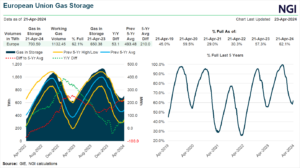

The European Union’s (EU) LNG demand is likely to peak this year and buyers on the continent are likely to be over-contracted by 2030 as efforts to displace Russian natural gas over the last two years have been successful, according to the bloc’s energy watchdog. Since 2022, when Russia invaded Ukraine and cut off gas…

April 24, 2024Natural Gas Prices

By submitting my information, I agree to the Privacy Policy, Terms of Service and to receive offers and promotions from NGI.