In a market at the forefront of the energy transition, natural gas price signals in the western United States instead are incentivizing the construction of newbuild pipeline capacity, according to RBN Energy LLC.

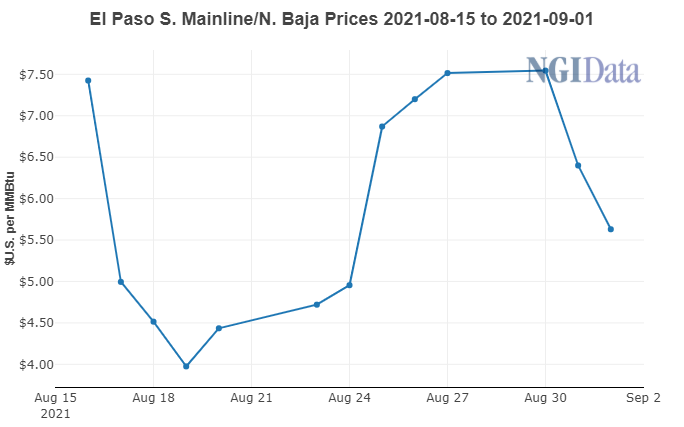

Markets west of the Permian Basin have struggled to consistently maintain adequate natural gas supplies for some time now, RBN analyst Jason Ferguson said. Recent events, however, notably the rupture of a segment of the El Paso Natural Gas Pipeline (EPNG), have served to tighten supplies further.

The Line 2000 segment near Coolidge, AZ, exploded early on Aug. 15, killing two people. The blast prompted EPNG to restrict Permian flows west into the Desert Southwest markets by about 0.6 Bcf/d, according to RBN.

“Those limits remain in place and EPNG flows west averaged...