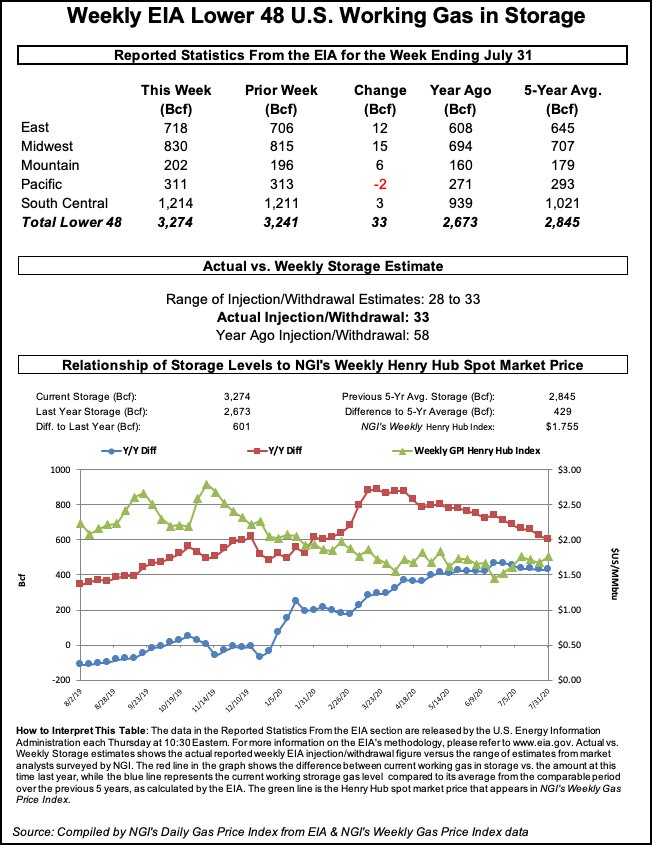

Natural Gas Futures Slip as EIA Storage Data Reflects ‘Woefully Oversupplied’ Market

Share on:

© 2024 Natural Gas Intelligence. All rights reserved.

ISSN © 1532-1231 | ISSN © 2577-9877 |

© 2024 Natural Gas Intelligence. All rights reserved.

ISSN © 1532-1231 | ISSN © 2577-9877 |

Mexico

North American natural gas prices got short-lived support through a Canadian maintenance event on Tuesday but overall continued to languish at well below $2.000/MMbtu. On Wednesday, the May New York Mercantile Exchange natural gas contract slipped 2.0 cents day/day to settle at $1.712. NGI’s U.S. Spot Gas National Avg. rose 12.5 cents to $1.165. TC…

April 17, 2024Natural Gas Prices

Markets

By submitting my information, I agree to the Privacy Policy, Terms of Service and to receive offers and promotions from NGI.