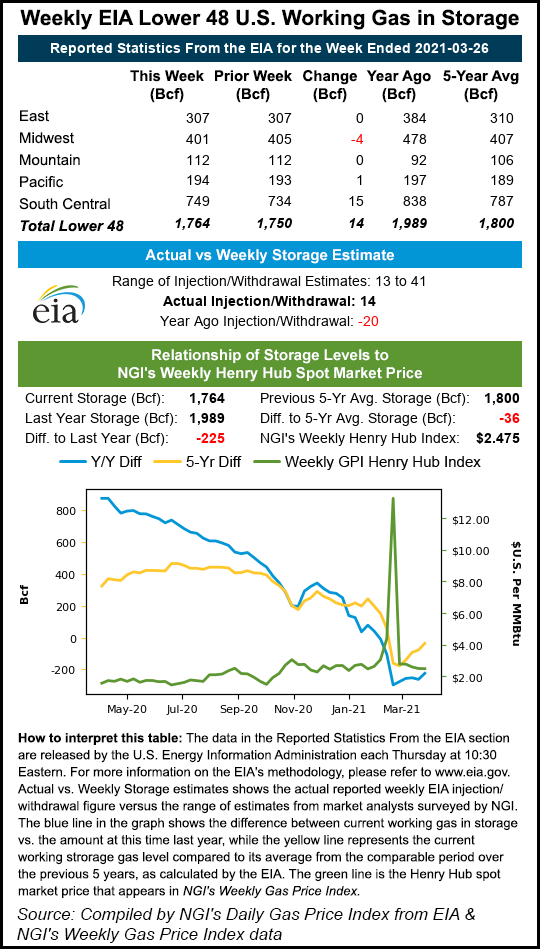

A couple of minor surprises in the latest government storage report sparked a modest gain for natural gas futures ahead of the long Easter weekend. With a few brief cold snaps on the radar, the May contract finished Thursday’s session 3.1 cents higher day/day at $2.639.

Spot gas prices were lower, however, amid weak holiday demand. NGI’s Spot Gas National Avg. fell 10.5 cents to $2.345.

NatGasWeather said volatility was expected given the Energy Information Administration (EIA) storage report and players positioning for the three-day holiday weekend. That proved true as prices started off lower day/day, then rallied and continued to ping pong throughout much of the session.

“To our view, as long as $2.58 holds on May, bulls are in control,” NatGasWeather...