Natural Gas Futures Churn Out Small Gain After ‘Neutral’ EIA Storage Report

Share on:

© 2024 Natural Gas Intelligence. All rights reserved.

ISSN © 1532-1231 | ISSN © 2577-9877 |

© 2024 Natural Gas Intelligence. All rights reserved.

ISSN © 1532-1231 | ISSN © 2577-9877 |

Markets

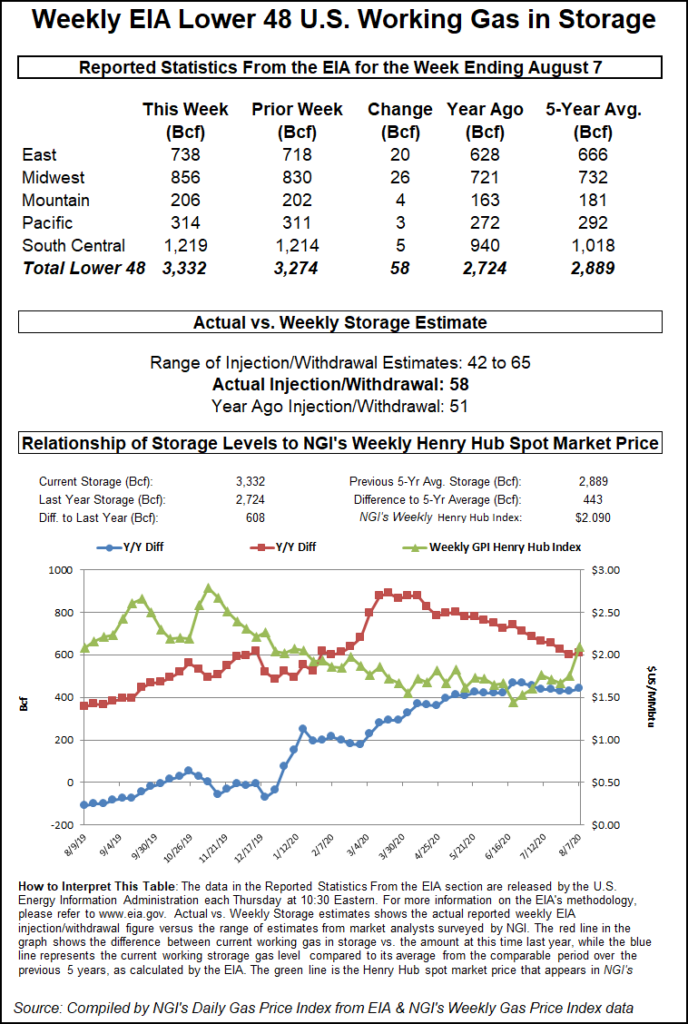

Natural gas futures gained on Thursday, supported by colder forecasts for next week and a government inventory report that showed supplies did not grow faster than expected. At A Glance: EIA reports 50 Bcf injection Forecasts colder for next week Production at 97.8 Bcf/d Coming off two days of price volatility caused in part by…

April 18, 2024By submitting my information, I agree to the Privacy Policy, Terms of Service and to receive offers and promotions from NGI.