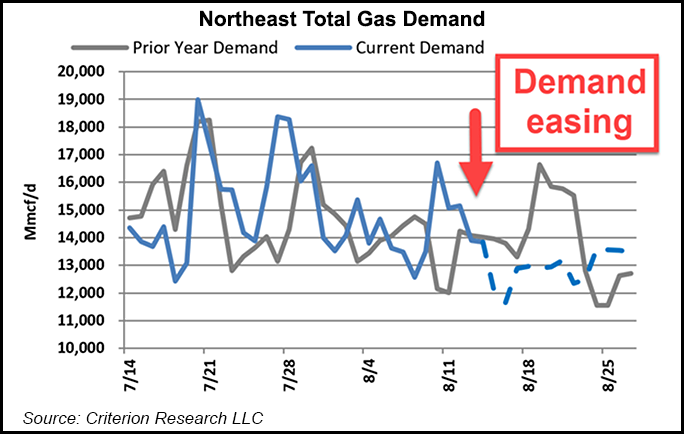

After pulling off a stunning rally in the first week of August, natural gas forward prices were mixed for the Aug. 6-12 period as easing demand pummelled East Coast prices while soaring temperatures prompted sharp spikes out West.

Meanwhile, liquefied natural gas (LNG) demand, which ramped up a bit over the past week, is seen playing an increasingly important role in balances in the coming months, with swelling storage inventories necessitating an outlet for supply.

On a national level, the September contract ultimately averaged flat for the period at $1.886, while October slipped a penny to average $1.976 and the upcoming winter (November-March) gained a penny to average $3.070, according to NGI’s Forward Look.

Taking price action on the East and West coasts out of the...