Natural Gas Clears $3.00 on Hiking LNG Demand, Shrinking Storage Surplus

Share on:

© 2024 Natural Gas Intelligence. All rights reserved.

ISSN © 2577-9877 | ISSN © 2577-9966 |

© 2024 Natural Gas Intelligence. All rights reserved.

ISSN © 2577-9877 | ISSN © 2577-9966 |

Natural Gas Prices

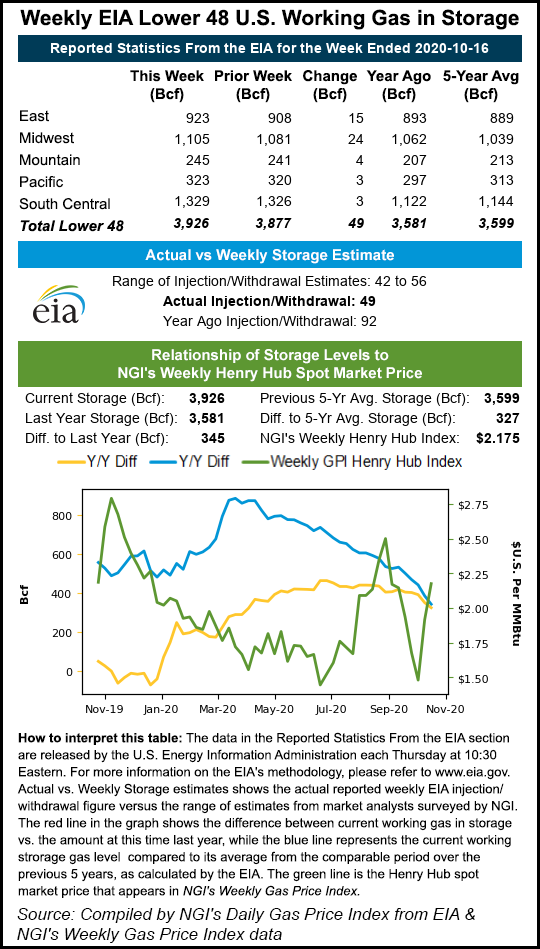

Utilities injected 50 Bcf of natural gas into storage for the week ended April 12, the U.S. Energy Information Administration (EIA) reported on Thursday. The result, near market expectations and avoiding the previous week’s bearish print, sent futures higher. Ahead of the 10:30 a.m. ET government report, May Nymex futures were trading 4.9 cents higher…

April 18, 2024Infrastructure

By submitting my information, I agree to the Privacy Policy, Terms of Service and to receive offers and promotions from NGI.