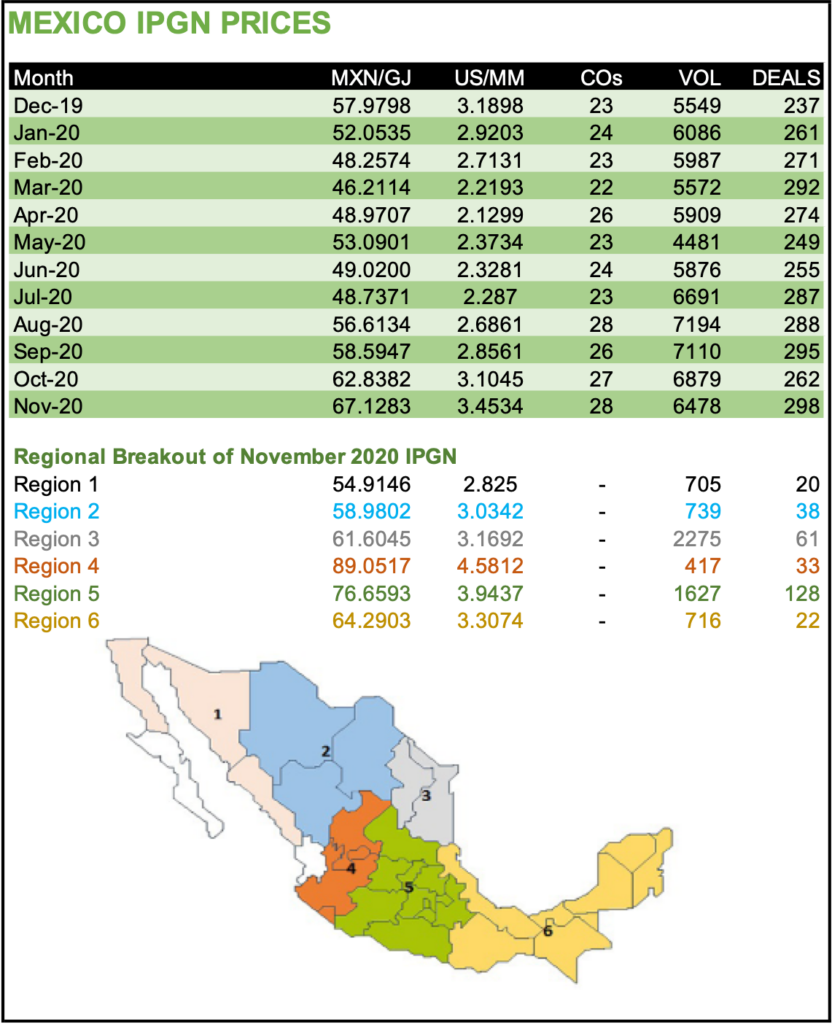

Natural gas prices in Mexico reached a 21-month high in November, averaging $3.45/MMBtu, according to the latest IPGN monthly natural gas price index published by Comisión Reguladora de Energía (CRE).

This compares to $3.15/MMBtu in November 2019.

CRE compiles the index based on day-ahead spot prices reported anonymously by marketers.

CRE used 298 transactions reported by 28 marketers for a total volume of 6.48 Bcf/d to calculate the latest index, up from 238 deals from 24 companies for 6.15 Bcf/d in the similar period last year.

Due to Mexico’s growing dependence on pipeline gas imports from the United States, Mexico gas prices are closely tied to prices at liquid trading locations in the United States, namely Henry Hub, Houston Ship Channel and Waha.

U.S. prices...