The July Nymex contract on Thursday rose for the seventh time in eight trading sessions to $3.253/MMBtu, up two-tenths of a cent day/day, as temperatures across the United States rose and demand for natural gas across many parts of the world remained strong.

“We remain on pace to come close to record hot levels for June as a whole” in the United States in terms of national gas-weighted degree days, “with the expectation that the hotter bias of the pattern rolls on into July,” said analysts at Bespoke Weather Services.

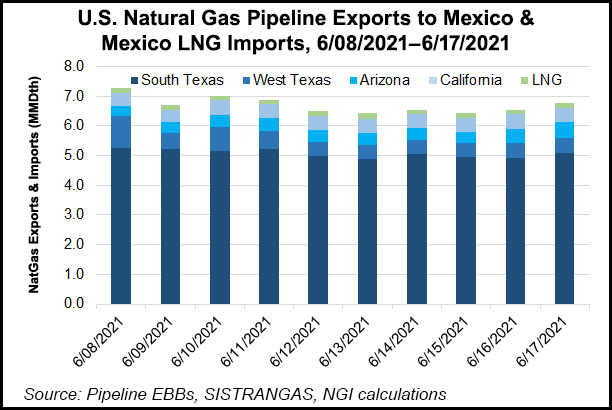

In Mexico, natural gas imports from the United States continued to gain steam as the country’s economy heats up. The 10-day average of U.S. imports into Mexico was 6.70 Bcf/d, according to NGI calculations. On Thursday, committed piped gas from the United...