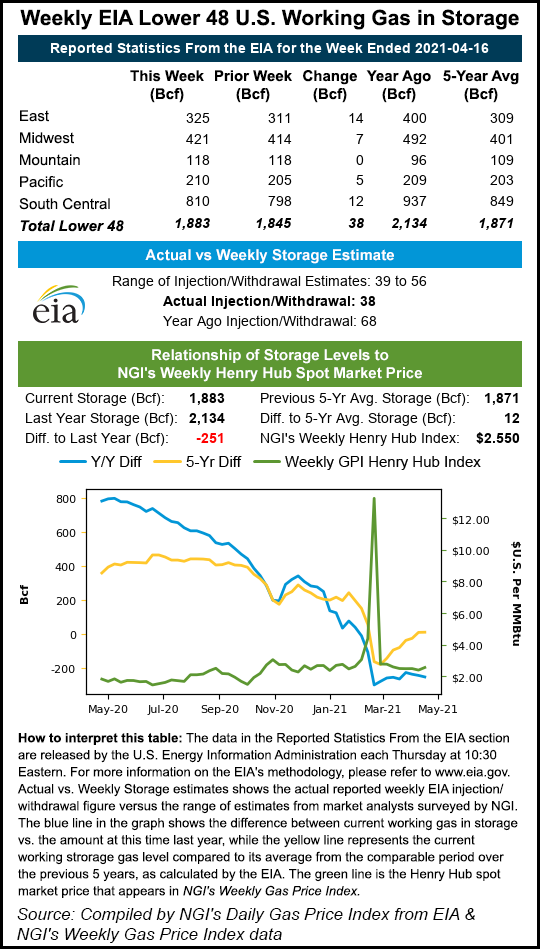

The Energy Information Administration (EIA) reported a smaller-than-expected 38 Bcf injection into natural gas storage facilities for the week ending April 16.

With estimates ahead of the EIA report pointing to a build as large as 56 Bcf, Nymex futures traders harped on the news.

The May Nymex contract was trading nearly flat day/day at around $2.69/MMBtu, with 36,000 contracts traded just prior to the EIA report. As the EIA print crossed trading desks, the prompt month jumped to $2.736, up 4.4 cents from Wednesday’s close, with around 41,400 contracts traded. By 11 a.m., prices picked up another couple of cents to trade at $2.757, with more than 66,500 contracts traded.

The EIA’s 38 Bcf injection compares with last year’s 68 Bcf build and the 26 Bcf five-year...