U.S. oil and gas producers have held the line on capital spending and concentrated on completing wells rather than costly new development, the Energy Information Administration (EIA) said.

The EIA’s Drilling Productivity Report (DPR) issued earlier this month noted that the backlog of drilled but uncompleted wells, aka DUCs, had declined in May by 247 from April across the Lower 48’s major oil and gas basins.

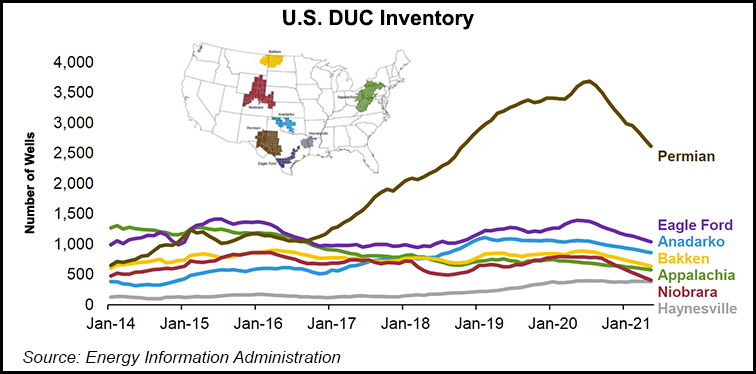

Researchers estimated that, as of the start of June, there were around 6,521 DUCs in the seven major tight oil and shale natural gas basins. The Lower 48 inventory “peaked at 8,874 DUCs in June 2020” amid the pandemic-related downturn in commodity prices and demand.

“Nearly 40% of DUCs (or 2,616 DUCs) are in the Permian Basin,” said EIA researchers....